It is one of the more exciting times to be an investor. Prices have been slashed, but the underlying thesis for many of these companies remains the same. Speculative companies with massive growth potential are still…. speculative; however, the downside risk has dissipated significantly. If these companies can still maintain their growth rates or have healthy cash balances, the risk of losing money on these investments in the long term has fallen dramatically.

Lemonade is a company whose stock has been obliterated in this market; however, the thesis remains the same:

- Become the preeminent insurance company in the 21st century.

- Create a digital insurance company with a different business model from traditional insurers. This model is powered by AI, telematics, and behavioral economics.

- Turn insurance into a social good in society vs. a necessary evil. Completely change how people buy and manage insurance.

Key Metric to determine if Lemonade will succeed:

Customer Growth and Retention:

There are four key advantages traditional insurance companies have over Lemonade:

- More customers: This will lead to stabilized loss ratios. They have clients spread through all 50 states, which minimizes their risk from black swan events.

- Monopoly on good customers: The customers they have are older and wealthier. They are not likely to swap insurance companies due to their loyalty.

- Established brand name

- Stable cash balance

There is nothing Lemonade can do in the short-term about 2-4. However, Lemonade has quickly been able to find new clients. The problem is that rental and pet insurance are niche markets. Most of Lemonade’s clients are first-time insurers and are not considered profitable. The good news is these clients will eventually become profitable, which will lead to lower churn rates. Again, they won’t be able to poach away customers from legacy insurers. Those are loyal customers that won’t leave anytime soon. Lemonade MUST keep bringing in new millennials and Gen Z who care less about the status quo and enjoy Lemonade’s simple user interface, transparency, and social good aspect.

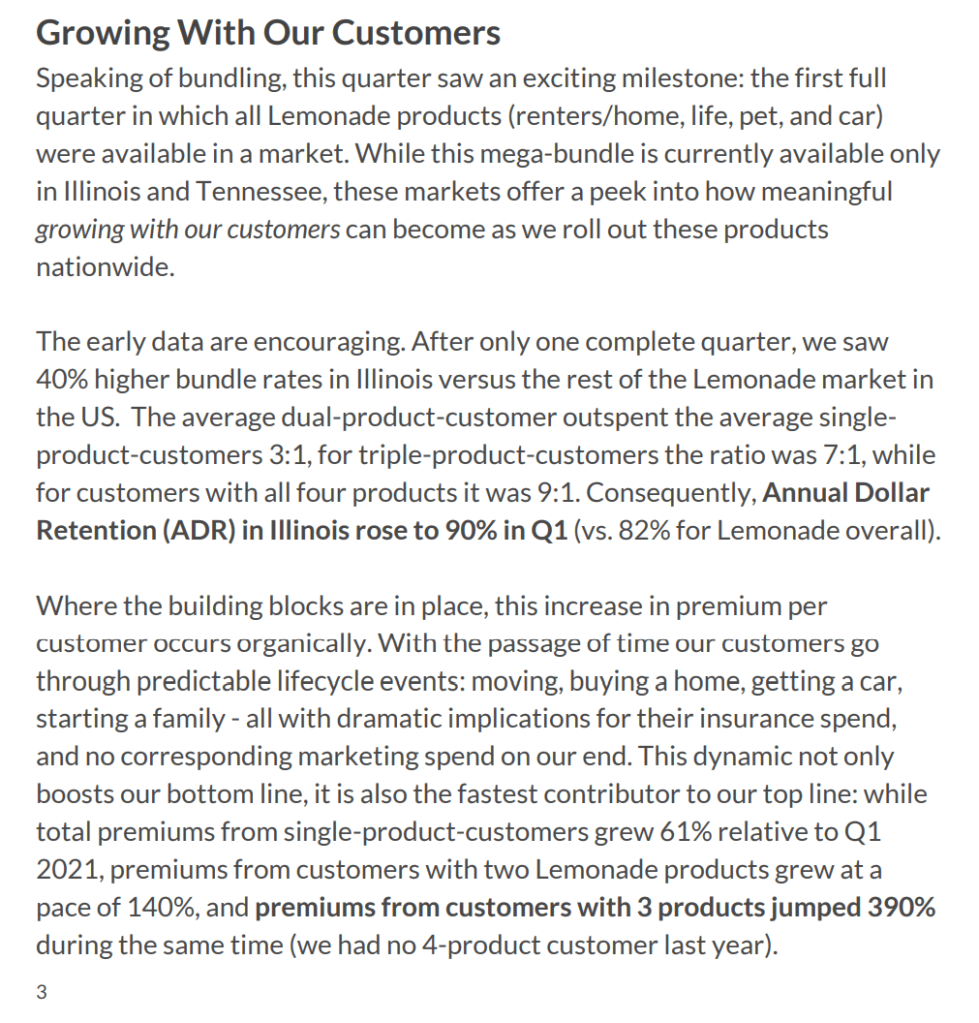

What is REALLY exciting about Lemonade’s future growth is the data from Illinois:

I believe Lemonade car will be their flagship product. You have pets, renters, homeowners, life, and car as an amalgamation. Each product is valuable; however, when you bundle them all together, they have a symbiotic relationship, which allows for cross-selling.

It does not take much brainpower to realize that if Lemonade can offer its full suite of products nationwide, you will see higher bundle rates and lower churn rates as we saw in Illinois.

Imagine if you couldn’t subscribe to Netflix if you lived in California, Texas, Florida, and Texas? Evaluating Lemonade when car insurance isn’t available yet in states with the most licensed drivers creates an incomplete picture. The Metromile acquisition won’t be completed until Q2 of 2022, so we could see a rapid number of new markets in this year’s back half.

I view three critical metrics for an insurance company to succeed:

- Continuously add new customers

- Retain current customers

- Underwriting.

I firmly believe that Lemonade will continue adding customers at a healthy growth rate as they have done from inception. I am confident they can retain these customers as they are popular and highly rated. They will address their churn rate by becoming a one-stop-shop for insurance. What Square is to banking, I could see Lemonade becoming to the insurance industry.

The growth is essential because for Lemonade to become profitable, they need to achieve the law of large numbers and have economies of scale. The more customers they have, the more intelligent and efficient their AI/Machine becomes in evaluating risk and underwriting. Customer growth is, thus, mandatory for the company to stabilize.

The unknowable factor is if Lemonade can effectively improve its underwriting and implement AI effectively. They have better technology. They collect 100x more data points per customer. The question is if they can use that data and technology effectively to create a profitable business. Unfortunately, we won’t find this out until they have more customers. They are also an early-stage growth company which means they have yet to reach economies of scale, and its goals are targeted toward the future, not current growth. I have confidence in their leadership and decision-making; however, taking insurance from scratch to compete with giants like State Farm will take several years to unfold.

The underwriting process is the most significant question mark for Lemonade and all other neo insurers. Here is an excerpt to explain how complicated underwriting is:

The practice of underwriting insurance is a fine mixture of art and science. To be successful, it takes a lot of common sense, even more experience and a well-rounded team of experts. Time and practice are the true keys to the profitable underwriting of life, health and disability insurances. As you can probably imagine, factors such as age, gender, occupation risk, financial viability and adverse health history play significant indicators in the underwriting of most insurance. But other, lesser obvious factors come into play when working in the specialty-risk side of the life and health marketplace.

The Nuances of Specialty-Risk Underwriting

The industry is ripe for massive disruption. It is inefficient and outdated, but entrenched companies are massively profitable. Companies like Lemonade, Root Insurance, and Hippo Insurance have slowly chipped away on legacy insurance. If you are still skeptical about this insurance revolution, consider what Elon Musk just recently said:

“The car insurance industry is incredibly inefficient,” Musk told attendees of the All-In Summit in Miami, which he joined virtually for almost 90 minutes. “You’ve got so many middle entities, from insurance agents all the way to the final reinsurer, there’s like a half-dozen companies each taking a cut.”

Tesla Bets It Can Bring Down Insurance Costs, Make Driving Safer

Tesla underwrites its own policies. They are entering auto insurance more aggressively. Will they succeed? I am not sure. The more this industry is disrupted, the better chance companies like Lemonade can take massive market share away from legacy insurers. If Telsa does become a major insurance company, they are only in one market dealing with Tesla vehicles. Lemonade has the entire insurance market.

I look at Lemonade like a small fire. Once it spreads, it can do so rapidly at an uncontrollable rate. Lemonade’s operating team runs in a very autonomous and frictionless way, which is why they have had success in an industry that typically moves at the speed of molasse. It’s like their version of “Move fast and break things.” I look at them more like a tech company than an insurance company.

From an operational standpoint, Lemonade moves from how to get from point A to D while others companies are moving from point A to B. This kind of thinking makes them misunderstood, and if you do not like volatility, you shouldn’t invest in Lemonade. If you can stomach the roller coaster over the next few years, Lemonade could be a big-time winner in this space.