The stock is down mainly because of intense macroeconomic factors and expected slowing consumer demand. The apparel section is primarily discretionary spending. If higher fuel prices and operating costs hit big players like Walmart and Amazon, a smaller company like Revolve will get hit even harder.

After listening to the earning call, my conviction has not changed. The company is still strong in the long term. I did not hear anything that indicates this company is in trouble, and they have a strong chance of coming out strong if the United States enters into a deep recession.

My takeaways from the earning call:

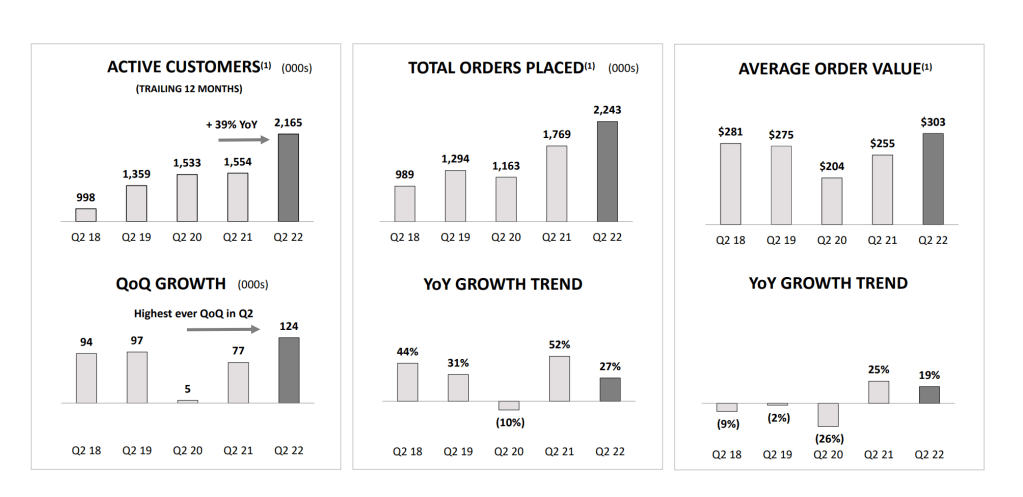

Key metrics are healthy: Revenue, Active Customers, Total Orders Placed, and Average Order Value.

The company is still growing, which is obviously important from a growth company. net sales were $290 million, which was lower than the $294.6 million expected. Not a big deal.

The Revolve brand is centered around consumers looking and feeling great and living their best life. And certainly, right now, consumers aren’t feeling that way.

Net income was the biggest issue, which can be attributed to rising fuel costs. Fuel prices have hit California harder than any other state, and Revolve is based out of Los Angeles. They can offer 1-day delivery time frames for many regions surrounding the Los Angeles fulfillment center.

The good news is that obvious macroeconomic headwinds will likely dissipate when inflation decreases. I believe current fuel prices are unsustainably high. Revolve is also operating its first east Coast fulfillment center, which should improve delivery times for customers on the east coast.

I did not hear anything on the call indicating a weakening long-term picture. In the short term, the company is challenged due to macroeconomic pressures. Still, from a quantitative standpoint, sales, revenues, and free cash flows are significantly higher from just three years ago.

This company would survive a recession:

The cash position on our balance sheet at quarter end was more than five times higher than our cash position three years ago — on June 30, 2019, just after we completed the IPO. And this cash generation was purely operational, without external financing. A clear and powerful indicator of our operating strength and scale.

Our team and technology are battle tested and have emerged stronger through this volatile period, and we are primed and ready for what lies ahead.

Companies you need to worry about during a recession do not generate free cash flow, do not have a pathway towards profitability, and have a lot of debt on their balance sheet.

Revolve is cash flow positive and has zero long-term debt. They are also not issuing new shares, which would dilute current shareholders. What I like about Revolve is that they have a clear pathway towards growth without having to sacrifice their balance sheet. I see this as good marriage between growth and value investors: Good long-term growth/revenue with stable financials.

There is no doubt that Revolve would suffer during a recession, and they would likely see a slowdown in sales. That’s not surprising, as if a best-in-class company like Amazon is getting hit during uncertain economic times, nearly every other company in the consumer discretionary sector would likely do worse. I am confident that a company like Revolve could navigate a recession due to its strong balance sheet. They have a lot of flexibility and options if the economy worsens. They also have a growing/loyal customer base, and most importantly, their demographic is affluent, a demographic which would be less affected by a worsening economy.

The covid lockdowns, in my opinion, were a more significant existential risk to Revolve than a looming recession. I would be more worried for companies like Farfetch or Allbirds (unprofitable, debt on the balance sheet) in this type of investing environment.

Revolve is a long-term winner:

And across the business, we will continue to invest heavily in our proprietary technology, which we view as a significant competitive advantage. Mike’s team is constantly building out internal technology to drive increased conversion rates and revenue, greater operating efficiencies, and an even better experience for our customers. For instance, within just the past few months, the technology and data science teams have developed proprietary internal applications that leverage machine learning and our rich data set to further optimize the customer experience and drive further operating efficiencies through enhanced fraud detection and package optimization. And on the site, we continue to elevate our personalization, product recommendations and search functionality, and recently launched an application that leverages machine learning algorithms to dynamically, and in realtime, recommend outfits for our customers to “complete the look.” We are in the early innings of leveraging AI technology with some exciting projects in the pipeline that we believe will both drive revenue and operating efficiency in the months ahead.

However, with the demand trends shifting during the second quarter, as discussed, our inventory balance ended the quarter in a place that is higher than we would like. While we feel good about the quality of inventory, the overall balance is elevated and we are working diligently to bring it back in balance.

I have talked about Revolve to death in the past and do not want to rehash things already repeated; however, the company has proven it is operationally efficient in managing its inventory.

Revolve is dealing with a slightly elevated inventory balance which is understandable given the supply-chain bottleneck and fizzling demand for consumer discretionary spending. Compare that to Walmart, which reported excessive-inventory issues. Walmart has a $356 billion market cap. A company of that size should be operating much more efficiently. Kudos to Revolve and their leadership for navigating these uncertain times and not having a glut of unsold dresses.

Lastly, Revolve is a winner because the most considerable thing Wall Street has wrong about them is labeling them as apparel only. They are building communities through social media and live events worldwide. Disney’s brand is so strong because they are not a product company. They sell experiences. I am not saying Revolve is on the same scale as Disney, but I could see them being on par with Lululemon, which has a $40 billion market cap.

Revolve can become a premier lifestyle brand and generate revenue through new avenues with a strengthening brand. Revolve ability to engage with consumers through social media and in-person events is unique. Very few apparel companies are doing this. It has a customer-centric approach through data, which keeps them on the pulse on what’s trending. Revolve has created a simpatico relationship with consumers, influencers, and designers on their platform, which not even Amazon has accomplished. They all love Revolve! Here is a recent quote from Khloé Kardashian, who partnered with Revolve through her Good American brand: “We love Revolve, we love their aesthetic, everything that they have to say, and then the fact that they’re picking up the core pieces of Good American in more sizes means a lot to us. And it’s a different set of eyes that get to see Good American and see how inclusive and fabulous we are.”

Recap:

- Operational excellence in inventory management: think like the Amazon of dresses.

- A strong balance sheet is unique for a company of its size.

- The trends show customers are most willing to buy clothing online over any consumer product.

- Growing loyal and engaged consumers through social media and in-person events.

- Personal brand momentum.

- Companies like Nordstrom and Macy’s cannot duplicate Revolve’s business model due to their bloated size (real-estate/# of employees).

- Proximity matters: Competing fashion companies would have trouble duplicating Revolve’s success if they were based outside of Los Angeles.

- Somewhat recession-proof. Default risk is very low, and they will have less competition if their less profitable competitors crumble during a recession.

- Still in the early innings of growth. Revolve is still very regionally-based. They will be significantly more profitable once they can reach nationwide and global reach.

Disclosure:

The most important thing I focus on is buying into quality companies. Valuation is important, but it is a secondary concern. I remember the famous quote from Benjamin Graham, “In the short run, the stock market is a voting machine, in the long term, it’s a weighing machine.” The actual stock price does not reflect the quality of a business and the work they do every day. Revolve is one company that I invest in because I see current shares being massively undervalued. Share prices do not reflect the quality of the business in its current state and are certainly not what they could be in the future. With my time horizon, I believe the probability is high that I will reap the rewards of what I have invested.

On a larger maco investment note, I am a long-term investor. As a long-term investor, I will suffer through nasty cycles where my portfolio suffers steep declines. In times of economic downturns, my portfolio will get crushed. I do not hedge my account. I do not buy on margin. My portfolio is mainly equity. I invest like this because I understand it is impossible to time the market. There is never a clear precursor to signal a market bottom or top. By having a long-term trajectory, I am fully guaranteed to participate when the economy starts expanding and companies rebound.

When I invest in a company, I ask myself two questions: Would I want to work there myself, and would I be okay being paid in company shares vs. a salary? The answer is two yes’s for Revolve. Employees are willing to work for bad companies as long as they are compensated well. The only reason why someone would be paid in shares of stock vs. a fixed salary is if they believed in the quality of the business. Revolve is a quality business. I have a long position in Revolve and may buy more shares soon. I have not sold one share in my portfolio since I bought the stock in 2019.