What criteria do I use when picking the stocks I invest in? I try to keep it super simple. Some investors use complicated formulas and algorithms. I can tell you from experience that isn’t necessary. Being a great investor doesn’t require a high IQ. What great investors tend to share is a strong ability to think and to remain calm under pressure. There are simple steps a long-term investor needs to do to find a truly great stock that does not involve a ton of work or to analyze elaborate valuation methods.

Vision to see them

Courage to buy them

Patience in holding them

So how do you spot a great stock?

4 basic questions an investor must ask themselves:

Can the company do well, or even thrive during a black swan event? Think of buying a house. Would you buy a home that couldn’t withstand a storm or heavy winds? There is a reason why I do not have much invested in airlines or banks. Great companies not only survive but they can prosper during the most uncertain times.

Is there high insider ownership? This is pretty straightforward. Typically high insider ownership signals confidence, but it is kind of expected for the CEO or management to own a lot of the company stock. High insider ownership alone should not be a reason to buy a stock. Some of the best companies are founder-led, and typically have a symbiotic relationship with the company. They try to do the best thing for shareholders, even if that means devaluing their compensation or well-being.

Take the example, of the NFL. Kirk Cousins is one of the top-ten highest-paid quarterbacks in the NFL, and his salary makes up about 16.61% of his team’s cap space in 2023. The problem is there are 52 other roster spots on a team, and the Minnesota Vikings did not even make the playoffs last year. Compare that to Tom Brady, whose salary is about 10.96% of his team’s cap space. You cannot blame Cousins for accepting such a ridiculous contract however, he did his team no favors as his massive salary enriches himself personally but cripples the team’s salary cap.

Is the company financially stable? Key factors include cash available, debt, and free cash flows. Typically the more profitable the company, the more likely it would survive during a recession. There is nothing wrong with investing in a company that isn’t profitable or has weak financials, however, the risk level is much higher. Financially weak companies most likely cannot acquire other businesses or buy back their shares.

Does it have a moat? A moat is a durable competitive advantage. It is a barrier that keeps competitors from breaking through. A few key points about a moat:

- Most companies do not have a moat.

- Moats are sometimes not easily identifiable and are not permanent.

- Some industries are better at creating value than other industries.

Types of Moats:

- Government

- Network effect

- Being the low-cost guy

- Brand name

- High Switching costs

It is important to remember that all humans have biases and preconceptions. Investing is a constant process of inquiry and thought. When any rule or formula becomes a substitute for thought rather than an aid to thinking, it is dangerous and should be discarded. Do not get caught in the precision trap, as precise answers are not realistic or possible when making future assumptions or evaluations.

I read an interesting article about where you grew up, and people’s childhood surroundings determine your ability to navigate later in health. How you invest is very much a product of your upbringing and environment early on in life. How people evaluate stocks can be highly subjective and produce various differing opinions.

I will briefly go over 3 stocks that I would define from a qualitative perspective, as great. I am focusing mainly on the quality of the business and not market prices. These are businesses that can create tremendous value in the years ahead. For long-term investors, it is about being an island of stillness in a flow of treacherous waters. The value you get from your portfolio is created by simply holding quality companies for a long period. We have been conditioned to measure performance by quarterly performance, not business performance. Give these companies time, and I could see them flourish.

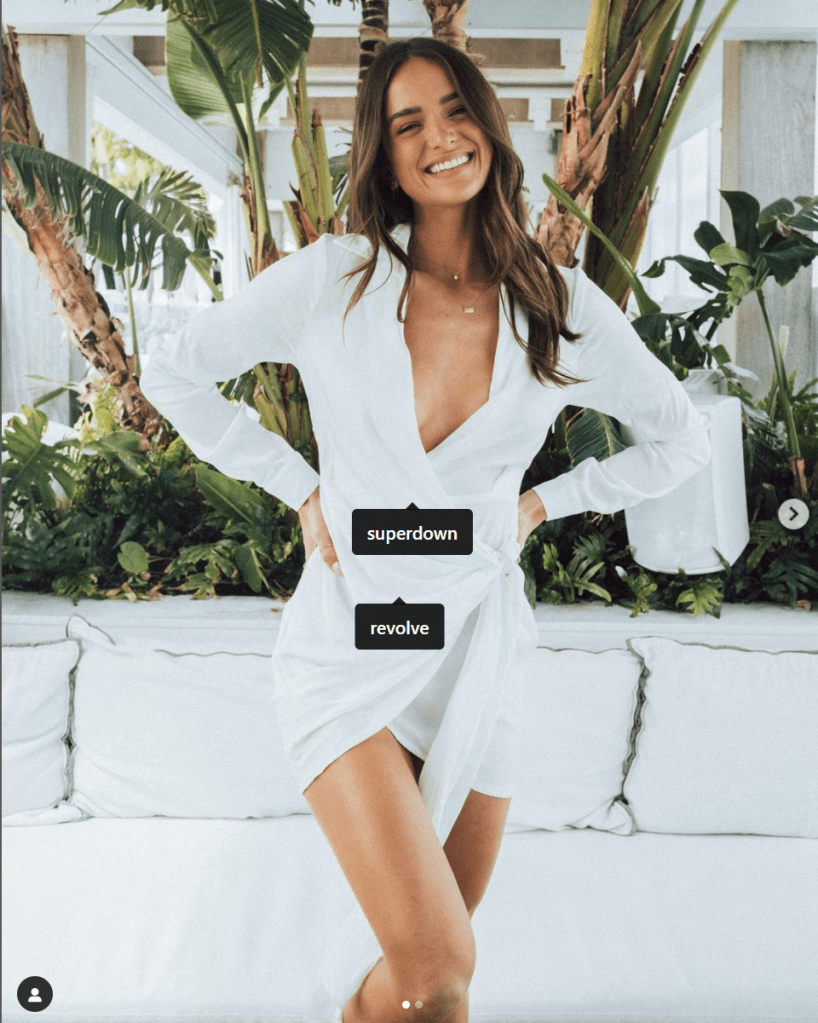

Revolve (NYSE: RVLV) Revolve Group is more than just an online fashion retailer. It is an agglomeration of brands, influencers, and designers. Just to give you an example, the influencer here has 1.6m followers on Instagram. Her dress was sold out in all sizes within the same day of the post. This influencer helenowen is also a designer, who has a line with Revolve. This is a win-win situation for all parties involved. When an influencer posts, Revolve makes money as they can create and order products based on real-time demand. The influencer benefits by having a platform to grow and showcase her brand. It is beneficial for super influencers like Helen Owen and Kendall Jenner. It works for nano-influencers. What’s even better is that influencers are essentially a renewable resource so Revolve doesn’t become hostage to one super influencer.

I have stated this many times, but I will repeat, Wall Street is still vastly underestimating this company. The brand is the moat. The brand is so strong, as they have a tight-knit community of influencers, celebrities, and customers. A great founder-led company with impressive growth numbers and already profitable. They can automate and map their inventory in real-time from their technology platform. This model will eventually be copied, but that could be a long time down the road. Revolve will experience exponential growth when its sales model is widely adopted.

- A strong brand ensures recurring customers and inspires loyalty

- Financially stable company – no real estate anchor

- The Total Addressable Market (TAM) is growing

- Not reliant on a specific customer, influencer, or designer.

Palantir (NYSE: PLTR) Very few companies can provide the service that Palantir does. They have an AI/ML infrastructure that makes sense of large data sets. Palantir is misjudged because people do not how to categorize them. This is why share prices have been all over the map. Many great growth companies like Amazon and Facebook, in their early-stage growth, have had similar issues. Was Tesla an automotive company, a technology company, or a pure-play on EV?

So what is it? Is Palantir high-growth tech or an overpriced consulting firm? I have said this before, but Palantir provides solutions to problems that companies do not even know exist yet. Palantir is in many ways the Nikola Jokić of stocks. There is no player in the NBA like Jokić, who was the lowest-draft player to win NBA MVP. On the surface, he looks like an unathletic big man that should ride the bench, but in reality, he is a star that passes like a point guard and can make 3-pointers. No NBA star plays like Jokić at his size (nearly 300 pounds). It is hard to evaluate Palantir because there has never been a company like them before, and their services are unique to the market.

- Risky now because they do not have a broad customer base.

- The Total Addressable Market is massive.

- Saas revenue model from Monthly Recurring Revenue (MRR) is highly profitable.

- High switching cost is a Moat.

Lemonade (NYSE: LMND) Chris Rock said in an interview with the Breakfast Club that unfunny comedy is a product of comedians who fear being canceled. Being a great comedian requires you to be a risk-taker. The same thing goes with being a great investor. If you do not take any risks, you will have guaranteed mediocre returns. Consider the average fund available to invest in has over 150 stocks, and those companies get turned over every year. Ask yourself, where is the edge in that?

Lemonade is a big-time risk. It is among one of the most hated, ridiculed stocks in the market. There is no timetable for profit however, the opportunity is massive. Right now, Lemonade is like a car halfway built. Evaluating Lemonade’s performance when its products are not rolled out nationwide is a bit shortsighted. Their future flagship product, car insurance, just launched in only their second state, Tennessee, last month!

Lemonade has a TAM, as big as any publicly-traded company. If Lemonade provides a better onboarding experience, offers lower rates, loses less on claims, and payout claims in minutes, it will gain millions of new users. For Lemonade, more users equate to more data points, and their overall network becomes smarter. This creates more efficient underwriting and accurate pricing. The scary thing is that the market for car, home, renters, pet, and life insurance is so big, that they don’t need to overtake State Farm or Geico to experience exponential growth. If they can just take a slice of the overall market share, the stock will be a 1,000% gainer in a decade.

- Powered by AI and using telematics allows Lemonade to undercut its competitor’s prices.

- The suite of products: car, home, renters, pet, and life being offered globally equals a large TAM.

- Potential of a Network Effect if consumers find Lemonade significantly better than its competitors.

- Social impact makes it different from traditional insurance.