Randominvestorhttps://investinmyselfcom.wordpress.comThis is my personal blog about finances, the stock market, and investments. Disclaimer: I am not a financial advisor. Take anything I say for entertainment purposes only.

“Artificial Intelligence, Leonardo da Vinci drawing style,” an image NVIDIA’s creative team created using the Midjourney AI art tool.

I really like Nvidia. This company amazes me with what it can do. It blows my mind.

What many investors underestimate about Nvidia is its importance to technology. Nvidia is to technology what the fire hose is to a fire department.

Nvidia’s GPU tools are used as digital shovels for crypto miners.

Nvidia’s A100 chips are now the engines used to train ChatGPT and other generative AI.

With any new technological advancements or innovations come new markets and revenue drivers. Whoever the winner in the space is, Nvidia will be there. The players’ names and buzzwords may change, but Nvidia will be there.

Self-driving cars

The Metaverse

Autonomous robots

That’s why you cannot just look at a balance sheet and value Nvidia properly. Their growth potential is nearly limitless. The free cash flow for Nvidia can double in a year. Nvidia’s technology is powering the next big thing you cannot forecast.

The big secret about Nvidia is that it will always be overvalued at any price. You invest in a company like Nvidia for 2028 and beyond. The company and what drives its revenue will likely be drastically different in the future. As an investor, if you do not like roller coasters, there are calmer rides to get on. Nvidia is a high-quality technology company, but its sector is volatile. AI is fast-moving. You cannot map it out in a DCF model. You aren’t valuing Starbucks or Visa. Artificial Intelligence Computing isn’t slow-moving or predictable.

When the stock price falls, you give them the benefit of the doubt, like if Stephen Curry were to go on a long cold shooting streak. The bounce back is inevitable. I am not saying to go out and buy the stock right now, but when you invest in Nvidia, you are investing in a best-in-class company.

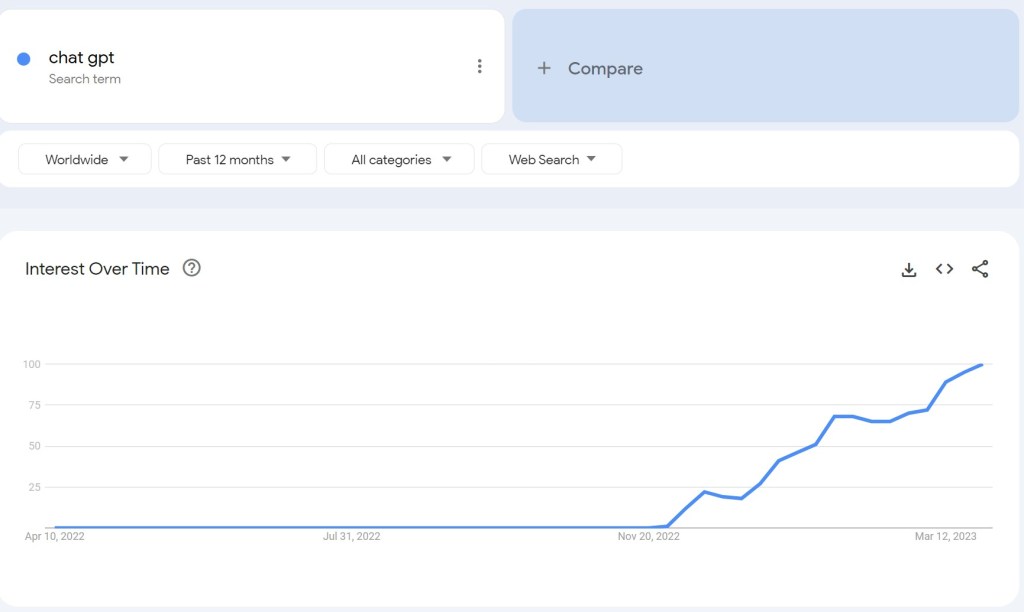

Interest in Chat GPT was not even on the mainstream media radar until December 2022.

Analysis of technological change requires imagination and the ability to quantify unknowable wonders. You will not find this in most financial market analyses. Just remember how often Chat GPT was discussed on Bloomberg or CNBC six months ago.

America will continue innovating based on four factors:

Moore’s law: the theory that the number of transistors you can fit on a microprocessor doubles every two years.

Koomey’s law: the theory that the energy efficiency in computing doubles every two years.

Kryder’s law: the theory that the amount of data you can fit in one inch of disk drive doubles every 13 months.

Shannon-Hartley theorem: As long as you can create channels with greater bandwidth, you can transmit information more clearly and faster. The more bandwidth, which is theoretically unlimited, the better.

Most of America’s tech industry revolves around these four rules. Eventually, when these wind-down, new advances will take place, driving innovation and efficiency further.

With Nvidia, I stress patience. The company was founded in 1993 and nearly went bankrupt in 1999. Owning the stock in the early 2000s may have felt like owning an overpriced gas-guzzling car.

But patience did pay for early investors. Owning $1,000 worth of Nvidia stock back then would be worth over $9,000,000 today. That’s why my investing philosophy consists of holding stocks for the long term and holding them for dear life. Long-term investing consists of holding stocks during bad times and when everyone says it is overvalued. This strategy awards patient laziness. The longer you hold, the bigger your reward.

The buy-and-hold strategy may lack intellectual sophistication, but it works. Wall Street tends to look only 14-28 months out. The average retail investor has an even shorter window. This short-view investing window will not net you 3,000% or more gains.

Salesforce iPod in 2004, and analysts said its P/E ratio was “too high.” The stock has increased more than 30 times in value since then.

People sold out of Google stock in 2009 because its valuation was “too rich.”

People sold out of Amazon in the 2000s because the stock was “too expensive.

If you want a company that optimizes growth, you look at Nvidia. Companies that favor growth are making riskier future bets that may or may not pay off, but when they do, and in a big way, they become the envy of Wall Street.

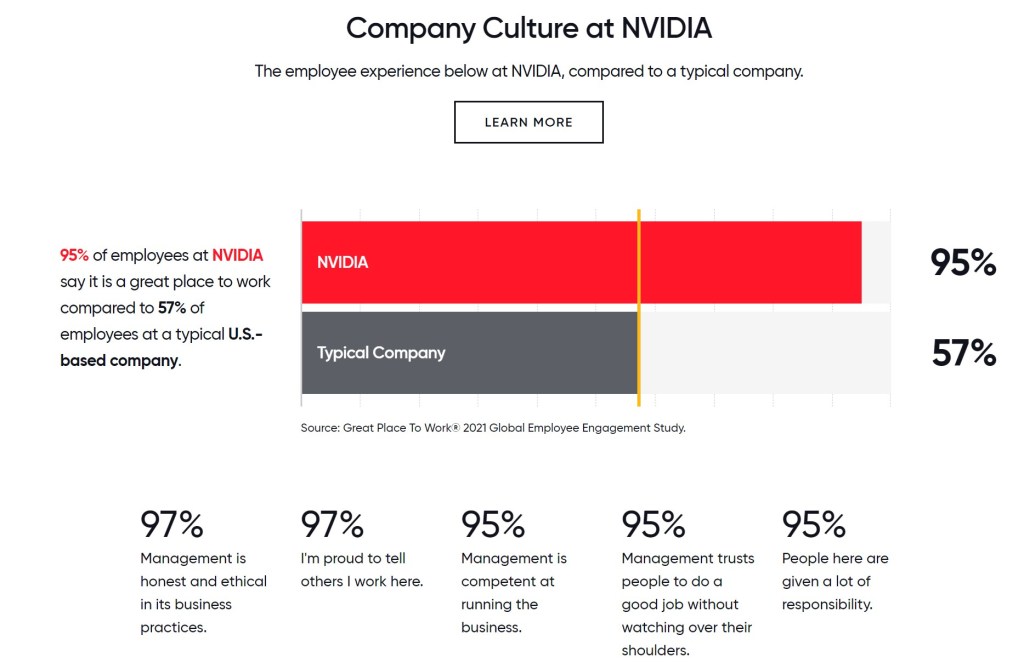

Lastly, I trust Nvidia because I trust Jensen Huang. As long as he is the CEO, I will hold the stock. Huang is an excellent CEO because he sells you on substance, not style and flash. Huang isn’t the best orator or salesman. He’s a hard-working guy who cares deeply for his company and employees.

Nivida is considered one of the best public companies in how they treat their employees, customers, and shareholders. Their employees are loyal, passionate, and dedicated. Huang preaches celebrating failure and intellectual honesty. Many tech companies take too little risk. You will be stuck in the mud if you fear taking risks. Many companies embrace risk, but many of those companies’ CEOS have a pie-in-the-sky mentality.

Jenseng demonstrates a great deal of emotional intelligence. He comes off as incredibly grounded yet relatable:

“I was a very good student and I was always focused and driven. But I was very introverted. I was incredibly shy. The one experience that pulled me out of my shell was waiting tables at Denny’s. I was horrified by the prospect of having to talk to people. You want customers to always be right, but customers can’t always be right. You have to find compromises for circumstances that are happening all the time and you have difficult situations. You have mistakes that you make; you have the mistakes that the kitchen makes. You can’t control the environment most of the time. And so you’re making the best of a state of chaos, which was a wonderful learning experience for me.“

A CEO like Huang is built for tough times. He understands how to navigate a company during turmoil and press the gas during a boom. I am confident he will lead Nvidia to a $1 trillion market cap as the growth story for Nvidia is still early. Buckle up and enjoy the ride up.

I listened to Raissa Gerona, the chief brand officer of Revolve, on the Glossy Podcast. I had never heard of the Glossy Podcast before, but it looks worth following on Spotify. Since Revolve is the biggest position in my portfolio, I would like to give my thoughts on Revolve before the Revolve Festival.

I recommend any shareholder of Revolve listen to the episode. It was very informative and gave a good primer on the state of the business.

Influencer marketing is still early.

Influencer marketing may seem oversaturated, but it’s still in its early stages and has doubled in size since 2019. The bigger the market grows, the better it is for the business and the stock. This type of marketing allows companies to engage with their customers on a personal level. User growth for Instagram and TikTok is expected to be steady for at least five years, so I don’t see any cause for concern about this form of advertising in the next decade.

“As someone who’s worked there for 11 years, it gives me peace of mind knowing that we have very senior leadership that understands the ebbs and flows of the business, and that’s gone through multiple recessions and obviously Covid — we’ve never experienced anything like this before. In 2019, we were doing $500 million in [annual] revenue, and then we just crossed $1 billion in revenue in 2022. “

The threat of TikTok being banned in the US is real, but Revolve has a strong presence on Instagram and YouTube shorts. If necessary, they have the team in place to pivot to where their customers spend most of their time.

The festival will have a fifteen-foot sunken UFO – whoa!

Looking at Revolve long-term, I see them opening up a flagship store in Los Angeles within the next five years. They should prioritize international expansion, Web3, and men’s wear. If a strategic acquisition target is available, they should pursue it more aggressively. 2023 is a good year to take on more obligations if it leads to meaningful future growth. Valuations for buyers are much more attractive than in the past few years.

Overall I see Revolve in a good position. They have a loyal customer base, and I see them capturing more female gen z clients, especially those born after 2000.

Free Cash Flow Problem?

Revolve’s Free Cash Flow influx mirrors that of Amazon. Revenue was up for these companies, and free cash flow was down.

Free cash flow is the cash from operations minus capital expenditures. Although free cash flow was down due to increased CapEx, these investments in brand marketing and fulfillment centers will produce a positive ROI. Forgoing profits for growth and expansion is a winning strategy in the long term. I would rather see a company invest than sit on cash. When the economy improves and demand returns, those investments will likely pay off and be reflected in the balance sheet.

Stock price vs. Intrinsic value.

The stock price of Revolve is publically available for anyone to view. The intrinsic value of Revolve is subjective, based on qualitative and quantitative factors of the business. I always go back to the great quote from Benjamin Graham: In the short run, the stock market is a voting machine, in the long term, it’s a weighing machine. This means that in the short term, the stock price may be influenced by sentiment, news, and market trends, but in the long term, the stock price will reflect the true value of the business.

Many investors, even good ones, make the mistake of following the stock price and letting the price movement dictate their thinking on how the business is doing. Like other e-commerce platforms, Revolve is currently mispriced and undervalued. Growth companies, particularly in e-commerce, are often grossly overvalued or undervalued based on future free cash flow.

Netflix’s stock price hovered around 175 in the summer. In March, it was trading at over 345.

Meta’s stock price hovered around 90 in November. In March, it was trading at over 200.

Nvidia’s stock price hovered around 145 in December. In March, it was trading at over 275.

Based on the stock price falling dramatically last year, you would think these three companies were distressed. It is hard to believe the intrinsic value of these three large companies changed that much in a few months.

The stock price dictates public sentiment, but the intrinsic value can take a while to metastasize and reflect for shareholders. It would help to ignore the noise because most stock analyses and commentary you see daily do not matter.

How I view investing:

The intrinsic value of Revolve is worth at least 100. Will that be reflected in the stock price? It will likely happen before 2030. Thus, I have never sold any positions I have accumulated over the past four years. That’s the bet I am making.

I can live with the stock price going to zero (unlikely). That’s the risk of investing. The good news is that is the worst-case scenario, or is it? What’s worse, buying a stock and watching your investment go to zero or buying a stock, doing the research, having the conviction, but selling too early and watching the stock generate 100x or more returns. The latter scenario for me is the worst-case scenario. Ask investors who held Amazon in the 2000s but sold because the stock was “too expensive” or those that sold Google in 2008 because the P/E ratio was “too high.”

Investors will make a lot of mistakes. People make a lot of mistakes in their life. 99.9% of them, you can recover from them. With a losing investment comes a lesson to learn. The biggest tragedy in investing comes from missing out on gains in something you believed in but didn’t have the patience in to reap the rewards. That would be a deep regret of mine.

Great investors will fail. With great success comes failure.

LeBron James has been to the NBA Finals 10 times. Six of those times, his team lost.

Tom Brady has been to the Super Bowl 10 times. Three of those times, his team lost twice to Eli Manning and once to Nick Foles!

Aaron Judge hit 62 home runs in 2022 and struck out 175 times that season.

Success comes with failure, but if you succeed enough times, those failures don’t become deep lifetime regrets. That’s why I am not a big fan of index investing. Index investing still carries risk but produces muted gains. The entire mantra of index investing is that active investing is too hard or unpredictable, so you shouldn’t try. I’m afraid I disagree with that philosophy; it would be like saying dieting is too hard, so you should take diet pills or supplements instead of trying to eat healthily.

I expect Revolve to be a big-time winning investment. I bypassed other lucrative opportunities like adding to my Amazon position or starting a new position in Lululemon and Louis Vuitton. Will it pay off?

Based on my research, I believe Revolve has a solid competitive position in the fashion industry and strong growth potential. Their focus on influencer marketing and customer engagement through social media has been successful and will likely continue to drive growth. Revolve is a good investment opportunity for those interested in the fashion industry and the potential growth of influencer marketing. While the stock price may fluctuate in the short term, I am optimistic about the company’s long-term prospects and see them as a strong player in the industry.

2020 and 2021, due to mainly the pandemic, were not standard years and must be considered anomalies. Those numbers might be a glimpse into the long-term future but not something you can expect in the next few years. 2022 although a lousy year with rising interest rates and the Ukraine conflict, should be considered a typical business year.

For a company like Revolve, compare their numbers from 2022 to 2019 instead of the last two years. 2022 was a bad year for the economy, whereas 2019 was a good year. If the crucial numbers like revenue, sales, active customers, and average order value in 2022 are better than in 2019, that’s a strong sign the company is doing well. If the opposite is true, that could be a sign the company is going in the wrong direction.

That’s how I look at growth companies. Revolve for 2022 had almost doubled the number of active customers, total orders placed, and net sales from where they were in 2019. With nearly twice the number of orders, the average order value has increased, a sign of a strong brand.

Bottom line: The 2022 numbers for Revolve are above the 2019 trendline.

Not everything is rosy. Some of the numbers are pretty bad. Macroeconomic issues hurt Revolve as they are not immune to inflation or rising gas prices.

When prices increase, consumers decrease their spending on non-essential items like apparel. There is no question Revolve will suffer, but I predict it will weather the storm of an economic slowdown better than its competitors. Before the pandemic, companies like Nordstrom, Macy’s, and H&M struggled. These high-end department stores have a laundry list of problems. Take Nordstrom, for example. They offer nearly a 4% annual dividend yield, which siphons funds to shareholders. This only makes sense if the business is healthy. This type of dividend for a struggling business is the equivalent of an unhealthy person donating blood. The old guard has a bunch of debt, stores, and employees. Revolve has none of these financial obligations, where its profits go straight towards fortifying its brand and investing in its logistics.

Strong Brand leads to Customer Loyalty + Consistent demand/Profitability

Revolve has Pricing Power. With PP, you can sell items at full price but avoid any long-term inventory glut

Revolve will emerge as a big-time winner and an industry leader when the economy improves. Like a high-end jewelry brand, Revolve will have consistent profitability, pricing power, and margins. The stock will be a hero based on the brand alone. If they continue to improve their digital infrastructure, it will allow them to create a deeper connection with their loyal customers and eventually create a cost advantage. If Revolve can replicate the Nike playbook, the stock will 10x relatively quickly. The stock remains a solid long-term hold.

One must go on working silently, trusting the result to the future.

Vincent van Gogh

Where does one start to become an investor? The pathway is not straightforward or a step-by-step process like other “careers.”

To become a doctor, you typically news to follow a specific pathway:

Earn a bachelor’s degree.

Earn a medical degree or osteopathic degree.

Pass licensing exams.

Complete a residency program.

Complete a fellowship program.

Pass all necessary exams.

Obtain a medical license.

Continuously renew license renewal and participate in continuing education.

To become an investor, you typically need the following:

Open a brokerage account.

Buy an investment.

Sell an investment.

There are a lot more steps in how to be a real investor. I’ll add some helpful steps and advice.

Investing is more behavioral than a skillset.

Successful investing does not require a high I.Q. or extensive education. Patience, memory, and observational skills are needed to be a good investor. Investing should be viewed by probabilities and not possibilities. In the long term, investing is like a casino where the statistical chances are in your favor. In the short term making predictions is more like roulette.

Some people think the behavioral aspect of investing is mobo jumbo, but ask yourself why the average holding period of stocks is just six months or less. How does an investor go from being a full-fledged long-term investor to selling your entire portfolio based on CPI data or spy balloons? You have probably heard the famous Warren Buffet story: Amazon founder Jeff Bezos once asked Warren Buffett: “You’re the second richest guy in the world. Your investment thesis is so simple. Why don’t more people just copy you?” To which Buffett replied, “Because nobody wants to get rich slow.”

That’s why I do not look at investing as a skillset but as a process that you need to experience firsthand to understand fully. If you are a parent, try asking someone single how to raise children. Almost anybody can provide the textbook definition of parenthood, but you will likely only understand it contextually once you become a parent yourself and experience it firsthand.

Long-term investing is a highly probable winning strategy that requires investors to witness massive downward spirals in their net worth. How one handles it is based on temperament rather than logic.

Finances are personal.

For many people, money is more uncomfortable than sex, politics, and religion. That could explain why so many Americans do not talk about finances and likely contributes to why we are so bad at managing it.

In investing, you are not in competition with Bill Gates, Elon Musk, or your rich neighbor. Your biggest enemy for finances is often the thoughts in your head. Like maintaining a healthy lifestyle, one must personalize investing to your goals and needs. Everyone has different diets and lifestyles. There is no best way to invest because everyone handles volatility and risk differently.

Investing has always had an undeniable link to luck.

Doctors, engineers, or professors do not want to hear this. Intelligence may hurt you as an investor. The truth is the janitor is on even footing with the brain surgeon working at the same hospital. Investing isn’t a high-IQ game. The technical skillset required to be a brain surgeon doesn’t translate to successful investing. The janitor can succeed if he has the correct behavior and mindset. Ask Ronald Read.

Investing is a game of probabilities, but even doing the right thing can cause you to lose money. Going all-in with a full house is statistically the right decision, but it gets beat by a royal flush every time.

Daily stock movements are unpredictable, yet analysts try to make sense of these movements, even marginal ones, with near certainty. Stock prices act like a roller coaster or whipsaw. Instead of trying to analyze the minutiae of volatility, I like many others, preach long-term investing. It puts the probabilities in your favor, and you avoid external noises.

From my observation, I see two significant problems really “smart” people are doing in the market. First, people need to focus on the goal of investing: making money. The stock market isn’t a place to make ideological statements or boast about your ego. Politics and religion are an endless black hole because there is never a clear winner or loser. There is nothing wrong with having strongly outspoken beliefs, but it has no place in your portfolio as it provides no competitive advantage in the financial markets.

Secondly, many intelligent people in the market make dumb decisions because of arrogance. There is a thin line between confidence and arrogance. Many smart people fool themselves by thinking they know things that are not knowable or predictable. Having vast information or research knowledge doesn’t translate to bigger returns. The most intelligent person in the room isn’t necessarily the one with the healthiest diet or the most successful financially. One of the best examples of a smart guy outsmarting himself and making a lousy decision is Steve Jobs, a brilliant entrepreneur who died too early, most likely because he couldn’t follow the advice of his doctors.

Simplification over Sophistication.

“The greatest enemy of a good plan is a dream of a perfect plan.”

Carl von Clausewitz

“The simplest solution is almost always the best.”

Occam’s razor was named after 14th-century logician and theologian William of Ockham.

How many people know all 613 commandments from the Old Testament? The majority of people remember only the first 10. You can even simplify the Old Testament as loving your neighbor as yourself.

Having a simple investing strategy is often the best strategy. Higher education rewards complex ideas and theories, but investing is a different animal.

Many successful investors would agree on the benefits of simplification, and most importantly, it keeps you sane. When you are confused and scared, you are more likely to make obvious mistakes. Even a small amount of anxiety can choke a vast amount of intelligence.

Outside of a rough snapshot, I don’t care about GDP, industrial production, retail sales, consumer spending, manufacturing outputs, imports, exports, etc. I tune out the noise. I am not an economist. I am an investor. The majority of economic data releases are non-factors. Even quarterly earnings reports are sensationalized as big events with significance and importance. Trying to make sense of all this is maddening and fruitless.

Understand how consumer behavior works, and find companies that generate free cash flow. Companies that can reinvest that free cash flow and expand the value of the enterprise in the future will likely be big winners.

Find order within chaos or stand still within a fire. Life is endlessly confusing and agonizing. Those that can maintain homeostasis within chaos will be the most successful.

Passive investing should not mean set it and forget it.

I recommend all investors watch 1-3 hours weekly of more traditional finance news channels like CNBC and Bloomberg. Watching too much financial news is a time-waster, but you at least must understand the general sentiment of retail and institutional investors and learn Wall Street vernacular.

Like how doctors participate in continuing education, investors should try to continue their education. Read or download an audiobook every quarter. I would avoid “How To” books about day trading or getting rich. Anything from Peter Lynch, Kenneth Fisher, and Joel Greenblatt are all winners.

You can explore less traditional sources for investments like youtube or Reddit once you are grounded with at least a base of solid financial knowledge from people that know what they are doing.

Balance is everything in life and investing.

A great investor must find a balance between obsessively looking at their portfolio daily and being too passive.

Have confidence but not arrogance.

Have a plan but be flexible and open-minded.

Investing is an art and science; you need to find the balance. Like improving your overall health, no one needs to run 5 miles daily to maintain fitness. It’s also okay to occasionally eat cookies and cakes, but not overindulge.

It would help if you had balance because it’s an assortment of uncertainties regarding investing and the economy. The dilemma in financial markets is that people are suckered into those who speak in certainties rather than probabilities. Certainties do not exist legally in the stock market.

It is okay to make mistakes.

“The risk of a wrong decision is preferable to the terror of indecision.”

Maimonides, Jewish Rabbi

Warren Buffett once said he’s owned 400 to 500 stocks during his life and made most of his money on 10 of them. Charlie Munger followed up: “If you remove just a few of Berkshire’s top investments, its long-term track record is pretty average.”

It is okay to make mistakes in investing, a lot of mistakes. Evaluating stocks from good vs. bad companies to cheap vs. expensive is subjective, and the odds are not in your favor to be right all the time. In investing, precise answers are not realistic or possible. Besides making money to achieve that goal, you need to learn from your mistakes and minimize them.

Everyone needs to create some room for error because if you have a long enough time horizon, the odds increase of a low probability infrequent event from happening. For company x to go from price y to price z, it cannot be predicted accurately in a flow chart.

Think exponentially.

Most of the writers portrayed an expansive future. But not George H. Daniels, a man of authority at the New York Central and Hudson River Railroad, who peered into his crystal ball and boneheadedly predicted:

It is scarcely possible that the twentieth century will witness improvements in transportation that will be as great as were those of the nineteenth century.

Elsewhere in his article, Daniels envisioned affordable global tourism and the diffusion of white bread to China and Japan. Yet he simply couldn’t imagine what might replace steam as the power source for ground transportation, let alone a vehicle moving through the air. Even though he stood on the doorstep of the twentieth century, this manager of the world’s biggest railroad system could not see beyond the automobile, the locomotive, and the steamship.

Three years later, almost to the day, Wilbur and Orville Wright made the first-ever series of powered, controlled, heavier-than-air flights. By 1957 the USSR launched the first satellite into Earth orbit. And in 1969 two Americans became the first human beings to walk on the Moon.

The world in the future will look drastically different from the world today. Compare 1923 with 2023. No one can accurately predict the future, but that doesn’t mean the future will follow a linear, step-by-step progression.

The problem with being really smart is that you can often think you know better than everyone else. Notice how the future is often forecasted with linear thinking, but when we look at history, it is driven by exponential, low probabilities events. How is history a description of impossible events becoming possible, yet you will hear future forecasters lay out the future in a predictive map?

A successful investor needs to have an exponential element in their portfolio. If your entire portfolio consists of index funds, you are either selling yourself short or fooling yourself with a false sense of financial security. There is no need to sacrifice your gains when you don’t have to. Index funds are the equivalent of accepting a plea deal when the risk of conviction is low.

As an investor, you must look at investing ideas as a scientist. Take other views and opinions, put them in your laboratory, and see what works.

Stop with Groupthink.

I always voted at my party’s call, And I never thought of thinking for myself at all.

H.M.S. Pinafore: When I Was a Lad Song by Arthur Sullivan and William

Groupthink, or investing based on a consensus, is one of the investors’ most common mistakes. Investing isn’t a consensus-building activity; it is an individual game like chess or golf. You will likely get mediocre results if you approach your portfolio as a politician approach legislating.

The greatest thing about investing in your portfolio is that it’s yours. You can do whatever you want. It reflects your personalized goals. You can invest as much or little, heavily diversified or concentrated; it is up to you.

In politics, the goal is not to be an outlier. Politicians need safety in numbers to get bills passed. When you lose the numbers, you lose job security. In almost any job, you must accommodate and compromise your wants with the employer’s needs to stay employed. The financial markets are a different beast. The more ambitious your goal is, the more you want to be an outlier. In running your portfolio, you are the boss and reap all the gains. You cannot be a long-term investor and follow groupthink/consensus because, eventually, the sentiment changes. If you can’t think for yourself, you will betray your goals and principles.

Obtaining and maintaining wealth can be summed up in two principles.

Delayed gratification and having fewer wants than needs.

If you haven’t heard, Coupang is the “Amazon of South Korea.” In many ways, it is out Amazoning Amazon by offering overnight deliveries. If you order something like fresh lobster or a birthday cake before midnight, it will likely show up at your door in the morning or sooner. Think of Coupang like Amazon and Uber Eats having a baby.

When evaluating an e-commerce company, I first want to see if they have a moat. Does the company have a robust end-to-end network, well-developed fulfillment infrastructure, and the technology to integrate it all together?

The high costs of logistics investments are massive in building a moat. As we have seen with Amazon, Alibaba, and Mercadolibre, once you have a moat, you have a safety buffer or a de-risked business.

A 5-10 year head start over competitors as building an end-to-end logistics network from scratch is expensive.

A strong logistic network can lead to lower costs, a strong brand name, and a network effect.

Ability to leverage customers from the core retail business to sell them other products and services.

For the reasons above, Coupang has a moat and is Amazon-proofing its business from the company it copied.

Look at Amazon. To compete with Amazon and pull Prime Subscribers away, you must offer a service or experience significantly better than what is already available. You can only do this with a fulfillment infrastructure and a controlled in-house fleet. Amazon also has a home-field advantage as they know the region of North America better than a company based overseas. Laying down the groundwork to build a logistics network is too capital-intensive for even a large company to commit, making Amazon’s moat likely safe.

Mercardolibre has a moat in Latin America. Amazon has the resources and capabilities to take market share away from Mercadolibre, but that would not likely happen. The largest e-commerce markets in Latin America are Mexico and Brazil. Mexico and Brazil are not among the world’s top ten largest e-commerce markets. Amazon is amazing, but even they have to curb spending. Pouring money competing against a worthy competitor in Mercadolibre would move resources away towards more profitable regions like Germany, UK, Japan, and India.

Look at a fulfillment network similar to a foundation towards a home. Coupang has invested $4.69 billion over the past 12 years in establishing an in-house logistics network. With the home base covered, it gives Coupang the map to expand into Japan, Taiwan, and possibly other markets in Southeast Asia.

Coupang has a similar market cap to Sea Limited, another e-commerce company in Southeast Asia. I prefer Coupang as an investment mainly due to its more substantial foundational base. Sea Limited has already retreated from France and the majority of Latin America. For them, expansion was too much, too quickly. They will likely have to re-invest to fortify their core operations to fend off competition from Coupang and Lazada (funded by Alibaba). This will be more costly now than they had this been done years ago instead of expanding in outside markets. Coupang can take on more risk, while Sea Limited will need to be more cautious.

I don’t see a strong moat for Sea Limited. I am not saying Sea Limited is a lousy investment. However, they are something other than a true e-commerce play, more of a gaming play with Garena, their gaming platform.

Coupang is a good investment due to its strong core logistic apparatus, which gives them the blueprint to capture markets overseas instead of retreating like Sea Limited. They will not overtake Amazon in market cap or even come close. However, analysts are also vastly underestimating the South Korean market.

South Korea is the crown jewel of eCommerce. By 2025 South Korea will likely be the third-largest eCommerce market in the world, behind only China and The United States. That is impressive for a country the size of Indiana. It is a small country that packs a massive punch. Having a dominant market share of South Korea, which has a high gross domestic product per capita, is more significant than having a dominant market share of 3-7 smaller countries in Southeast Asia.

The average Korean worker worked 1,915 hours last year, the fifth-longest among 38 OECD (The Organisation for Economic Co-operation and Development) member countries. Koreans have very little leisure time and will pay a premium for convenience. There is still a lot of juice to squeeze from South Korea. Coupang already launched Coupang financial and Coupang Travel recently. It will be exciting to see if their business can expand into something like Travelocity or a bank. The stock is undervalued just for the growth in South Korea alone.

Suppose Coupang continues to dominate South Korea and finds new regional markets with high urbanization, population density, and a well-developed digital infrastructure. In that case, the stock will be a big-time winner.

I am also making a bet on Bom Kim, the CEO. For an immigrant CEO, Kim is very Jeff Bezo-esk. I am an investor who puts a lot of weight on the company’s leadership. Strong leaders with savvy and grit can flip the script and make the improbable probable. Leadership is not something you can typically spot on a balance sheet or 10-K, but for a growing startup, it matters.

Kim has the rare trait of someone with a long-term vision but is not afraid to pivot in response to unpredictable market conditions. With Bezos and Jack Ma no longer running their empires, Kim has a chance to cement himself as the next great founder-led tech CEO.

Coupang investor checklist:

The overall growth of eCommerce revenue continues to grow.

Coupang is in the best market for eCommerce sales outside of China and the United States.

Founder-led CEO with the characteristics of a visionary has a ton of skin in the game.

It diversifies its business model by entering new industries that complement its core operations.

Expanding overseas will be costly but could be what boosts this stock to an astronomical valuation.

Well-known investors like Bill Gates, Stanley Druckenmiller, and Bill Ackman have been backers of Coupang. These investors wouldn’t have taken such a significant position if they didn’t do a lot of due diligence.

Neither political party is better for the stock market. Neither party cares about your portfolio returns.

Tesla and Elon Musk are imploding. It feels like the company is headed toward an existential crisis or bankruptcy.

Investors must understand that investing isn’t a game of certainties or possibilities. It’s a game of probabilities. Many people do not invest because of the potential of stocks going to zero, even though the likelihood of that happening is highly unlikely.

Business goes through cycles. Although most stocks are down in 2022, energy, healthcare, and defense are areas that have done quite well.

Look at the stock of companies like United Health, Bristol Meyers, Gilead, Chevron, and many others in these industries. All are doing quite well. These are the stocks “experts” are saying you are supposed to be buying now, not selling. If you went back 3-4 years ago, these names were loathed, and now they are beloved. This is how cycles work. They turn. If you assume tech stocks will always be uninvestable, you may need to look at investing through a probabilities lens. Are companies like Meta, Tesla, and Netflix going bankrupt? Again, look at it through possibilities rather than probabilities.

One of the greatest investors people have never heard of was Shelby Davis. Davis was a long-term investor who started investing at age 38. From 1947 until he died in 1994, he turned $50,000 into $900 million.

Shelby preaches many of the same principles that Warren Buffett does in long-term investing:

The biggest history lesson you can learn is that the market cycles from bust to boom and back again. Investor behavior flows with it. Each time is slightly different but similarities abound and the cycle always rolls on,” he said.

“Between these two extremes, and what investors forget, is a great long-term track record at compounding money that no other asset class offers. The few times in history when there is an exception, investors rarely seized the opportunity because they projected their short-term pessimism far into the future,” he said.

Shelby Davis and Warren Buffett are legendary investors, but their gains are attainable even for everyday investors. When someone tells you it is nearly impossible to beat the market by picking stocks, it is an arbitrary statement that can make investors take inappropriate actions. Saying investing in single stocks is an impossible game to win is like saying sticking to a diet is impossible because most people fail at it.

These are some of my thoughts, and I could be completely wrong. Some of the views I am expressing cannot be proven quantitatively, but if I had to bet money, I am more right than wrong. I have always preached investing is more behavioral and philosophical than numerical.

Take a room of 10,000 random investors. 2/3 of those investors, or at least 6,666, will fail to beat the market not because they are uninformed or bad stock pickers but from self-inflicted wounds.

Investing money you can’t afford to lose. You can categorize these investors into two groups. People who shouldn’t be investing either live paycheck to paycheck or have no emergency fund. The other group is people that are invested but will likely need to dip into their portfolio in the near to mid future – to buy a house or fund retirement, for example. These people are not in a dire financial situation but will likely have to sell out of positions for non-investing reasons because they do not have enough discretionary income.

Lack of emotional control or patience. Suppose you have a strong conviction to buy a stock but a few months later sell out because the stock has fallen or everyone in the media is saying to sell. In that case, you most likely shouldn’t be investing. Humans aren’t hard-wired to be good investors. Humans hate losses twice as much as they like gains. A 50% loss feels as bad as a 125% gain feels good. This is one of the reasons why many investors never see exponential gains. They don’t have the stomach to wait for it. For many people, once they see 30-40% losses, they just sell and leave the market altogether.

The 6,666 investors will have one or two of these problems, like having one hand tied behind your back. This provides a significant advantage to investors that can follow basic long-term investing principles. Not an arbitrary rules-based methodology but an ability to think independently, be patient, and learn.

If you can invest money you can afford to lose and have balls of steel, you will likely be in the 70th percentile of investors. Notice I didn’t mention anything about a person’s ability to analyze/value stocks because this is a subjective practice that can be learned over time.

You will get little debate from anyone about not using your rent money on stocks. You will get a lively discussion on whether stock x is overvalued or undervalued. As you gain experience, if you are adequate at analyzing equities and can think independently, you can likely be in the 80th percentile or higher of top investors.

If you are in the 70th percentile of investors, you have beaten the market rather easily. How likely is this? Not that improbable.

If you are having trouble following, I will provide an example:

A 1200 SAT score can be considered good or bad, depending on one’s expectations. A 1200 SAT score puts you at the 74th percentile, which from one perspective, sounds great – you scored higher than 74% of your peers! On the other hand, a 1200 SAT score will not get you into Harvard or Yale.

So, when people say you aren’t likely to beat the market, it depends on the individual investor. The entry of barrier to investing is low. Are you an investing hobbyist, or do you view your portfolio like a business? The average Robinhood user is 31 years old with an account balance of $240. That is not enough skin in the game.

A large number of investing hobbyists skews the number of people that fail to beat the market at a higher percentage than it should. More than 2/3 of investors fail to beat the market, which is a conservative guestimate given how many Americans live paycheck to paycheck or do not have the proper investment mindset.

The majority of people that fail to beat the market are breaking simple investing rules. Think again about the high percentage of people who break their diet. Does that automatically mean you shouldn’t diet because most people fail or abandon their diet? Again, you have to individualize the experience.

Investors shouldn’t give up investing and automatically go into index funds. Tesla is a perfect example. A tremendous long-term stock going through short-term negative sentiment.

Returning to investors being able to control their emotions, this includes not being blinded by arrogance or ideology.

“Worldly wisdom teaches us that it is better for reputation to fail conventionally than to succeed unconventionally.” John Maynard Keynes.

Framing forward-looking expectations through an ideological prism is a terrible idea for investing. Getting investing advice from political commentators about Tesla stock is foolhardy. Partisan politics, by nature, is tribalistic, negative, and biased. Tesla sells electric vehicles for over $50,000. Most consumers on the fence about buying a Tesla base their decision-making on non-political reasons.

Potential Tesla buyers don’t care what Elon Musk thinks about Dr. Anthony Fauci or his tweets about Democrats. That is not how consumer behavior works. That is not how consumers think. Those that do most likely make up a fringe minority or weren’t that interested in buying a Tesla in the first place. Imagine buying a house: how much does a potential home buyer weigh the seller’s political affiliation or social media activity before making an offer.

The great Telsa story has been hijacked by politics. Political commentators and politicians do not care or understand the company’s financials. The declining stock price drives whatever narrative is spun by the media and curmudgeons on Twitter.

Investing and politics should not mix. You may disagree, but a CEO’s political affiliation is meaningless. Tesla is a fantastic company producing phenomenal growth results. I have seen this play out before:

“Tesla is doomed.”

“Elon Musk is unstable.”

“Tesla is a car company, not a technology company.”

“Tesla has no competitive advantage.”

I think I’ve seen this film before

And I did like the ending.

Where Tesla bears don’t admit they were wrong, they just say I got lucky.

The stock may enter a bust cycle, but this creates an opportunity. As Davis said, “out of crisis comes opportunity… A down market lets you buy more shares in great companies at favorable prices. If you know what you’re doing, you’ll make most of your money from these periods. You just won’t realize it until much later.” Unfortunately, many investors will fall into the same trap of selling stocks during a bust cycle and buying during a boom cycle.

The Tesla fundamental story is solid. The growth numbers are impressive. The future is incredibly bright. The Tesla Bears have already been defeated. Refuting decade-old talking points is a waste of time.

Politics is mainly theatre. It is entertaining to watch, but it typically has no material impact on a company’s earnings, profits, or shareholder value. Trying to turn political commentary into investment tips is dangerous in investing. Politics has a definite space for society, but how do political programs on CNN, MSNBC, and Fox put money in your pocket? In investing, it doesn’t. I view these shows on the same level as watching pro wrestling, or comedy shows, purely for entertainment.

Having insurance is one of the best ways to preserve your wealth. Another way to say this is that insurance protects your downside risk and makes it less likely for you to go into financial ruin.

Did you know that medical bills cause over 62% of all bankruptcies? Health insurance isn’t a cure-all solution since it doesn’t cover all medical expenses. Still, it would be reckless today to voluntarily opt out of health insurance.

Being young and healthy is not a smart reason to opt-out of insurance. The risk of paying the total cost of a health emergency is the equivalent of being trapped in a building with a bomb in it. The explosion will hurt you.

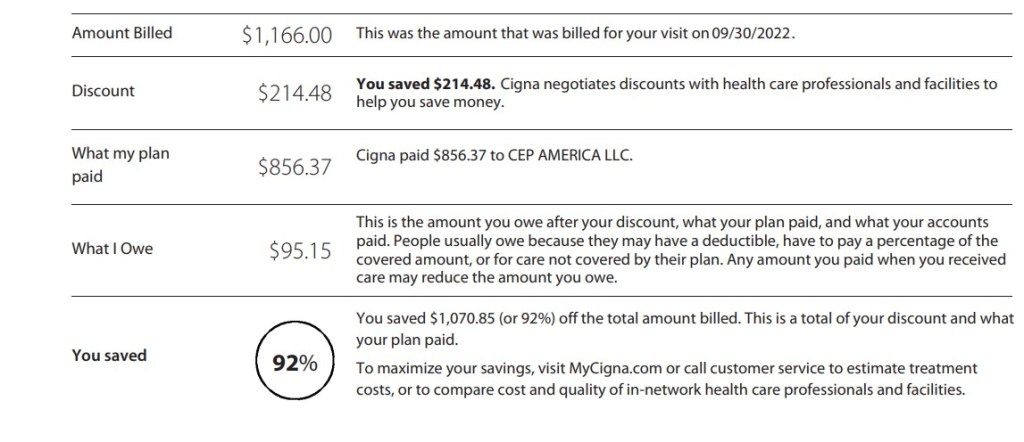

A few months ago, I had chest pains, which could have been a precursor for a heart attack. Luckily, I went to the emergency room, and all my tests returned back as normal. I never found out why I suffered chest pains, but I was still billed $5,716 for a few tests. Insane right? No treatment or diagnosis, just a few bills to find out I didn’t have a heart attack.

Put yourself in my shoes. I am relatively healthy, with no serious medical history or preexisting conditions. Do you avoid a trip to the ER and hope the pain goes away but risk suffering from a heart attack in your home?

One of four medical bills I received for getting tests done. Luckily my insurance covered the majority of this bill.

I was lucky and considered myself fortunate to have insurance. Is it worth saving $100-200 monthly in premiums but risking paying medical expenses at full cost? No investment or opportunity is worth the uninsured risk. Multiple medical bills can create an avalanche effect, wipe out your net worth, or bury you in debt. Remember, unpaid medical debt doesn’t go away or expire.

Get Health Insurance! Being uninsured is not worth the risk!

The amount you would save in a decade by not paying premiums ($200 monthly) with no health insurance: $24,000

The average cost of a hospital stay for one day is $2,873

Main takeaway: Many Americans are doing okay financially but are entirely unprepared to absorb a major financial shock. A cataclysmic health crisis, even a mini one, can crumble your net worth. Staying at a hospital for over a month without insurance will cost you easily over six figures.

I agree that health insurance in the United States is broken and unfair however people have to best navigate through this rigged system with intelligent financial decisions. Just complaining about the system and hoping the government will fix it isn’t a viable solution. Health insurance is one (but not the only) way of not becoming another American healthcare system victim.

If getting good health insurance requires working a part-time or full-time job you hate, so be it. Educate yourself and take prudent steps before soliciting donations on GoFundMe becomes your only option. Ignoring the issue isn’t going to resolve the issue. Crying foul on how rigged the system isn’t a viable solution either; take steps to protect yourself.

Another valuable insurance is renters or home insurance. Many landlords and banks require insurance, but it isn’t required by law like car insurance. Ironically about the same percentage of people who file for bankruptcy from medical bills is about the same percentage of renters that do not have renters insurance.

Many think paying $10-15 a month in renters insurance is a waste of money, even at that low cost. I used to think this way until I was recently robbed.

The robbers took nearly all of my belongings. Luckily I was not injured or required any medical attention. My insurance through Lemonade reimbursed me for my phone, laptop, and glasses. Getting those funds wired from Lemonade provided a great sigh of relief. They made me realize how paying for renters insurance was worth every penny.

Please consider getting renters, pets, car, home, or life insurance through Lemonade here. My experience with the claims agent, Jose, was pleasant, and the process was smooth. Once I provided a copy of the police report, Lemonade immediately wired the funds to my bank account. I couldn’t have received better service from any other insurance company, and I am thankful for being a policyholder through Lemaonde.

Think of insurance as a safeguard for yourself. You do not typically profit from insurance, but it keeps you whole or restores what you lost. I write a lot about how investing can create financial freedom, but with wealth building, you need to start with a strong base or foundation. Insurance is necessary to protect that foundation and can prevent it from collapsing. Investing can create wealth, but insurance can protect it. Insurance will act as a safety net even if you have a small net worth. If you voluntarily opt out of insurance or are thinking about it. I strongly advise you to reconsider. In risk management, not having insurance is one of the riskier decisions you can make.

Taylor Swift performs in Houston in 2017. Photographer: Frazer Harrison/Getty Images North America

Taylor Swift fans, or “Swifties,” will spend ridiculous money on seeing her perform live. For many fanatics, the motto is “I’ll spend the money now and worry about paying it off later.”

Spending $3,000 or even more for a Taylor Swift ticket is ridiculous. Looking at it from a surface level, even if you are affluent, spending this money on a concert is a bit irrational.

I will not judge Swifties or fans of Beyoncé, Lady Gaga, etc., for spending this kind of money because experiences have a different price tag for everyone. For one person, the experience can be transformative; for another, it’s $1,000 an hour to watch someone sing live. These stars have built large, dedicated communities, and fans will spend; this is nothing new in fandom or consumer behavior.

The problem with Taylor Swift as an artist is that she isn’t generational. She is a product of Wall Street. A talented songwriter/musician who understood the business aspect of the music industry and cashed in. Taylor Swift’s father is Scott Kingsley Swift, a financial advisor at Merrill Lynch. Her mother was a mutual fund marketing executive. Her career is managed like a wealth portfolio, and it shows.

I am not questioning Taylor’s talents or abilities. The problem with Taylor is that she didn’t break down any barriers or transform the music industry. America loves artists saved by the music industry or musicians who went from rags to riches. Tayor was born into a well-off family that provided her the resources and connections to become the star she is.

My theory is that the most influential artists are highly flawed individuals. These “broken” musicians can manifest their struggles and life experience into their music. The music produced can be volatile, raw, and out-of-the-box, ultimately redefining music genres and reshaping the industry.

Many of the most influential musicians suffered from abusive parents, alcoholism, drug abuse, violence, trauma, or something tragic that happened to them. Mixing that in with Hollywood and paparazzi can create an explosive solution that garners a lot of eyeballs. None of the above fits Taylor. Her story is kind of uninteresting. Imagine a millionaire who already manages their money well, winning the lottery.

Taylor is a highly talented artist who manifests a whimsical/cookie-cutter view of capitalism. With her music, I don’t feel a real sense of struggle, passion, or purpose. The most passion she has shown was fighting for her music catalog rights, which was more about profits than the actual music.

There are better role models for musicians than Taylor Swift. As an entrepreneur, yes, but as an artist, no. Taylor’s music is highly curated and manufactured. More about ROI and profit margins than taking risks and breaking barriers. More about image control than raw vulnerability. Around the world, you can find thousands of talented undiscovered artists playing at smaller intimate venues and watch them perform live at a fraction of the price of an Era Tour Ticket.

Unfortunately, we see a lot of Taylor Swift clones emerging in the industry with younger artists like Olivia Rodrigo, who are drawing inspiration from the more commercialized version of Taylor. Do people remember when she was a country singer?

Gustavo Coutinho, who’s never seen Swift perform live, came up with a $2,000 budget after 10 months of savings. The 25-year-old consultant in Boston ended up spending about $1,500 to attend two concerts. “I would pay $3,000 if I had to.”

Truly, generational artists take risks, even dangerous ones, and the audience decides whether that risk is worth taking. Taylor’s career arc has been a consistent slope towards playing it safe and mediocrity. That is a slam on her as an artist, not an entrepreneur. Unlike a lot of musicians, she thinks like an executive. She’s more Sheryl Sandberg than Amy Winehouse.

In the future, I would expect her to launch her own record label and become a billionaire. In 10 years, her empire will be worth more than Ye, Rihanna, and even Jay-Z/Beyoncé. Taylor has the Millennials and Gen Z demographic locked down pat, who will continue to pay their hard-earned savings to watch her perform live.

I am not knocking Swifties. However, they should evaluate the actual reason for their worship of Taylor. Rooting for Taylor is the equivalent of rooting for TicketMaster, Alabama Crimson Tide, Facebook, or Amazon. She doesn’t look at her fans as fans but as lifetime customers who pay, in essence, an annual subscription for her merchandise and events. To Swifties, she may seem down-to-earth, but in reality, she is an opportunistic savvy business genius.

“If you are working on something that you really care about, you don’t have to be pushed. The vision pulls you.”

Steve Jobs

Many of the best companies are born during tough times. It feels like we are in a macroeconomic depression.

For Lemonade investors, you have to be comfortable being uncomfortable. Currently unprofitable and not forecast to become profitable over the next three years.

That is not new.

The stock will suffer because there isn’t a short-time pathway toward profitability. In a market like today, unprofitable companies get punished, especially with the ongoing inflationary pressure.

I’m highly confident that at some point in the future — it might be six months or three years — we’re going to look back at some point over the next few months, and we’ll say, ‘that was a phenomenal time to buy Lemonade.’

Every investment opportunity has risks. You have to assess if the risk is worth the reward. Sometimes the risks are either exaggerated or hidden. Some companies can overcome risk, while others can’t. An investment in Lemonade is worthwhile for the potential reward. I could see this being the start of something big.

The good news:

The story is simple. Lemonade will either realize the economies of scale or not. To achieve this, they must continue to grow. The good news is customer growth is scaling nicely.

Where Lemonade shines brightest: Gateway policies

Lemonade is among the leaders among all insurance companies in acquiring first-time buyers of renters insurance, especially if they are under 35 years old. The growth in pet insurance is also impressive.

The growth rate for these gateway policies is very positive, but renters and pet insurance are just appetizers for Lemonade’s growth. These businesses are niche, and customer churn is high.

Renters and pet insurance have to be looked at the same as the rice and asparagus of insurance policies. Nobody eats rice or asparagus by itself, but when eaten with steak, chicken, or mac and cheese, it creates a perfect synergy. Lemonade renters and pet insurance policyholders will bundle more policies together as they become available. If they need term insurance, it is available. Lemonade has a 300k waitlist for Lemonade car without advertising. Most of those on that waitlist are in the Lemonade ecosystem.

Customer growth has been consistent and steady. I expect that to continue as they enter more markets. When Lemonade grows with more 2-4-product policyholders, you will see the flywheel spin.

Evolution of a policyholder at lemonade:

$60 a year: Renters Insurance $600 a year: Renters, Car, Pet Insurance $6,000 a year: Home, Car, Pet, Term

The bad news:

I fully expect loss ratios to fluctuate in the short term. Lemonade is an insurance company that isn’t profitable. Not what you want to hear, but they are a newer company. I don’t hold it against them, just as I don’t hold it against SoFi or Block for being unprofitable banks. It is about the future forecast.

That being said, any catastrophic natural disaster like Hurricane Ian will have a more crippling effect on Lemonade’s balance sheet than a more stable insurance company. A rise in claims will hurt any insurance company’s bottom-line results, but for Lemonade, the cut will be felt deeper since they are still trying to diversify their business book.

Lemonade home and car are low frequency-high severity products. When paying out claims for home and car, the payouts can be crippling. It creates a double-edged sword. The juicy TAM and profits are in car and home insurance, but so are the expenses and payouts.

The question remaining:

How to determine if Lemonade will be a big-time winner: If their technology – LTV models, leveraging AI and machine learning can lead in the long run to better underwriting results.

A natural event like Hurricane Ian can push insurance companies to the brink of bankruptcy. How Lemonade navigates through this in the future will determine if they succeed.

From Q3: Total Customers: 1,775,824. Premium per customer: $343. As the customer count grows and more products become available, the premium per customer should steadily increase. As this happens, the LTV Models and AI provide better predictive data, leading to better underwriting. The result is providing more desirable customers with less expensive premium costs and riskier customers with more expensive premium costs.

That is it. Lemonade’s stock will likely go sideways in short to medium term. It may even go down significantly. It might take several quarters for Lemonade to hit its stride fully, but the groundwork now will be unlocked and prove significant in time.

Expenses may continue to grow, but if Lemonade can gain exponential customer growth, that will be the key to unlocking a network effect. If Lemonade gets a network effect, revenue growth will far exceed expenses.

I could never see myself selling Lemonade stock anytime soon because the potential reward is so big. The company could 10x, twice, and still have a small share of the overall insurance market.

Lantern Consciousness and First Principles Thinking

Many investors are looking at Lemonade as a big loser, which is fine. The stock is not for everyone. I would argue that narrowly focusing on just a few key metrics can create blind spots and tunnel vision in investing.

Consider the difference between spotlight and lantern consciousness. Spotlight consciousness illuminates a single focal point of attention. This is how most adults think. Lantern consciousness illuminates a broader point of attention. This is how most children think.

Spotlight consciousness is fantastic. Drugs like caffeine and certain medications enhance it better. The problem with spotlight consciousness is that it may not be helpful for long-term investors.

Projecting a company’s stock price in 5-10 years is silly, focusing on the balance sheet or discounted cash flow model. Lantern consciousness in investing can provide an advantage because it doesn’t lead toward a predictable tract. Financial measures and formulas don’t help see where a stock will go long-term, as too many variables can change. Figures can be interpreted differently based on preconceived notions and biases. If a few prominent analysts make a prediction, it shapes everyone else’s perception, leading to a herd mentality. Humans generally want a feeling of belonging, so popular opinions often become the “right” opinion.

What is needed is a more philosophical viewpoint or first principles thinking. This is why investing is hard. Humans desire to belong, and investing requires you to go against the popular decision. When utilizing lantern consciousness and first principles thinking, it allows you to peel the onion and gain a more introspective viewpoint:

In layman’s terms, first principles thinking is basically the practice of actively questioning every assumption you think you ‘know’ about a given problem or scenario — and then creating new knowledge and solutions from scratch. Almost like a newborn baby.

On the flip side, reasoning by analogy is building knowledge and solving problems based on prior assumptions, beliefs and widely held ‘best practices’ approved by majority of people.

People who reason by analogy tend to make bad decisions, even if they’re smart.

Elon Musks’ “3-Step” First Principles Thinking: How to Think and Solve Difficult Problems Like a Genius

Lemonade can be a big winner because they have a culture and model wholly divorced from how legacy insurers operate. Could they fail? Obviously, but what if they succeed? Something improbable is improbable until it isn’t. The insurance market is incredibly inefficient and outdated. A lot of it needs to make more sense to the consumer. Why do male drivers pay higher insurance than female drivers? Simple because of their gender? Why do older drivers pay less than younger drivers? Simply because of their age?

Calculating premiums based on how groups of people within a demographic behave is outdated and unfair. Lemonade addresses many of these inefficiencies because they utilize technology to create a more efficient business model, and if they succeed, the stock has no real ceiling. Again, they can go bankrupt, but from where they were in 2015 to now, the company has made meaningful progress and is still in the early innings of growth.