Randominvestorhttps://investinmyselfcom.wordpress.comThis is my personal blog about finances, the stock market, and investments. Disclaimer: I am not a financial advisor. Take anything I say for entertainment purposes only.

Revolve is still undervalued and mispriced by Wall Street simply because the majority of analysts who cover it do not understand the nuances of the company. Heck, most of them are still figuring out what they sell. This isn’t surprising. Revolve’s demographic is female Millennial and Gen Z consumers. The demographic of Wall Street are typically white Gen X males like this analyst covering the company.

Here is a video of one analyst giving his assessment of Revolve. This is a sound analysis from a book value perspective but even he admitted: “I am not a Gen Z’er or Millennial so it is too fashionable for me, I am old school.” Were no female contributors not available to give their opinion? If you were to ask his wife or daughter, they probably would be able to give a more accurate description of what the company does.

The analyst said, “I don’t get this kind of retail,” and “I went to their website because I had to figure out what they sell.” Can you imagine a professional analyst covering Tesla or Apple saying they had to go on their website to figure out what they sold? This seems shocking but not surprising. The majority of people on Wall Street have a limited scope of expertise. It is plagued by herd mentality and an inability to think outside the box. Regurgitating financial statements is not enough. What many on Wall Street are missing on Revolve is that they represent the future of e-commerce fashion retail. This may be obvious for someone born after 1980 but not so much for out of touch Wall Street.

Revolve from a financial perspective is doing well and has a positive outlook, but that is only half the story. Here’s a summary and what many analysts are missing. Revolve is a luxury lifestyle/fashion brand located in Los Angeles (specifically Cerritos) California. Los Angeles is emerging as the fashion capital of the United States. The “Big Four” global fashion capitals are widely considered London, Milan, France, and New York. Fashion is to New York as Big Tech is to Silicon Valley. Any legitimate luxury fashion brand is located on Fifth Ave.

Los Angeles has been emerging as a growing fashion hub where it will eventually become the 5th global fashion capital. I am no expert in fashion, so please take whatever I write with a grain of salt however it doesn’t take much research or an open mind to learn this trend by reading any random reputable fashion blog.

GETTY IMAGES

Reasons for this shift:

Instagram’s popularity has allowed emerging designers to showcase their work much more easily and LA has become the preferred destination of choice.

Celebrity brands/culture has grown (fueled by social media) much more popular within the past decade. Look at Robyn Rihanna Fenty, who launched her lingerie line in 2018 called Savage X Fenty. The company is headquartered in El Segundo California. Rihanna is now a billionaire and has a higher net worth than the majority of rappers she collaborated on songs with this past decade.

Los Angeles culturally is considered more about wellness and leisure. This more health-conscious laid back lifestyle is trending upwards and becoming more popular.

What Revolve has done in a short amount of time is quite remarkable. They may become the first true American luxury fashion brand outside of New York. Los Angeles’s growth in fashion also coincides with it becoming an emerging tech hub as well. This isn’t just about a fad fashion retailer but a growing fashion empire that is attracting the most influential social media influencers and designers in the fashion space. This shift just happens to coincide with retail spending rapidly moving online. I like to make bets on trends and in my opinion Revolve is grossly underpriced. I see Revolve priced similar to where Lululemon was priced in 2017. I will gladly hold onto my shares of RVLV and watch it appreciate as Wall Street figures out what they do as a business.

There is a lot of excitement regarding psychedelics in treating serious illnesses. I believe this sector can one day be bigger than cannabis. Psychedelics refer to:

Psilocybin (Shrooms)

Ketamine

DMT/Ayahuasca/Dimitri

Peyote/Mescaline (Cactus)

MDMA (Ecstasy/Molly)

Salvia Divinorum

LSD

Ibogaine

In the future, I believe many of these drugs will be used to treat mental illness and addiction. I am super excited and optimistic about this space in general and I prescribe to the idea a rising tide lifts all boats. A lot of these psychedelic biotech companies will likely be really profitable down the road. We are only in the beginning stages of this sector as none of these drugs have been approved by regulators yet. I think companies focused on Psilocybin treatment will gain market share the fastest as Psilocybin is the easiest of these drugs to be distributed. In the psychedelic sector, the biggest companies focused on mainly Psilocybin are:

ATAI Life Sciences Compass Pathways Plc Mind Medicine Cybin Inc

The science supports it:

There is evidence that the reduction of astrocytes in your brain is linked to depression. Psilocybin and other psychedelic drugs may increase or boost astrocyte function. Recent studies have been overwhelmingly positive:

Dr. Charles Grob, a professor of psychiatry and biobehavioral sciences at UCLA, who worked with terminal cancer patients in the early 2000s, says many of the patients he worked with emerged from the experience with a newfound ability to focus on the present moment.

Most of his patients came in experiencing high levels of existential distress, demoralization, depression and anxiety. After the psilocybin treatments, they often left with a newfound sense of peace and a determination to spend the rest of their days connecting with loved ones and making the most of the time they had left.

“Because there are several types of major depressive disorders that may result in variation in how people respond to treatment, I was surprised that most of our study participants found the psilocybin treatment to be effective,” explained Roland Griffiths, PhD, study author and director of the Johns Hopkins Center for Psychedelic and Consciousness Research.

By the late 1960s, funding and research on psychedelic therapy stopped due to politics and regulation. Today the politics and mood have changed. In 2019 The FDA greenlighted Psilocybin medical research. Now regulation has eased with several cities decriminalizing Psilocybin. In 2020 Oregon legalized Psilocybin for therapeutic use. The fact is that science was right 50-70 years ago and it hasn’t really changed (which is a good thing). What has changed is the money. This type of research was only getting a small amount of funding up until recently. Now VC deals and institutions are pouring million into psychedelics the past two years.

Don’t bet against Peter Thiel:

Peter Thiel is a co-founder of PayPal. He was the first outside investor of Facebook. He is the chairman of Palantir Technologies. His track record is impressive and shadowing some of his investments would seem like a wise decision. Both Compass Pathways Plc and Atai Life Sciences are backed by Thiel. I would assume Thiel having a Silicon Valley background, knows how big Micro-dosing is thus, understands how big the market would be if Psilocybin received a medical pathway from the FDA. This to me is a no-brainer. If it’s good enough for Thiel, I will follow his lead. One of my favorite investing quotes is from the great Charlie Munger: “I believe in the discipline of mastering the best that other people have figured out. I don’t believe in just sitting down and trying to dream it all up yourself. Nobody is that smart.”

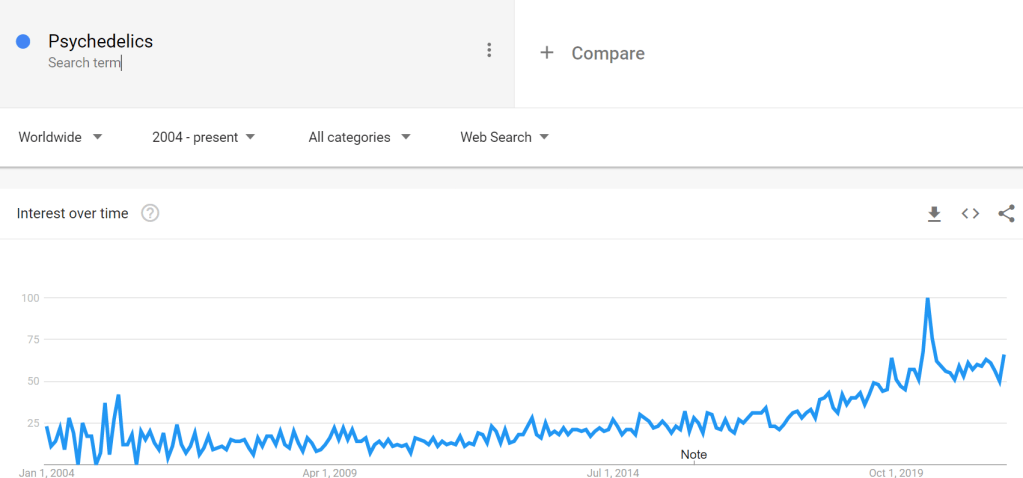

There is simply too much good news not to invest in Psilocybin. I believe in the science and data. Will there be political and regulatory hurdles ahead? Absolutely, but let’s exercise some common sense. If you believe the thesis that Psilocybin can significantly help many people with depression, addiction, or mental illness, wouldn’t it be better for this to be on the market, covered through insurance, vs the current antidepressants available? We wouldn’t be having this discussion if there was a viable legal solution readily available to combat mental illness and addiction. Psychedelics/Psilocybin is trending upwards for the past 15 years on Google trends. Clinical trials today are much safer compared to the 60s. The face of the Psychedelic movement is not nutty psychologists giving acid to random people but well-respected entrepreneurs with money and influence. They give credibility to this space and can help with the regulatory approval process. Aside from the actual science is the story. Mega Influencers like Peter Thiel can help shape the story of this industry and avoid the roadblocks we have seen in cannabis.

The fight is won or lost far away from witnesses—behind the lines, in the gym and out there on the road, long before I dance under those lights.” – Muhammad Ali

FUD: Fear, Uncertainty, Doubt

“The biggest risk is not taking any risk. In a world that’s changing really quickly, the only strategy that is guaranteed to fail is not taking risks.”- Mark Zuckerberg

Often many of the decisions we make are based on fear. We may not like the decision, but we do it anyway out of fear. We work at companies we may not like for fear of not being able to support ourselves. We get married out of fear of being alone. For investing you would think more people would invest out of fear of not having enough money for retirement however the majority of Americans do not invest anything at all. A big reason for this is due to a fear of loss. This fear could be correlated to loss aversion, which is the tendency for humans to experience a loss with twice as much impact as an equivalent gain. This fear causes people to not invest at all or invest too conservatively to avoid the pain.

The media helps play on these fears as negative headlines tend to garner more attention than positive ones. How many times have you read the word “crash” in a headline when the stock market falls? A stock falling a few percentage points is technically not a crash, yet we see that word being used liberally regarding the financial market. These scare tactics are poisonous for novice investors or those starting on their investing journey.

The truth is stocks going down is quite normal and a sign of a healthy stock market/portfolio. They are inevitable and happen quite happen. Pain is something we cannot avoid in all aspects of life, especially regarding the market. When people say they don’t like volatility, they are saying they don’t like downward volatility. If you take volatility away from the market, you essentially have a savings account. Volatility provides the ability for your portfolio to beat inflation and get massive gains. One of the best analogies I can make to being an investor is to that of being a boxer. In boxing, it is inevitable for a boxer to get hit. Every boxer expects to be hit however they simply cannot stay on defense the entire fight. To win a boxer needs to take an offensive position and throw punches, even if that means an increased likelihood of being hit themselves. A boxer that takes no risk, will never win. A boxer that takes too much risk, might get knocked out. The key is to find some sort of balance

Great boxers and investors:

Get hit and suffer losses, that is inevitable.

Try to avoid getting knocked out

Understand this is a long game. Boxing is 12 rounds. Not every fight will end in a round one TKO. Not every investment will be a 10x gain in one month.

Make adjustments. Remember Mike Tyson’s famous quote: “Everybody has a plan until they get punched in the mouth.”

Train, study, and prepare. It is said the fight is won long before the bell rings.

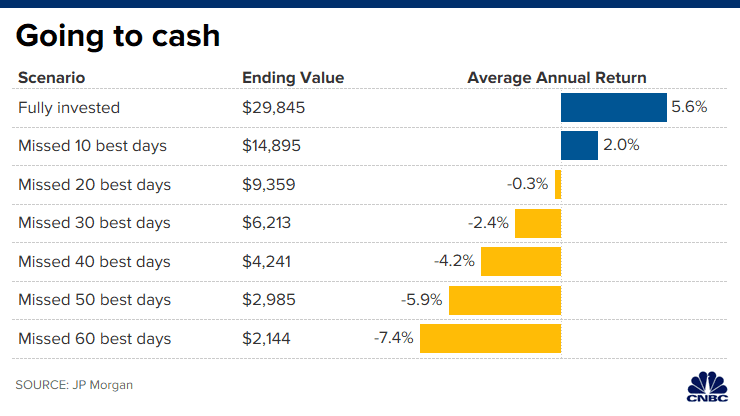

How 10,000 invested in the S&P 500 index, for the 20 years of 1999 through 2018, would have performed under various scenarios.

Staying in the market in the long term is important. We simply do not know when a stock will have its biggest upswing. It can happen right after a stock has its biggest downswing. Trying to avoid pain altogether is typically a losing strategy. When you pull out of the market simply to avoid short-term loss, you risk missing out on the best days. Not accepting risk is a big mental hurdle preventing many from investing. The stock market is impossible to predict accurately in the short term and trading in and out of stocks too frequently puts you in a trader’s mentality. Stats have shown the majority of day traders lose money.

Psychology plays a lot in investing and life in general. These barriers are a big reason why people stop or never invest. Here is some general advice that could help you as an investor.

Evaluate companies based on what you project they will do in the future. Remember, no company beats on earnings every single quarter. Don’t be a prisoner of the moment.

Understanding the price of the stock may not be the best indicator of how a company is performing or how it will perform in the future.

Growth stocks like Tesla, Lemonade, Affirm are volatile by nature because they are valued on future potential earnings which are 3-5 years down the road, potentially longer.

Earnings drive stock prices in the long run. How the company performs, not macroeconomic events or sentiment will determine the projection of the stock price.

There is no exact formula or metric that will tell you where the stock is headed. Anyone can look up a company’s EBITDA or P/E Ratio. Investing is not a math equation.

My best response to comments rooted in FUD about investing.

I am not a financial expert, I don’t know which stocks to pick.

If stock picking was purely a science, wouldn’t the majority of mathematicians, accountants, and college professors all be millionaires? If you could predict stocks based solely on a formula or chart patterns, why are so many smart people wrong so many times?

The truth is stock picking is not purely a science, it is just as much an art. If you listen to some of the wealthiest investors, they all say something similar. One book I would highly recommend is One Up On Wall Street: How To Use What You Already Know To Make Money In The Market. It is a very quick read and although Peter Lynch wrote the book in 1989, the advice in the book is just as relevant today as when it was originally written.

Believe it or not, retail investors have a major advantage over Wall Street. The majority of retail investors live in the real world, they experience it. Wall Street is a bubble made up of mainly upper-class, older white males with an east-coast bias. Institutional investors have an advantage with transactional data however they have a very antiquated approach to interpreting that data. The advantage we have is in our imagination. We are a diverse group of people with different backgrounds and experiences.

90% of Wall Street is looking at the same data under a herd mentality doing the same thing. There is very little diversity or creativity involved. If you are looking for a fresh idea, the last place you would want to go to is a financial institution. Set up a meeting with a bank or Wealth Management Group and ask them a few questions. They typically provide the same investing approach. If you want creativity, go to an art studio, a music festival, or talk with a fashion blogger. You will probably get more relevant ideas that could spark your next great investment.

We all have unique perspectives, so utilize that in our investment philosophy. Identify change by making casual observations. Consume information to identify a change which could be anything – politics, consumer behavior, science, etc… Based on what you observe connect that to an investment opportunity. We are all experts in some sort of field. Some fields like chemistry, energy, or medicine require more knowledge to understand however things like brands, products, consumer behavior, pop culture, or entertainment are things that millennials and Gen Z are quite knowledgeable about.

If you are going to invest in something regarding social media, why would you listen to the segment of the population that never uses TikTok or Snapchat, or don’t even understand how these platforms work? Wouldn’t you want to listen to the people that use that platform daily?

Developing a quick thesis is not that hard. If you can come up with a few logical bullet points in owning a stock, you will likely hold it longer and know when to sell it when that thesis changes. Here is an example of how to develop reasoning to own a certain stock:

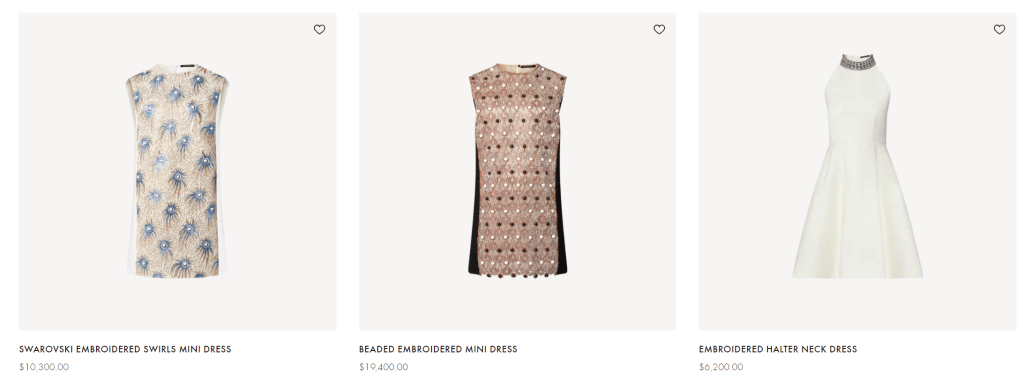

I know what Instagram is. I noticed a lot of luxury brand companies like Louis Vuitton on it. They have a big following. Instagram seems like a great platform for luxury brand companies to build awareness and gain customers. The site is a perfect environment to promote an aspirational lifestyle and luxury experiences.

Luxury companies have already learned that Instagram is a driver of sales and have responded by dramatically increasing their social media presence and budget. Based on my research going on Instagram this is evident. When a consumer sees Louis Vuitton’s Instagram page, it’s just as influential as going to the store in person. Just in a day, a consumer can purchase a $2,000 dress, $1,000 top, and $800 hat all in a single purchase based on one Instagram post.

This is why I consider Apple, the Louis Vuitton of Electronics. One of the top five richest men in the world is Bernard Arnault, the head of Louis Vuitton who has no tech background. Consider the cost to make a Tesla or iPhone vs the cost make a handbag or dress. The margins are quite intriguing.

When I see some high-end fashion stores packed with customers I wonder “who is buying all these overpriced items?” Instagram is fueling these sales as multiple posts can create demand for buying multiple outfits and the luxury fashion brands that can best utilize social media will likely see higher revenue growth in the future.

Cost of dresses on Louis Vuitton’s website

Reasons to Invest in Louis Vuitton.

Reason 1: Pent-up demand from the pandemic. A lot of people have money to spend and a lot of that will go into luxury products.

Reason 2: Social Media platforms like Instagram are fueling the growth of Luxury Brand companies

Reason 3: Inflation proof: If you are already going to spend $5,000 on a Louis Vuitton handbag, is increasing the price to $5,500 going to deter you from buying it? When you decide on buying a handbag, you also need the matching outfit and accessories, which means more spending.

Reason 4: Louis Vuitton has a strong luxury brand name. Biggest fashion brand in the world outside of Nike, clearly number one in luxury fashion, not even close. Unless they do something to hurt their brand name like go into factory outlet malls, that won’t change soon.

FYI I have never invested in Louis Vuitton, but have considered it though. I have used this thesis/thought process to invest in companies like Stitch Fix, Revolve, and Coach. The biggest thing you should ask is why? It is one thing to understand that Louis Vuitton is the top brand name in luxury, but a good investor will understand why it is.

I work too hard. I won’t risk losing it all

If you are that risk-averse, you should most likely invest in low-cost index funds or put a small percentage of your net worth in individual stocks. Only put what you are willing to lose, but also be prepared on missing out on gains. When you are investing in an ETF or Index Fund you are mitigating your losses but also capping your gains.

An ETF can have hundreds if not thousands of stocks inside the fund. An Index Fund is typically designed to mimic the index or benchmark, not beat it. With lower risks comes lower rewards. Single stocks appear to carry more risks however some stocks are conglomerates. Companies like Tencent, Berkshire Hathaway, and Louis Vuitton can be considered well-diversified as they are multiple businesses under one parent company. Given how diverse one company can be, investing in multiple ETFs can be considered a cluttered investing strategy.

The stock market is a giant casino/Ponzi scheme. It is designed for me to lose money

When you think about that statement more in-depth, do you wonder how people lose all or near 100% of their wealth in stocks when in the long-term the stock market goes up? Did they engage in options trading, margins, shorting the market, or buying penny stocks? Ask and you might not get a clear answer. The problem with the Wall Street mentality is that they focus too much on quarter-to-quarter results. It’s as if once they get a decent gain, they already have their eyes on the sell button. Having this type of mentality puts you closer to a gambler rather than an investor. Why sell a stock you know likely will 10x 5-10 years later? If you view stocks as a get-rich-quick scheme then yes, it can feel like a casino. The shorter your investment strategy the more risk you are assuming. Psychology and emotions might take over and allow you to cut corners or do something stupid. We are all guilty of making make bad investments but again, the common theme of investing is that you have to be invested and assume risk to make money. That is the necessary risk to become wealthy.

There is too much risk in the market

If one could time the market accurately, you would likely have at minimum, a billion dollars. There is no such thing as a risk-free stock market.

The amount of risk you subject yourself to in the market is probably more based on your personal qualities rather than external factors. Good traits for investors are typically patience, use of common sense, open-mindedness, humility, a willingness to learn and admit mistakes. If you have ever watched an episode of Gordon Ramsay’s 24 Hours to Hell and Back or Bar Rescue, you see many owners stick with a failed business strategy (stubbornness/close-minded) and ignore good advice (lacking common sense) despite bleeding their business dry.

Stocks can be viewed as an educated gamble where the odds are tilted in your favor. When you engage in more short-term riskier activity, you are mimicking the gambling you see in a casino, which is more luck-based. Patience and time are some of the greatest edges an investor has but many don’t utilize them enough. It can erase big mistakes and turn a small amount of money into a fortune.

My best advice is that when you invest, you should have some sort of plan. Whatever you do, measure the survivability of your plan. The more risk, the less likely that plan is to survive. If one risk can wipe you out completely, it is probably not worth taking. Genius can be defined as seeing opportunities so obvious they go unnoticed by 99% of others. The best investment you make is more likely to come from something you wear or eat every day rather than a company working on advanced genomic testing or hydrogen fueling stations. Allocate your risk accordingly but remember to take risks.

Buy Now, Pay Later services have gained massive popularity recently. Three of the biggest BNPL companies are Klarna, Affirm, and Afterpay. Klarna is headquartered in Sweden and will likely IPO eventually. Affirm (NASDAQ: AFRM) partners with companies like Peloton and Amazon. Afterpay, which is headquartered in Australia was acquired by Square (NYSE: SQ) in August. BNPL is point-of-sale, or POS loans, which allow consumers to make monthly installments – often in four months. Klarna and Afterpay require 25% due at purchase. Both do not charge any interest but do charge late fees. Affirm could charge 0 due at purchase and does not charge any late fees. Affirm does charge interest as low as 0% and as high as 30%. Klarna and Affirm may do credit checks and report missed payments to credit bureaus. Afterpay does not perform credit checks.

For these companies to become profitable, they will need the majority of their customers to consistently make their payments on time. Unfortunately about a third of users in the U.S. who have used BNPL have fallen behind on one or more payments. The typical item being purchased is under $500. There appears to be a lack of consistency or reporting to credit bureaus but it is safe to assume that many that do miss payments will see their credit score decline, although the exact number is not clear. These companies do not have consistent data as underwriting standards seem minimal.

The delinquency rate for all consumer loans runs between 2-3%. The highest it has ever gotten is 6.7% in 2009. The Australian Securities and Investment Commission (ASIC) found that 21% of BNPL users in Australia had missed a payment. As of right now, there is no real incentive for someone that can make a full payment to utilize BNPL. If they offered some type of reward program, like credit card rewards, it would entice a lot of consumers that are consistent payers to utilize this payment feature.

I have 18 active credit cards in my portfolio. I obtain credit card reward points on everyday purchases. A lot of the cards I applied for, like the American Express Platinum, require a credit score of over 700 to be approved. A lot of people who are getting these reward points are not lower-income households. You could argue that lower-income households are subsidizing those reward credit cards from their purchases. At this point, I am wondering who is subsidizing consumers utilizing BNPL. For these companies to become profitable, they will need to keep increasing their footprint but have to decide if they are a true alternative to credit cards or a modern-day version of a payday loan.

BNPL companies could be good investments however regulations are likely so there could be better buying opportunities in the future. Right now BNPL is a very niche space in the financial market. As it currently stands, companies like Affirm are more like Moneytree rather than a go-to financial services company. The upside and opportunity are there however I would rather stay in companies like Square and PayPal which in my opinion have less risk.

I am a big fan of the fintech sector. I believe this space is growing and profits will keep steadily increasing. Now is BNPL good for the average consumer, and will it increase consumer debt and misery? I do not believe loans are inherently good or bad. People can obtain student loans and credit card debt and pay them off responsibly. I am not the arbiter of morality. If someone without the money wants to make payments on a sweater or shoes, it is on each individual to pay off those items. I believe the government has some sort of obligation in protecting consumers however regulation won’t prevent people from making poor financial decisions.

* On a side note, I hate talking about politics and I hope this is not perceived as a political statement. Our country will be at its best when we focus on lifting people out of poverty. There shouldn’t be dramatically different class systems. Lifestyles should be more equal all around. When we focus on that, and not so much on promoting individuals and corporations to gain massive wealth, our economy will truly stabilize. It took a Great Depression for the government to create a response (The New Deal) to help millions of families out of despair. We should always prioritize lifting those in poverty and preventing them from falling through the cracks. By increasing the wealth gap further and further, we risk a higher likelihood of economic cratering. When more and more people go into extreme poverty and fewer individuals reach extreme affluence (shrinking the middle class) our entire system becomes less fair and more dangerous.

The United States made it a priority to normalize debt after World War II to prevent another great depression. The government has promoted the mantra that having debt is okay and an acceptable way to finance your lifestyle. Student loans and credit cards began in 1958. Our government has equated owning a house, to the American Dream, even if that means you cannot afford your mortgage payments in the long term. If you ever wonder why personal finance is never taught in public school, you should know why. Increased consumer spending helps prop up the economy and is favorable for businesses.

I want to be financially frugal and responsible. I want others to do the same as well. The sad irony is that I benefit personally from increased consumer debt even though I don’t have any myself. If consumer behavior dramatically changed overnight and a large segment of the population became financially responsible, that would not be good for the economy overall. A lot of the companies I invest in would lose revenue, and may even become unprofitable. The economy would likely suffer and go into a deep recession. What would become of American Express and other banks? Who would financial advisors help if no one had debt? That’s why I believe things will not change anytime soon. Based on studies, 60-70% of people would rather talk about sex, politics, religion, or their mental health before finances. It is just a very taboo subject people do not want to discuss openly. Not enough people talk about personal finances, and there are too many debt instruments that create negative compounding interest, which destroys an individual’s wealth. This may not be the brightest outlook but that doesn’t mean you will become a victim to this instant gratification culture. You (and only you) are responsible for the financial decisions that you make.

Dwayne Johnson got released by the Canadian Football League before becoming a Pro Wrestler, and eventually an A-list Actor

I would like to go in-depth on why so many people don’t invest anything at all. I think the best way to analyze this is to break down the main reason why. I definitely would like to re-visit this topic in the future as I will only go over the main reason cited for people not investing. It is assumed by numerous surveys/studies, that around 40-60% of Americans have absolutely nothing invested in the stock market. The #1 reason provided is not having enough money. Studies have shown 70% of millennials are living paycheck to paycheck. An even more shocking finding can be found here. 60% of millennials earning over $100,000 a year are living paycheck to paycheck.

Here is what I take from these findings:

You can’t invest if you don’t have savings – The next logical question is why don’t Americans have enough savings? One thing I have learned is to master savings and investment, you need to get in the correct mindset. Savings and investing are more mastery of psychology and behavior rather than financial knowledge. 60-70% psychology, 30-40% knowledge of numbers, formulas, statistics, charts, or what I call head knowledge. The best analogy I can make is living healthy. Why do people continue to eat so much junk food if they know it is bad for them and they can easily find healthier options elsewhere? Why do people not exercise enough, even just walking 30 minutes a day? A big component of this is behavioral psychology. There are deeper reasons why people do not save enough money but this is just a very brief summary. Saving money is the gap between your self-worth and your income. Wealth is created by suppressing what you can buy right now to increase the value of your money in the future.

High income does not equate to wealth – As evident to the numerous millennials making six figures but living paycheck to paycheck. The best example I can think of a wealthy person with a modest income is Ronald Read, a career janitor, gas attendant, and mechanic who never earned over $100,00 in a year. When he passed away at age 92, he was worth over $8 million, mostly in stocks. How was this possible? Investing, even a small amount, can create massive wealth. A high income simply provides one with the ability to invest. Whether you invest is dependent on many other factors.

Relying solely on your income in the long-term is a suckers bet – Unfortunately, I see a lot of people relying on their income to create wealth, and that is a likely pathway towards mediocrity. There are too many negative variables with your employer that can change – losing your job, the company becoming unprofitable, office politics, nepotism, the economy, COVID-19, family situation changing, age discrimination, etc… The fact is, the few that do climb the corporate ladder and become executives in their company do not build wealth through their salary! The reason why these people do become millionaires is most likely through equity sharing plans or stock options. For the majority of us, this pathway is not realistic even though many of us cling to this internal belief that if they work hard enough, they will be eventually promoted or given a raise. Consider that on average, a millionaire’s income makes up only 8.2% of their net worth. Someone with one million in net worth is not making anywhere close to a million a year from an employer. My thoughts: consider other ways to make money or as a supplement to your current job. Dwayne Johnson couldn’t make it as a professional athlete, so he pursued a career as a professional wrestler and became Dwayne “The Rock” Johnson. He then left wrestling and became one of the highest-paying actors in Hollywood.

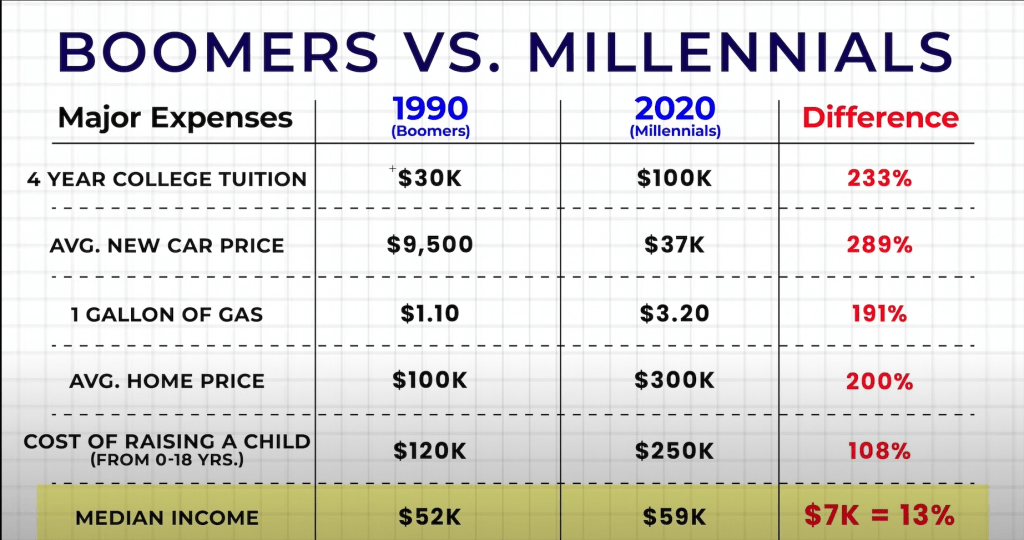

Saving a small amount and investing it long-term could turn into a big thing: A small contribution today could double, and then double after that, and so on. It is like putting Kerosene on a fire that’s already burning. As seen from the chart above, the average American spending on things like tuition, gas, home prices, raising children has skyrocketed over time whereas their income has not. Investing is such a powerful force with compound interest in force, the growth from your investments will likely exceed your annual income by a lot. This statement may seem shocking but it isn’t. Think about this: if you have one million invested, you probably will see more than $82,000 in a combination of dividends or gains from your investments annually. That’s 8.2% growth, not unrealistic at all and below the average rate of return from the stock market. How many hours will that person research stocks? Maybe 1 hour a day or 52 hours in a year. If that same person works 40 hours a week, that’s 2,080 hours in a year to make an annual salary of $82,000. Ask yourself, would you rather have your investments earn you $82,000 annually with nearly zero physical labor, or work for it, not taking account for the time you sit in traffic, get ready for work, and all that extra inconvenience that comes with working. Over time, a $1 million portfolio will grow thus, likely increasing your annual gains at a much higher rate than your salary increasing.

If more people understood the power of compounding, they might invest more: Investing is a powerful force due to compound rates of return. Doubling one’s money throughout one’s life, multiple times, is quite honestly the best chance people have of getting rich. It is possible but many people quite cannot understand it. The majority of us have an incremental mindset, looking at change gradually or step-by-step. An exponential mindset is something harder to understand. Incremental mindset: Average annual return for the U.S stock market since the end of World War II: 11.2%. Exponential mindset: Total return for the U.S stock market since the end of World War II: 270,000%. Incremental mindset: If you had invested $1,000 in Apple stock in 2020, it would be worth roughly double that, around $2,000 today. Exponential mindset: If you had invested $1,000 in Apple stock at IPO, 1980, it would be worth $1 million today.

Not having a defined purpose: People invest to make money, but what is the purpose to have that money? If you haven’t thought about that question, you may not have the motivation to invest. Do you want to buy a lot of stuff? That may not provide what you want. I invest to have more control over my time. It will provide me the ability to do what I want, when I want, as long as I want, with the people that I want. This provides me with the most independence and freedom, which is quite different than wanting more material possessions. And even if you don’t have a specific purpose, there is nothing wrong with wanting more money to protect yourself from the unknown. As Murphy’s law states: “Anything that can go wrong will go wrong.” We never know what the future brings. We all try to have a plan, but we should consider that plan not going to plan. Wealth can be viewed then as a combination of insurance, a get out of jail free card, and Wild Draw Four Uno card all in one.

“Jenner’s multifaceted experience in the fashion industry and the vision she has outlined for the FWRD business has the potential to transform our business and the luxury business as a whole.”

Michael Mente — Co-Chief Executive Officer and Director of Revolve Group from Q2 2021 Earnings Call

“Kendall is the epitome of luxury fashion, and there isn’t a better fit for this position.The world looks at Kendall to lead the industry, and we are beyond excited to have her vision for FWRD come to life.”

Raissa Gerona, Chief Brand Officer of Revolve Group

“A black trench coat is a forever staple–check out more of Kendall’s must-have investment pieces.“

Forward, the premier luxury e-retailer owned by Revolve Group named Kendall Jenner its new Creative Director. This is a brilliant move that increases the intrinsic value of Forward and its parent-company Revolve Group.

You can already get Kendall’s signature look and favorites here.

Revolve group is a powerful data analytics company disguised as an e-fashion retailer. Think a mixture of Amazon and Pinterest. Bringing on Jenner was based as much on data analytics as personality. An influencer for Revolve and Forward needs to showcase its brands and products in a way that depicts a lifestyle of aspiration and luxury. It is a perfect marriage because both Jenner and Revolve Group have roots in the So-Cal lifestyle.

FWRD is one of the hottest growing brands right now. Michael Mente during Revolve’s Q2 earnings on FWRD:

“While momentum has been building at FORWARD for some time, the second quarter was a breakout moment. Net sales increased 151% year-over-year and increased 122% on a two-year growth basis compared to the second quarter of 2019. FORWARD also delivered record gross margins in the second quarter. The strong results underscore FORWARD’s differentiated position in the market as a preferred destination for the next-generation consumers seeking curated luxury offerings.“

The average order value for Revolve is $255. The average order value within Forward is much higher, over $500. I am unsure what Jenner is being paid, but she is worth every penny. Revolve has a very specific strategy that includes:

Optimization of the inventory process

Data-driven performance marketing

Produce on-trend products quickly (trend-forecasting algorithms)

A prominent player in Influencer marketing blending macro/micro-influencers with different strategies.

Develop unqiue brands, which have extremely high margins.

There is tremendous momentum with the FWRD Brand. There is a lot of excitement all around with the companies growth trajectory as a whole. Jenner who is a super-Influencer, will accelerate the companies growth and likely provide a boost towards FWRD’s gross profits. She comes from America’s version of the Royal Family. Among the 10 highest-earning stars on Instagram, her family makes up 30% of the top ten list. Jenner earns $1.05 million per post.

Jenner can move products and create brand power with just one click on the Gram. My conviction for RVLV is high and I am looking forward to the next few earnings reports. I will remain patient and expect big returns.

Lululemon (NASDAQ: LULU) was the one that got away. I have no idea why I never bought the stock. LULU is a company that sells yoga pants/sweat pants and consumers buy them without hesitation for over $100. Believe it or not, the stock price was once less than the price of these pants. Adding injury to insult, I own a few pairs of ABC pants. Wearing these pants feels like wearing sweats, but they have the look of high-end pants.

LULU is a stay-at-home stock and recovery stock. Who would have known it would be acceptable to work Yoga and stretchy pants to work? There is a lot to like about the company’s growth moving forward. Their most recent earnings report was nothing short of spectacular. With great margins and the acquisition of Mirror, the sky’s the limit.

Oatly (NASDAQ: OTLY) is a stock I have strongly considered buying. Sales are up 131% and I drink Oatly regularly. Demand for oat milk is increasing and they have an exclusive partnership with Starbucks. The problem with OTLY is obvious, they are dependent on oats. If the product falls out of favor, the stock will likely suffer. The cost of a 64 oz. carton of Oatly is $4.99 These margins aren’t great and milk is significantly cheaper.

My other concerns with OTLY are depending on your needs and preferences, oat milk is not necessarily healthier for you than regular milk. If oat milk does gain significant market share from dairy, they have significant competition among almond, soy, rice, and cashew milk. Assume even if oat milk is healthier for you than milk, they have to compete with all the other non-dairy milk products. Also is there a consensus in the vegan community that oat milk is the best among all these choices? Margins, long-term demand for the product, and fierce competition in the space are all question marks for me. There is nothing about oat milk I have a high conviction on. Just like a seltzer slowdown, I could potentially see an oats slowdown, especially if dairy can make a comeback.

I will pass on the stock as the company is not profitable yet. To justify a high price, they will need to sustain tremendous growth rates, which I am unsure they can do consistently. Perhaps OTLY becomes a profitable company, there are just too many unknowns n the future for me to invest in. I see better opportunities elsewhere in the market.

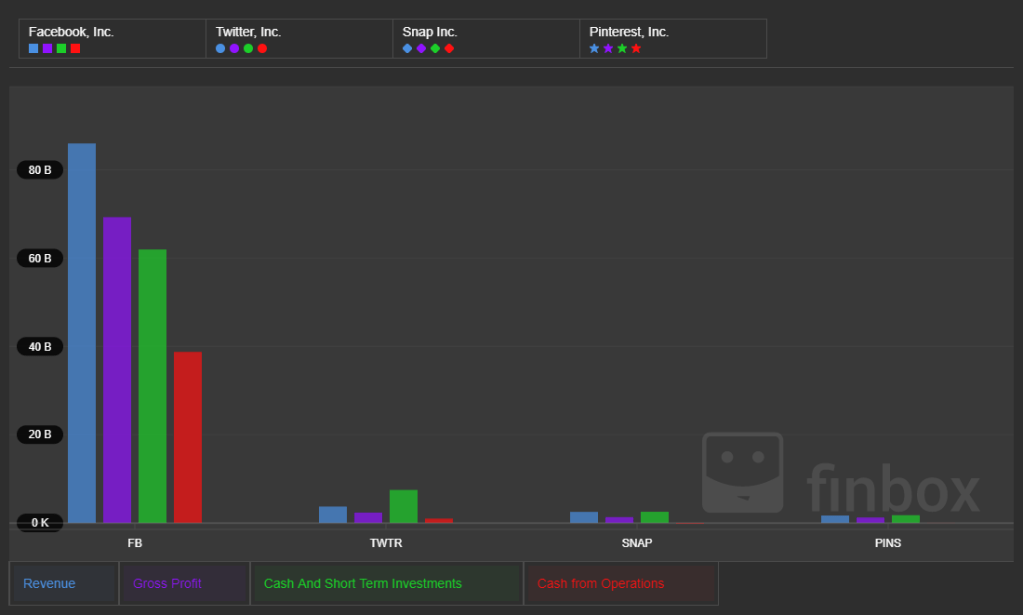

The FB is swimming on $24 Billion in Free Cash Flow and $159 Billion in total assets. They are not going anywhere.

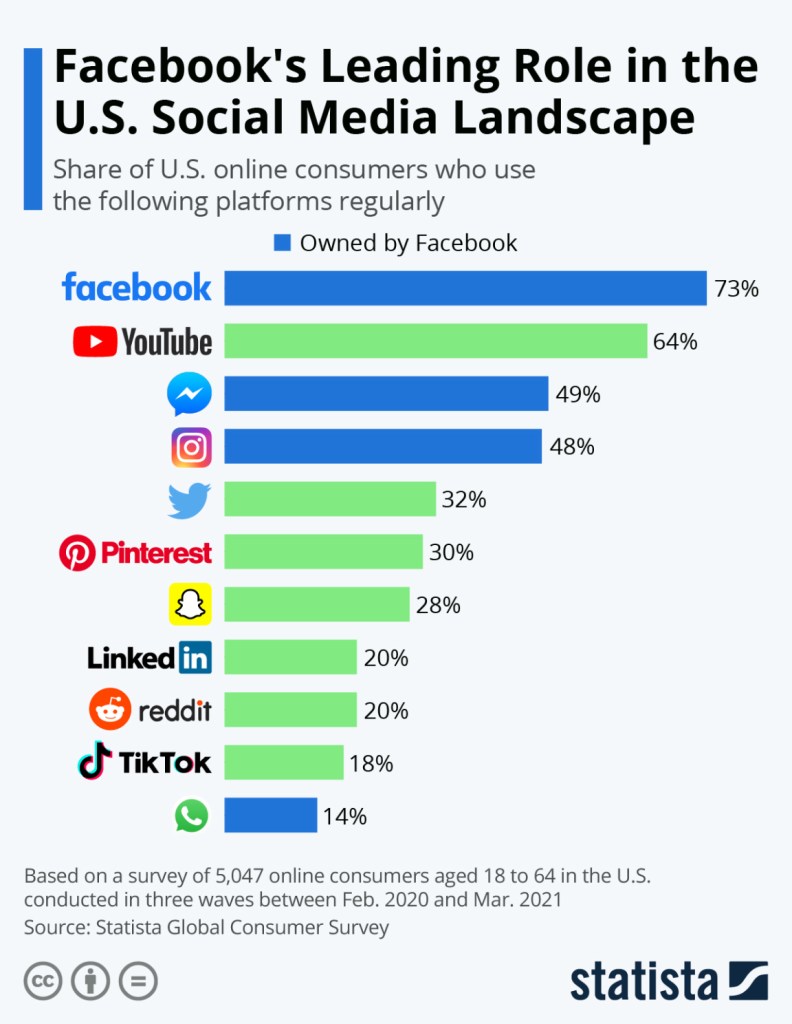

For Social Media sites, there’s Facebook, and everyone else. Facebook has the most active users and cash on hand. If you take out Youtube, which is more of an online video platform, they have nearly lapped all their competitors.

Facebook will remain relevant and on the king’s throne for social media networks this next decade. As for the stock, they are still the best show on the road. You can make the argument that Facebook (the platform) is declining, and maybe it is in terms of popularity, but at this point, it doesn’t matter. Facebook owns Instagram, WhatsApp, Facebook Messenger, and Oculus Rift. They have more cash than their competitors by… a lot. Cash on hand for a company means being able to snatch/pouch the best employees, acquire competitors, buy back shares, expansion, and gain political influence.

“Oh Well Guess You Win Some And Lose Some, As Long As The Outcome Is Income” – Drake, Over My Dead Body

It is important to remember, in regards to stocks, this isn’t a popularity contest, it’s about money and power. The FB may have the most powerful leadership duo in Mark Zuckerberg and Sheryl Sandberg. Sandberg may be the most powerful woman in corporate America. She has been in important meetings with President Obama and Trump. She is a resource smaller companies do not have and cannot afford to bring in.

You can make a really good argument that Snapchat and TikTok are more engaging platforms for Gen Z, however, The FB is still the king of monetization. Popularity, user growth, engagement, user experience are all nice however as an investor, the most important thing is free cash flow and utilizing it.

As a consumer, you may use and like other platforms more, however, answer one simple question, where are you spending your money online? Based on the numbers it is Facebook or Instagram. That’s monetizing on daily active users and advertisers know that.

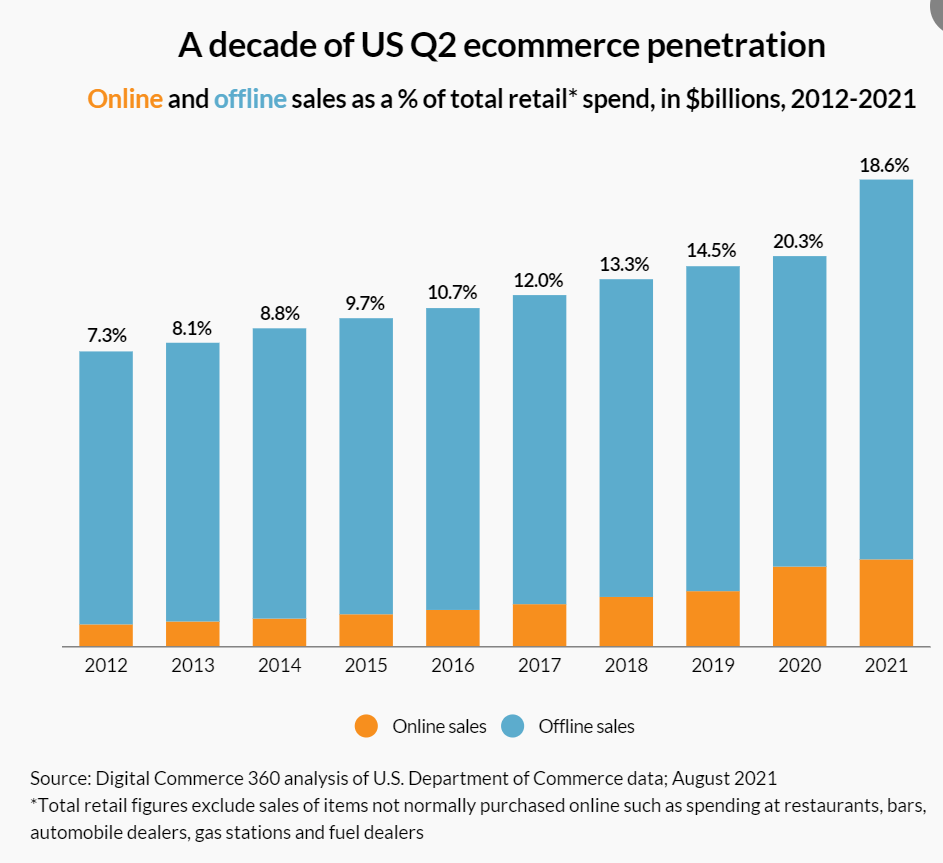

Brief conceptual summary. E-commerce is the selling and buying of products online. E-commerce in 2021 made up 18.6% of all U.S retail sales. If you estimate conservatively, that number should be 25-30% by 2030. If E-commerce is trending up globally (many people don’t have internet service or smartphones yet) it makes sense that more money will be poured into social media influence marketing/advertisements. The number one platform for advertisers to flock towards is Facebook or a platform owned by Facebook.

That’s what makes Facebook so special. They are not niche. Everyone else is trying to establish their lane in regards to demographics and target audience. Facebook attracts all demographics and businesses – young, old, men, women, white, black, restaurants, small businesses, corporations, etc…..

Twitter recently launched Super Follows, a way to generate more revenue for the company. This however should have been done 3-5 years ago. Now their daily active user growth has slowed down. Twitter is not even close to being in the top ten for most overall downloads, App Store downloads, or Google Play downloads. They couldn’t monetize the President of the United States tweeting over 25,000 times, which was a major disappointment as a former TWTR shareholder. I seriously question if their leadership can properly monetize their platform efficiently.

Snapchat & TikTok are relevant for anyone under 35. These are more entertainment platforms. It is questionable if these are effective platforms for monetization and ad money. I like Pinterest most for the secondary players however they are concentrated towards women and niche categories. The average revenue per user for Pinterest is around $5 whereas Facebook’s average revenue per user is closer to $50.

While other companies sent their #1’s, Facebook sent their #2 in a tech meeting with the President. Drew Angerer/Getty Images

I just don’t see tremendous upside in owning shares of Twitter, Snapchat, Pinterest, or Etsy unless their share prices dropped significantly. I am also not interested in a future IPO for TikTok or Reddit. Why worry about owning shares of a company that can barely squeeze money out of their users when The FB does it so effortlessly? I don’t see any immediate existential threats either, and when that does happen, they will have a much bigger cash empire. Like it or not they are here to stay. One of the biggest reasons why I own shares of Bilibili is because Facebook is banned in China. That’s the only way you can stop them, albeit in one country.

Even if Facebook just makes minor tweaks to their platform, it doesn’t matter if their user growth declines. There is nothing illegal about copying your competitors – Instagram Reels/TikTok, Instagram Stories/Snapchat Stories. They have such an amazing balance sheet, they can essentially buy growth. It doesn’t matter if you only log onto Facebook a few times a year. You are still in their ecosystem and most likely in the future, their metaverse. They also don’t need to issue more shares outstanding to raise cash, meaning they do not dilute current individual shareholders. The king still resides in Menlo Park California. I will still hold onto my shares of Facebook because quite honestly, it’s one of the surest things to grow this decade. Their competitors may think they are catching up to with them, but I will finish with a lyric from Jay Z:

Y’all on the ‘Gram holdin’ money to your ear There’s a disconnect, we don’t call that money over here

Mac Jones completed 36 of 52 attempts in the preseason for 389 yards and one touchdown with no interceptions. Eric Hartline/USA Today Sports

In the sports world, Mac Jones was named the starting quarterback of the New England Patriots. Despite the fact he is a rookie with no pro experience, Bill Belichick had enough faith in their first-round pick to release last year’s starter, Cam Newton, a former league MVP. We have no idea if Mac Jones will be the long-term answer at quarterback for the Patriots but even if he does succeed, he will likely go through some growing pains throughout his career. The Patriots liked Jones enough to draft him in the first round with the 15th overall pick. They paid him based on what he could potentially do for them in the future. The keyword is potential. Potential in sports is referred to as upside. Not proven or realized, but in the right situation could potentially be good or even great. Mac Jones might struggle his first year or two, or three, but the Patriots believe he will eventually become a solid starting quarterback.

These 3 stocks present huge potential upside, however, the keyword again, is potential. These stocks aren’t there yet. They all have no price-to-earnings ratios (P/E ratio), meaning they are unprofitable. That’s not uncommon for newer companies. It took Amazon 9 years before having a profitable year. It took Tesla 18 years. Apple almost went bankrupt. Not only are these companies profitable today, but they are also actually among the most financially healthy publicly traded companies you can invest in today. Although the future is uncertain, I believe these companies can eventually become profitable, potentially meaning lots of gains for shareholders who own the stocks in the beginning stages of these companies.

Lemonade (LMND)

Lemonade currently has 1,206,172 customers. They are rapidly growing for a company that was started in 2015.

56% of their business comes from Renter’s Insurance which has a $3.8 billion market size

30% of their business comes from Homeowners Insurance which has a $19.2 billion market size

13% of their business comes from Pet Insurance, which has a 3.62 billion market size.

1% of their business comes from Life Insurance, which has an $886.7 billion market size.

Lemonade is planning to enter Car Insurance, which has a $311 billion market size.

The key to taking away from these numbers is a fast growth, big market opportunity, lots of ambition. Think of Lemonade right now as a small fire. I think it will spread like a wildfire. Some think it will be distinguished. If you want to learn more about Lemonade you can read the founder’s letter here. Ask yourself, do you like your current Insurance Company: State Farm, Allstate, Geico? When I mean like, I mean with a passion or something you care about. Most people I know would say no. How Lemonade does business in the insurance industry is different. I am not saying better or worse, but different. It is making me change the way how I feel about my insurance and the insurance industry in general. Insurance is boring. Part of the reason we discuss certain types of insurance is not by interest, but by the legal requirement to own these products! Lemonade has the potential to be a generational company in its early stages, which makes for quite an appealing investment option. They just entered the Life insurance market and have yet to launch Lemonade Car. Be patient. They are disrupting a big industry so the ride will be bumpy. There are obstacles ahead however this company is just scratching the surface. They could 10x in size and still be a small player in the insurance industry.

Bilibili (BILI)

Cosplayers perform at the Bilibili stand during ChinaJoy at Shanghai New International Expo Center, China, on July 31, 2020. Photo: Getty Images

If you do not know what Bilibili is, it’s basically the Chinese version of Youtube mixed with Reddit, Twitch, and maybe Netflix?

They went from 110 million monthly active users last year to 237 million this year!

Think about this. The average time spent on TikTok is 52 minutes per day. The average time spends on Bilibili is 81 minutes per day.

I honestly have very little doubt Bilibili will see over 500 million monthly active users by 2023. You have a social media/video game platform targeting Gen Z and Millennials in the largest Asian country. To me, Bilibili is a no-brainer and I potentially could see its stock outperform even Alibaba and/or Tencent. The only question is regulatory headwinds but I see that issue being overblown. If you take the fear out of the equation and look at this issue analytically, I am not as worried. A lot of these high-growth Chinese tech stocks are going through a temporary volatile period. In the long-term not much has fundamentally changed. Remember, oftentimes gut-wrenching pain is a necessary feeling for an investor. That feeling of owning a stock during intense fear and doubt can yield the best gains.

Here are two good articles to explain what China is doing recently. The first from Ray Dalio, founder of Bridgewater Associates, and Gabriela Santos, Global Market Strategist from J.P Morgan.

One of my key investing philosophies is to be open-minded and diverse. You can take this as a basic life philosophy. “In a forest of a hundred thousand trees, no two leaves are alike. And no two journeys along the same path are alike.” Paulo Coelho in Aleph.

Be diverse in the companies you invest in. Of course, invest in things you know and understand but don’t ignore stocks outside of your core competency. In 2007, Ulta Beauty IPO’d. As a man, I know very little about cosmetics or nail products. When I mean, very little, I mean almost nothing. I would guess a lot of male investors have the same gender bias that would potentially make them ignore a company like this. If I had done some basic research and invested in ULTA back in 2007, I would be up 1,110.81%

With Chinese Tech stocks I can sense a lot of anti-Chinese sentiment from American investors. America good, China bad, Democracy good, Communism bad. A lot of this is fear-based but also I get the feeling this is related to the growing anti-China rhetoric growing in this country. I don’t want to make this a political discussion but I think there is an indirect link that has caused a lot of investors to dump their shares of Chinese companies or to remain on the sidelines. I simply ask people to ignore sentiment in the short term and focus on the numbers. In my opinion, having no allocation in Chinese companies is financially reckless for a growth investor. It is no different than those that have nothing invested in Cryptocurrency. As an investor, you are capping off your upside which is too safe of a strategy.

Honest Company (HNST)

Jessica Alba, co-founder of The Honest Company (GETTY IMAGES)

Unlike LMND and BILI I do not own any shares of the Honest Company but I am strongly considering adding this to my portfolio.

In a lot of companies, I invest in, it is not an immediate decision. It can take a few months for me to want to invest in an individual company. I am not overly impressed with HNST’s growth, but I am intrigued.

Jessica Alba isn’t just a figurehead for the company. She is a legitimate founder that built the company from the start. She started this lifestyle movement and for her, this isn’t just paid sponsorship. She is the face of the company and a mega influencer who provides an edge over its competitors.

What makes HNST appealing to me is its intrinsic value. The customers care about the company and its products. That’s why they have such positive reviews for their products. You won’t find this in the book value of the company but I think the edge for the Honest Company is its branding and messaging.

The company can speak to Millennial and Gen Z moms in a way Proctor & Gamble and Johnson & Johnson cannot. The consumer base they are targeting is more mission-driven and cares more about the ingredients in the products they buy instead of the actual price. Consumers will pay a premium for this, causing margin expansion. If this company can get into more retailers like Walmart, get their diapers into Costco, an existing retailer they do business with and expand their product line, I think they can become profitable by next year. Luckily for HNST, they aren’t in a winner-take-all marketplace. They don’t need to become the #1 consumer good company to be wildly successful. There is plenty of TAM (Total addressable market) for them to succeed. Similar to how Shake Shack doesn’t need to become the biggest fast-food company to be profitable. If HNST can execute and expand, it can become a highly profitable company in the upcoming future.

I invested in Coach, now Tapestry (NYSE: TPR) in 2016. The company seemed like a solid value play with good growth potential. I liked the direction they were going. At the same time Coach made a $10 million deal with Selena Gomez to become the face of the brand. I thought that was an excellent move because at the time Gomez had 104 million followers on Instagram (now she has 255 million). It was a much-needed deal for a company that seemed to have lost its Je ne sais quoi, or “it factor” that gives life to a luxury brand. You know that “thing” that creates an emotional response and connection with a brand making you want to pay full price for their product instead of buying a discounted version on Walmart.

Although the company seems to have been making some strides the pandemic changed all that and paused everything. I bought TPR again last year as a solid rebound play and that worked out well as the company has recovered nicely. As I review TPR today I am extremely optimistic and believe there could be a growth storm brewing. The company is still undervalued from its Forward P/E and after patiently waiting I could realize massive gains.

(Photo credit: Courtesy of Coach)

The stock has been dead money for almost a decade, I see that changing.

You can find the most recent Q4 earnings report for TPR here and the presentation here The numbers indicate the company is very healthy and growing. 117% revenue growth for Coach, 95% revenue growth for Kate Spade, and 146% revenue growth for Stuart Weitzman. Coach provides TPR with over 70% of its revenue so they are the main driver of TPR’s profits. The fact Kate Spade and Stuart Weitzman are doing well is a nice bonus for the company as a whole.

#1 Digital growth and engagement is key

The company said its online sales rose 35% from a year earlier. This was mainly driven by Coach, which drove over 55% of the digital growth. Coach is executing on their social media presence and e-Commerce channels in a big way. Coach has 5.4 million followers on Instagram which is surprisingly more than Revolve (NYSE: RVLV), a pure internet retail play. They have several TikTok campaigns which are rapidly creating buzz and new customers. Female Gen Zers and millennials are driving the growth and revitalizing of this 80-year old company.

I am extremely bullish on e-Commerce, specifically social media marketing. This is the future of the fashion industry. Digital growth has better margins than brick-and-mortar growth. If Tapestry can continue to execute on its digital growth, it will see more customers, maintain high margins and increase its brand integrity. When listening to interviews from the CEO of Tapestry, Joanne Crevoiserat, I am hearing a lot of the same verbiage that I hear from another company I am bullish on, Revolve. This is absolute music to my ears. Even just recently I viewed TPR as simply a recovery play that would get a nice boost as the pandemic eased up. Now I see TPR more like a true growth stock disguised as a value play.

#2 Brick-and-Mortar still matters and Tapestry is innovating their stores

Last year Coach opened its first digitally immersive store in Shanghai China, the IAPM mall. These are stores that use digital interactions leveraging virtual reality (VR) and augmented reality (AR). This is all connected to their Acceleration Program for Profitability which they announced last year. Tapestry is focused on delivering on its omnichannel and making a better experience for the consumer. From my viewpoint Tapestry’s strategy is a mix between Apple and Starbucks and so far it looks like it is working. Create appealing products, deliver a seamless consumer experience physically and digitally, strengthen the brand by making consumers care about them again.

#3 Expand in China

Sales grew over 60% in China. 62% of its revenue comes from North America whereas 19% from China. I eventually see the makeup of revenue 50% North America, 25% China, 18% other Asian countries, and 7% the rest of the world. For Tapestry to grow it will need to continue to penetrate the China market. China has an enormous middle-class population and Tapestry’s products are geared toward them. The sweet spot of a luxury handbag for someone in the middle class is about $400-600. Not $2,000-4,000. I have confidence they will carve their lane in the middle-class luxury demographic and who knows, in the future, they may have enough brand strength to compete with Louis Vuitton, Dior, or Prada.

#4 Simply Execute.

Victor Luis was the CEO from 2014 to 2019 and he failed to restore the brand. Jide Zeitlin resigned after 1 year due to personal misconduct allegations. That entire situation was odd, to say the least. Zeitlin, once nominated by Barack Obama to be a UN Ambassador was accomplished but had no real fashion background. Regardless, they seem to have hit a homerun with Crevoiserat, the CEO since October 2020. With stable leadership hopefully, they can take advantage of the talent they already have. Stuart Vevers has been the creative director at Coach since 2013. From most reputable people covering fashion and style, Vevers is a savant. He is very talented however it is hard for his work to shine if management cannot execute. Just like a master chef will suffer if given bad ingredients or incompetent staff. It seems they have figured it out. The truth is a lot of fashion retailers have actual plans in place towards profitability and shifting digitally. It’s really about executing on that strategic vision. That’s on management.

(Photo credit: Courtesy of Coach)

When you put a cake in the oven, there is no guarantee it will come out fully baked. A lot of things can go wrong. I view Coach as being many failed cakes the past decade. A lot of “almost there” and “close” but not complete. I think whatever is in the oven right now though, I think they got it right this time. I bought more shares of TPR recently, even with the stock being up significantly from last year. Despite the 1-year gain, the stock has been stagnant the past five years and lagging behind its peers.

Coach has been performing well in 2021. They brought in Jennifer Lopez as the new face of the brand. The Coach Pillow Tabby is trending on TikTok. The fashion world is believing in Coach again. Female Gen Zers and millennials are spending money on Coach handbags again in a significant way. Despite this, the stock is still undervalued. I don’t believe Wall Street has fully caught on to this story as the cake is still baking. When the story changes from simply a recovery open to a high-performing transformative global technology company, the stock will reach all-time highs.

The Psychedelic industry is growing rapidly. This year I have invested in Psychedelic stocks, specifically Mind Medicine (MNMD) and COMPASS Pathways (CMPS). I understand the biotech sector is risky. The majority of drugs, like 90%, do not reach approval by the FDA. That being said, any successful investor needs to take at minimum a small measured risk in their portfolio. I believe these stocks or other companies in the psychedelic sector could potentially 10x before the end of the decade.

My thesis: Psychedelic treatments can be part of the solution for treating depression, PTSD, addiction, etc.

The idea of psychedelics being used to help with mental health therapy is not new. There are enough studies and research that show it can be viable. Kevin O’Leary, most famously known from Shark Tank laid out his opinion here. I pretty much agree with almost everything Kevin said. There seems to be a lot of institutional money flowing into the psychedelic sector. Whereas cannabis seems more focused on recreational use and politically charged, psychedelics are about medicine and science. If you google Psilocybin, Ketamine, or Psychedelics, see how the search results differ from Cannabis or Marijuana. Psychedelic news seems more concentrated whereas the latter is kind of all over the place.

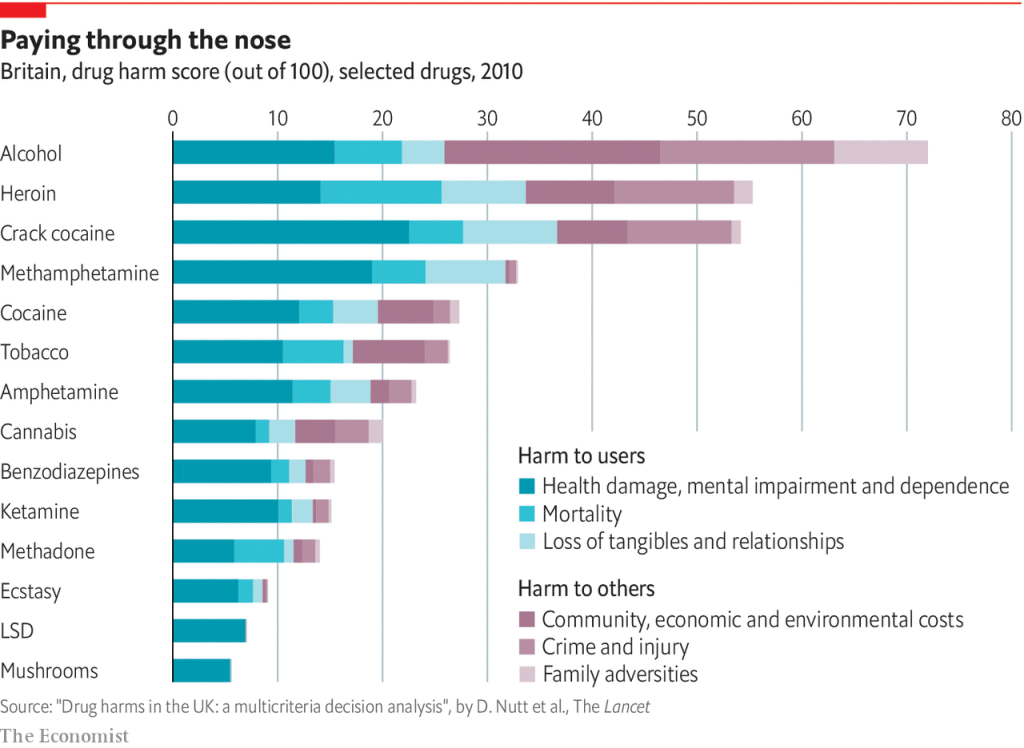

What also makes psychedelics an attractive option, is its relatively low drug harm score, particularly, harm score towards others, even compared to cannabis. Given this information, I think the pathway towards legalization and marketization will be a lot easier than it has been for cannabis, thus removing the barriers to profitability.

Thesis #2 The need for psychedelic treatment is growing due to an emerging mental health epidemic.

The #1 domestic issue for America is health care, and that was even before the pandemic! Mental health is linked with health care, and a lot more people are suffering from anxiety and depression. This problem has only exasperated because of the pandemic. I think the vast majority of the population would agree with this, however, we do not have enough viable solutions being offered. Nowhere even close. This seems to be an issue we kind of just sweep under the rug until the next mass shooting happens. We talk about addressing it, and then….. nothing happens, repeat cycle.

My experience:

I have volunteered over 230 hours as a Crisis text Counselor in 2020. I had over 1,000 conversations with people seeking help. I can tell you from my experience, mental health is a problem and getting worse. Collectively as a nation, we are so woefully behind in finding viable solutions, the problem is likely to get worse than it is better. Consider that many people think mental health is not an actual medical problem, just a temporary weakness that shouldn’t even be discussed, not even among family members. Given how serious this issue is, I believe psychedelics as a whole, will eventually make up a big space in the biotech industry.

At some point, mental health will become too much of a problem to ignore and our government will have to throw a lot of money into addressing the issue just like they did Covid-19. A practical solution would be a commercial low-dose psychedelic prescription drug. I don’t anticipate this to be a very partisan issue. Demand for such a product is already high because the marketplace has such a low supply of viable solutions in treating mental health issues. As we have seen with vaccines lately, if the problem is big enough, and there is enough willpower, we can speed along the process in getting solutions out to the public.

In Conclusion:

I have used psychedelics in the past. So did Steve Jobs who said, “Doing LSD was one of the two or three most important things I have done in my life.” So did the founder of Alcoholics Anonymous Bill Wilson, who believed LSD could help treat alcoholism.

I don’t know how to put in words how psychedelics affected me or how I felt. Based on my experience I felt an altered form of consciousness. In a controlled safe setting I could see how it could help someone with mental health issues or addiction.

I am not a scientist. I am not a financial advisor. I know biotech companies are risky. These companies pretty much live on binary events. Based on my experiences and the scientific research that has been conducted, I think psychedelic stocks in general, have something worth investing in.

This story could take years to play out however as retail investors we have a major advantage over fund managers and analysts. We don’t have to focus on short-term profits. I am fully content having this section of my portfolio in the red before the actual story materializes. The research has merit and the problem is big enough that even a mediocre solution could cause this sector to expand dramatically.

We are still in the beginning stages of this journey. I am personally rooting for success in this industry and so should you. Mental health and addiction are such serious issues that have an extreme negative cost on our economy. It is such an overwhelming topic, we don’t even talk about it in depth because solving it seems impossible. In regards to an investment opportunity for me, this is a trip worth taking for the long run. I believe it will go from a speculative industry to a legitimate billion-dollar industry. Those companies on the forefront right now could reap major rewards.