In 2016, I invested in Tapestry (TPR), betting on Coach as an undervalued brand poised for a turnaround. It was one of the first stocks I bought as a new investor. My thesis was straightforward: the stock could reclaim its March 2012 peak of $79.70. Nearly a decade later, my prediction proved correct, though the road was far from smooth.

Tapestry faced significant challenges, including the 2019 ousting of its CEO, the 2020 resignation of another due to ‘personal misconduct,’ and a 2024 court ruling blocking its merger with Capri Holdings. Yet, TPR has outperformed the likes of LVMH, Lululemon (LULU), Capri Holdings (CPRI), and Nike (NKE) over the past five years—the very stocks I eyed when TPR struggled. Those same peers now sit well below their prior peaks.

I acknowledge luck played a role. Had the Capri merger proceeded, TPR would likely be trading in the $50–$70 range today, far below its current levels. Now, with TPR soaring past its 2012 high, I’ve shifted my strategy and trimmed my position to lock in long-term gains. If the stock continues to climb, I’ll likely reduce my holdings further.

My original thesis—that Coach was trading at a bargain—no longer holds. In a tough luxury market, Coach has unexpectedly gained pricing power for a mid-tier brand, fueled by a reshaped brand narrative and the TikTok-driven success of its Tabby Bag. However, Kate Spade, accounting for about 15% of revenue, remains a weak link due to inconsistent branding and declining sales, tempering my optimism.

Management deserves credit for Coach’s turnaround, but I remain cautious. Tapestry’s cyclical nature ties its success directly to consumer spending and economic conditions. A weakening economy would likely pressure sales.

Tapestry’s acquisition strategy is my primary concern. Selling the unprofitable Stuart Weitzman brand was a smart move, but the pursuit of the Capri merger suggests management may doubt Coach’s standalone growth potential. Given the lackluster outcomes of the Stuart Weitzman and Kate Spade acquisitions, future M&A activity could increase debt and strain cash flow.

My suggestion? If Tapestry is set on acquisitions, it should issue new shares to fund a targeted purchase, such as a niche luxury brand with strong growth potential. This approach would preserve cash and avoid debt, though it risks diluting existing shareholders. It could create more long-term value than increasing the dividend or buying back stock to where it’s trading currently—an action that offers limited upside if the stock corrects.

While I’ve enjoyed reinvesting dividends during the stock’s recent climb, weaker economic indicators, like declining retail sales, suggest uncertainty ahead. Most companies in the consumer cyclical sector face headwinds from slowing spending, and TPR is no exception.

That said, TPR isn’t wildly overvalued. With an upcoming earnings report and Investor Day looming in September, short-term upside potential remains. I’m cautiously optimistic and will monitor these events. My goal is to sell more shares at a higher price before the end of the year.

Once the undisputed athletic apparel champion, Nike has faced increasing challenges recently. With Mark Parker’s departure and John Donahoe’s subsequent leadership, the company is struggling to keep pace with rapidly changing consumer preferences, particularly among Gen Z and Millennial demographics. The stock has seen a significant decline, underscoring the urgency of the situation.

A New Playbook

Starbucks’ revival under Brian Niccol’s CEO appointment is a powerful example of the transformative potential of strategic leadership change. Nike, too, could benefit from a bold and quick decision, emphasizing the need for risk-taking in order to reap potential rewards.

Sheryl Sandberg: The Perfect Choice

With her experience as Facebook’s COO, Sheryl Sandberg possesses a unique blend of skills and insights that are directly relevant to Nike’s current challenges. Her deep understanding of social media and her passion for women’s empowerment aligns perfectly with the company’s visions and goals, making her the perfect choice to lead Nike into a new era.

Leveraging Women’s Sports and Social Media

The growing popularity of women’s sports, exemplified by the rise of athletes like Caitlin Clark, presents a significant opportunity. Nike can tap into a powerful cultural force by investing in women’s sports and leveraging social media to connect with younger audiences. As a female executive who has broken barriers in the tech industry, Sandberg is well-positioned to champion women’s sports and empower female athletes.

Cultural Understanding

According to a recent survey, 40% of Gen Z and Millennials find women’s sports more exciting to watch than men’s, compared to about 25% of Gen X and Baby Boomers. Moreover, social media has become integral to how consumers engage with sports. Six in 10 Zoomers are very interested in content creators on Twitch or YouTube chatting about sports on live streams, and 70% discovered or deepened interest in sports through fan communities on social. This indicates a significant opportunity for brands to leverage social media to connect with younger audiences.

A Game-Changing Move

Sheryl Sandberg’s leadership could be the game-changer Nike needs to regain its cultural relevance and standing. Her proven ability to drive revenue growth, build strong teams, and foster a positive company culture would be invaluable in navigating the challenges of a rapidly evolving market, instilling hope and optimism in the company’s future.

Sandberg’s expertise and track record are based on optimizing and fine-tuning advertising revenue. She can create a more effective ad strategy, creating engaging and shareable content that builds communities and drives engagement.

The Time is Now

By bringing Sheryl Sandberg on board, Nike would signal its commitment to innovation and demonstrate its understanding of the changing landscape of sports and consumer behavior.

Caitlin Clark’s meteoric rise is changing the narrative of how we talk about women’s sports and how to market women athletes effectively. It’s a shift that’s happening now. Nike needs to adapt quickly, and bringing in a proven winning rockstar CEO can dramatically turn things around.

I endorse giving Sandberg a blank check to turn around Nike. John Donahoe is the wrong CEO to revive the brand. Sandberg’s background in technology is not directly relevant to the athletic apparel industry, but Nike has never been just an athletic apparel company—it’s a global cultural brand that celebrates great athletes. This is the right time, and Sandberg is an even better fit. I urge the Nike board of Directors to take action because quite, honestly, it makes too much sense.

Despite Nike’s current slump and the deserved hit its stock has taken, the growth potential is significant. Many of the issues are fixable, and with Nike’s robust financial and brand muscle, it can weather these storms, even a potential recession, as it did in 2008. Nike’s infrastructure and ecosystem have been stress-tested for decades, a testament to its resilience.

You won’t find it here if you’re seeking a deep security analysis of Nike Stock with a sophisticated review of Nike’s business. But that’s not a cause for concern. Nike is a simple business, and my investment thesis is relatively straightforward.

I am bullish on Nike because Caitlin Clark has the potential to propel it into a new hyper-growth phase, similar to the impact we saw with Michael Jordan in the 1980s and 1990s. This growth potential seems evident (the right time and place) for a magical story to unfold.

When Wall Street talks about Nike, it seems rather blah. Where is the creativity or outside-the-box thinking? Almost everyone analyzing this company is talking about the wrong thing. Nike can be summed up simply through a Steve Jobs quote:

“The best example of all, and one of the greatest jobs of marketing the universe has ever seen is Nike,” Jobs explained. “Remember, Nike sells a commodity. They sell shoes. And yet when you think of Nike, you feel something different than a shoe company. In their ads, they don’t ever talk about their products. They don’t ever tell you about their air soles and why they’re better than Reebok’s air soles. What does Nike do? They honor great athletes and they honor great athletics. That’s who they are, that’s what they are about.”

It’s not about the shoes; it’s about the people wearing the shoes!

It’s that simple.

A shoe is just a shoe. Proprietary shoe technology doesn’t move merchandise. Nike is an aspirational lifestyle brand. No other company in the world does a better job selling and promoting great athletes. They have an invisible superpower in their brand value, an intangible asset that drives a high level of engagement in selling apparel, shoes, and merchandise.

Nike isn’t the company it is today without Michael Jordan, who signed a five-year, $2.5 million deal in October 1984.

The contract was an absurd overpay for a basketball player at the time. Yet, now it looks like a slam dunk for Nike because Jordan transcended basketball and became a global cultural phenomenon.

The NBA and Nike didn’t elevate Jordan; it’s the opposite. The Jordan brand elevated basketball and sneakers to new heights. His sponsorship with Nike turned into a billion+ industry.

Nearly 30 years after Jordan signed with Nike, Clark signed an eight-year deal worth $28 million. This deal is bafflingly low for what could be a future brand worth $1-5 Billion.

Nike stock appreciated over 1,000% from when they signed Jordan to when he retired for the first time in 1993. It gained another 100% from when he returned in 1995 to when he retired for good in 2003.

In the story unfolding with Caitlin Clark today, we are witnessing the early stages of another cultural phenomenon that undeniably impacts culture.

How Clark can elevate Nike:

The Clark Effect:

A name that is trending up: Clark transcends sports. Very few athletes trend like this with long-term staying power. We already see this in the WNBA, a sport with an extremely niche following pre-Clark. The fanbase was small, with fans not spending “big” money on the product. That is changing.

Clark is now part of daily sports talk shows and debates. The more people talk about it, the longer it remains relevant and stays in the mainstream discussion.

Record WNBA attendance and viewership:

When the Indiana Fever played the Los Angeles Sparks, 19,103 fans attended Crypto.com Arena. That was more than the largest home game crowd for the Los Angeles Lakers, and LeBron James drew 18,997.

The cost of Indiana Fever tickets has doubled and, in some marquee matchups, nearly tripled compared to last year!

WNBA games are averaging 1.32 million viewers, almost tripling last season’s average of 462,000.

The WNBA has expanded, adding two new teams: the Golden State Valkyries in 2025 and a Toronto team in 2026. More stars will join the WNBA in the next four years – Paige Bueckers, Juju Watkins, Hannah Hidalgo, etc.- which will increase viewership and the league’s star power.

Based on ESPN personalization data, the WNBA has seen the largest YoY growth (+47%) among sports with 1M+ favorites

Caitlin Clark led all players with +373% MoM growth to become the 4th most-favorited active athlete, only behind LeBron James, Tiger Woods and Steph Curry

She is only trailing LeBron James, Stephen Curry, and Tiger Woods. Clark could quickly ascend to #1 in the next 3-5 years as the most famous athlete today, just entering her physical peak. The top three athletes in this list are nearing the tail end of their respective careers.

She’s a superstar:

We have seen hyped-up college athletes like JJ Redick and Jimmer Fredette before. We have witnessed Linsanity in the NBA and Tebow Mania in the NFL. None of these players were superstar athletes on the pro level, and their fandom eventually diminished.

No checkered past with a pristine record:

Clark seems similar to Jordan, a no-nonsense athlete intensely focused on basketball and obsessed with winning. No demons or scandals that diminished or brought down other athletes – Kobe Bryant, Johnny Manziel, and Michael Vick come to mind.

I don’t see Clark posting dances on TikTok or starting her podcast. She’s not an activist who is getting involved in politics. Eat, Sleep, Breathe, and play basketball. There are no distractions.

A new brand within a brand: Bigger than Air Jordan?

Clark already has a rabid, dedicated, and obsessive fanbase. Comparing Clark with LeBron James or Stephen Curry is the wrong comparison. Clark’s brand is more similar to that of Taylor Swift and Barack Obama.

Swift can make her fans spend over $1,000 on a non-premium seat ticket for a show and make them feel they are getting a reasonable deal.

Obama brought in millions of first-time voters to vote for him because (insert whatever reason you believe is correct) he propelled himself to a cultural phenomenon status.

A market largely untapped by Nike:

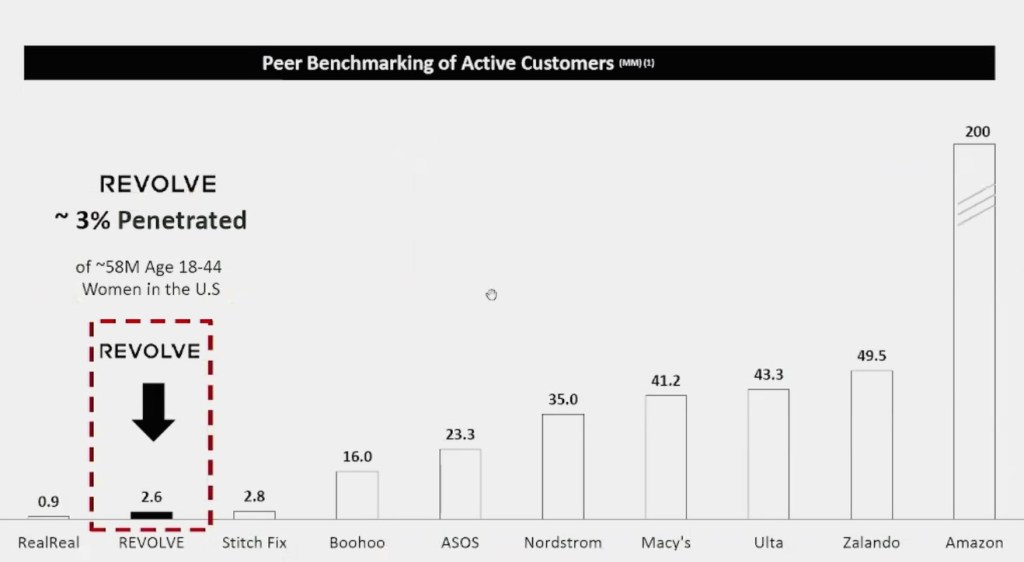

Nike’s women’s segmented business makes up just 22% of its sales.

Think of all the girls and women who want to buy Clark’s shoes. The market is largely untapped. Nike is seeing early success with Sabrina Ionescu and the Sabrina 1, a top ten WNBA player.

Clark’s brand could evolve beyond sneakers and boost Nike’s lifestyle segment into an entire product line of different types of shoes, socks, tracksuits, etc.

Identity with mass appeal:

Victor Wembanyama is a French basketball player and could be the best men’s basketball player in the next five years. He is also a Nike athlete, but I don’t see him coming close to bringing in what Clark does. “Wem-bany-am-a,” the name isn’t catchy or memorable. “Clark’s” is already a well-known popular shoe retailer in the UK. Besides the name, Clark is from the heartland and plays in the heartland.

I am not knocking Wembanyama or Ionescu as athletes, but like performers, style points matter in our culture. The top recording artists aren’t the top vocalists. Popularity and fandom are more a feeling than a rational thought. Competitive sports fall into a performance art category. What you won’t hear on CNBC or Bloomberg is the intrinsic relationship between Clark and her fans in the arena and online.

Get in while you can:

Wall Street will react once the shoe is released and the numbers are in an earnings report. I am getting in now. As we saw with Jordan, this feverish support can last for years, even decades. I see a noticeable halo effect for Nike, and this is like investing in Taylor Swift if she were a stock in 2010.

What I also love about this investment is that it isn’t binary. It could be a solid long-term investment rather than a trade.

Nike’s dividend (1.96%) is low, but given its financial health, it is well-covered by earnings and has increased over the past ten years. This trend should easily continue in the next ten years.

Nike trades at about 21x forward earnings. There is no expected earnings growth this year, so the stock is cheap (for a growth company) and reasonably priced, with low expectations.

Nike has a solid business that doesn’t need saving, but Clark could elevate the brand to a level that even Nike executives do not anticipate. A signature shoe deal was originally off the table during the initial negotiation, showing skepticism about the confidence that a shoe line by a female basketball player could drive sales. At this point, the skepticism doesn’t matter. It would be hard for Nike to mess things up and not capitalize on Clark’s meteoric rise in fame.

The biggest question is whether men will buy Clark shoes. I empathically believe yes. Hype and cultural shifts are not gender or even age-exclusive.

Take, for example, Donald Trump, who has said deplorable things against women. His actions against women have been equally disgraceful, yet he has millions of supporters who are women.

Taylor Swift’s fanbase is distributed uniformly across various ages. Almost half the people who attend her concerts are over 45, and her fanbase is almost evenly split 50-50 between males and females.

Humans are generally programmed to follow a herd. The more popular Clark becomes and achieves on the court, the more valuable her brand name becomes, making her a powerful force in selling merchandise to anyone worldwide, not just sneakerheads or young girls.

Even if Clark flops, this isn’t an all-or-nothing type of risk. The business is highly robust. Nike has missed trends and made mistakes in the past, but it always recovers because it excels at sales and marketing better than almost everyone else. If there is lightning in a bottle with Clark, Nike will know how to maximize sales. That’s what they do.

Revolve’s venture into brick-and-mortar retail with its first Aspen, Colorado store was not just a success, but a triumph. The initial pop-up store in December was a mere glimpse of the potential, and the decision to sign a multi-year lease was a resounding testament to Revolve’s ability to exceed its own expectations.

Why does this matter? Revolve, a digital-first business that has been diligently building its brand and e-commerce model, has made a strategic shift. Despite previous comments from earnings calls suggesting no serious plans for retail, Revolve has now embraced the potential of the physical retail space.

But the results were too good to ignore. It wasn’t so much that they sought retail, but demand called, and Revolve answered the call.

Aspen is just the beginning. With a robust digital marketing apparatus already in place, and the success of its first brick-and-mortar store, Revolve is poised for further expansion. This is a pivotal moment for Revolve, as it can now potentially translate its digital brand into a network of physical stores, paving the way for future growth.

This has the potential to increase an already impressive high average order value from the benefits of in-person shopping: impulse buyers from being able to feel and touch the merchandise. The Aspen store has also been a source of bringing in new customers, which is Revolve’s advantage and opportunity.

Advantage: Revolve’s customer base is mostly Millennial and Gen Z females. Roughly 60-70% of Macy’s and Nordstrom’s customers are Gen X and Boomers. I am not optimistic about legacy department stores. They have a problematic long-term business outlook. Macy’s is investing heavily in Bloomingdale’s and Bluemercury, but their brand name has declined significantly in the past decade. Nordstrom is doing a better job attracting young customers due to its off-price retail chain, Nordstrom Rack, but focusing on deals and discounts is a race to the bottom, and they will likely lose to Amazon, Walmart, and Target. I never understood Nordstrom’s business model because the off-price division does not complement the flagship stores. A “luxury” brand shouldn’t target consumers on a budget and vice versa.

Opportunity: Macy and Nordstrom need help mightily attracting Gen Z customers. It’s dire. Both companies will likely not show any year-over-year sales growth. Macy and Norstrom will eventually go private and leave the public market soon. It’s not a matter of if but when. These businesses may be able to restructure by going private, but it will likely take a very long time. Going private would also make raising capital difficult and cause a potential departure from key employees. Once the move happens, the capital and employees will likely shift towards a company like Revolve.

Is the Aspen store a signal for immediate retail expansion? I hope not. The focus should remain on building the digital platform and live events—Coachella, The Super Bowl, Cannes, etc. Physical retail should only complement the existing business unless the data overwhelmingly suggests otherwise. Much work is needed to build the brand through product/category expansion and international growth, which is more cost-effective through social media and pop-up events.

It would be premature for Revolve to make an aggressive retail push like Aritizia (3-5 new stores annually by FY27). They also don’t need it. Revolve has a much bigger online presence than other digitally native brands like Figs, Warby Parker, or Allbirds.

As a shareholder, I advise Revolve management to focus on curation rather than expansion. Identify 3-5 unique locations to create a highly personal and immersive experience. The stores should be bright and feature natural wood fixtures, making them engaging places to shop. Aspen works because it is an affluent city that blends luxury, charm, and scenic beauty. However, a store like Aspen is not scalable to a nationwide rollout. The ambiance is more subtle than in bigger cities like Las Vegas or Miami. It offers lesser-known brands in the high-end category to stand out more to a wealthy clientele.

I have identified some markets for Revolve to explore that can create a potential Aspen effect:

Park City, Utah Nantucket, Massachusetts Jackson Hole, Wyoming Charleston, South Carolina Carmel-by-the-Sea, California Key West, Florida Santa Fe, New Mexico

Entering smaller but highly profitable markets is a strategic move that makes perfect sense. Revolve, armed with ample marketing data, is poised to make prudent decisions and identify a few Aspen-like markets. The goal is to create a small footprint of high-ROI stores that offer a curated collection of luxury fashion brands—a blend of art, immersion, and boutique feel. The key is a luxurious bespoke experience, catering to the target audience’s preference for experiences over value or deal-hunting.

There is still plenty of room to grow. Despite a challenging macroeconomic picture for luxury retail, I haven’t sold any shares. I am confident in the business’s fundamentals and see a long-term pathway for growth and overperformance.

Revolve remains one of the largest holdings in my portfolio. The stock has suffered due to softening demand in the U.S. Consumers are spending less on discretionary items due to high-interest rates. Revolve and most luxury brands are directly affected when aspirational shoppers spend less money. When you add economic uncertainty and a tense geopolitical landscape, it creates a rather unsettling picture. The company has lost favor with Wall Street, and analysts have written off the company, but not so fast. Signs of a retail rebound are emerging, and Revolve can bounce back strong.

Despite retail headwinds, the underlying fundamentals of the business remain intact. The leadership, vision, and strategy have stayed the same. Revolve, as a business, has many traits that I love in an investment:

No long-term debt.

Low CapEx spend.

Proven history of generating an operating profit before the pandemic and even during a tough 2023.

No significant share dilution.

Buy back shares at an appropriate price when the stock price is low.

Revolve is still the same: a profitable e-commerce fashion platform that leverages social media and influencer marketing.

The broader slowdown in the luxury market has occurred as we have seen some cracks. Saks Fifth Avenue has been months behind in paying some of its vendors. Farfetch, which is, in my best comparison, the Shopify of luxury fashion, is either on the verge of insolvency or going private. Although these are disturbing headlines for the industry, they are incremental to the vast online luxury space ecosystem and insulated from these poorly managed companies. Saks issues predate the pandemic, while Farfetch has an extreme governance issue. Early signs point to a rebound or a normalization of luxury spending.

Farfetch was a company I considered investing in due to its innovation. Fast Company named it the 19th most innovative company in 2022. My concern with Farfetch was its large debt load and a lack of clear direction. The company tried to emulate Amazon’s growth strategy, but that approach has been costly. Instead of being innovative, they have become bloated with a complicated business structure.

The advantage of being an asset-light business is that you can remain innovative, be agile, and have excellent margins. Farfetch was asset-light in its early days but went on an expensive acquisition spree over the past eight years, entering into physical retail and drifting away from being solely a technology fashion platform. A lot of these investments have gone south. As their growth slowed due to a changing macro-environment, the story became muddled as they piled on more debt, further delaying the likelihood of becoming profitable anytime soon.

Revolve has avoided Farfetch’s mistakes by not expanding into physical retail or entering ambitious endeavors outside their core business, like the resale market. Farfetch will likely survive operating, but not as a public company. The stock is down over 97% from its all-time high in 2021. Many of its key executives have already departed, and they will likely have to offload many of its investments at a steep discount.

Revolve remains intensely focused on brand engagement and building a dedicated army of influencers who promote the company. The strategy is working, and Revolve is seeing meaningful growth in its virality on TikTok. The business model is becoming like a perpetual royalty business on influencer marketing. The Brand Ambassador Program becomes a money-printing advertising business as its digital channel presence on Instagram and TikTok grows; it generates more cash on every new post. Having such little debt and low CapEx spending means Revolve can continue investing in its brand. I will eagerly see how much Revolve and Forward can develop in the next 5-10 years.