Randominvestorhttps://investinmyselfcom.wordpress.comThis is my personal blog about finances, the stock market, and investments. Disclaimer: I am not a financial advisor. Take anything I say for entertainment purposes only.

In 2016, I invested in Tapestry (TPR), betting on Coach as an undervalued brand poised for a turnaround. It was one of the first stocks I bought as a new investor. My thesis was straightforward: the stock could reclaim its March 2012 peak of $79.70. Nearly a decade later, my prediction proved correct, though the road was far from smooth.

Tapestry faced significant challenges, including the 2019 ousting of its CEO, the 2020 resignation of another due to ‘personal misconduct,’ and a 2024 court ruling blocking its merger with Capri Holdings. Yet, TPR has outperformed the likes of LVMH, Lululemon (LULU), Capri Holdings (CPRI), and Nike (NKE) over the past five years—the very stocks I eyed when TPR struggled. Those same peers now sit well below their prior peaks.

I acknowledge luck played a role. Had the Capri merger proceeded, TPR would likely be trading in the $50–$70 range today, far below its current levels. Now, with TPR soaring past its 2012 high, I’ve shifted my strategy and trimmed my position to lock in long-term gains. If the stock continues to climb, I’ll likely reduce my holdings further.

My original thesis—that Coach was trading at a bargain—no longer holds. In a tough luxury market, Coach has unexpectedly gained pricing power for a mid-tier brand, fueled by a reshaped brand narrative and the TikTok-driven success of its Tabby Bag. However, Kate Spade, accounting for about 15% of revenue, remains a weak link due to inconsistent branding and declining sales, tempering my optimism.

Management deserves credit for Coach’s turnaround, but I remain cautious. Tapestry’s cyclical nature ties its success directly to consumer spending and economic conditions. A weakening economy would likely pressure sales.

Tapestry’s acquisition strategy is my primary concern. Selling the unprofitable Stuart Weitzman brand was a smart move, but the pursuit of the Capri merger suggests management may doubt Coach’s standalone growth potential. Given the lackluster outcomes of the Stuart Weitzman and Kate Spade acquisitions, future M&A activity could increase debt and strain cash flow.

My suggestion? If Tapestry is set on acquisitions, it should issue new shares to fund a targeted purchase, such as a niche luxury brand with strong growth potential. This approach would preserve cash and avoid debt, though it risks diluting existing shareholders. It could create more long-term value than increasing the dividend or buying back stock to where it’s trading currently—an action that offers limited upside if the stock corrects.

While I’ve enjoyed reinvesting dividends during the stock’s recent climb, weaker economic indicators, like declining retail sales, suggest uncertainty ahead. Most companies in the consumer cyclical sector face headwinds from slowing spending, and TPR is no exception.

That said, TPR isn’t wildly overvalued. With an upcoming earnings report and Investor Day looming in September, short-term upside potential remains. I’m cautiously optimistic and will monitor these events. My goal is to sell more shares at a higher price before the end of the year.

Palantir redefined data analytics, while Gangnam Style redefined K-pop. Both achieved unexpected success through unconventional approaches, capitalizing on the right timing, transformative momentum, and cultural context.

Palantir, whose stock has surged over 400% in the past year, has become a focal point in the AI movement, despite its 20-year history. Similarly, Psy was already a veteran artist in South Korea, having started his career in 1999, 13 years before the global phenomenon’ Gangnam Style’ was released in 2012. The video eventually became the first on YouTube to reach one billion views.

Both share the same superpower: unorthodoxy, which helps them stand out in a competitive field. Palantir has unexpectedly fueled the spirit of AI-driven operations, just as Gangnam Style helped usher in K-pop on a global level. Alex Karp, an unconventional CEO, and Psy, the highly unconventional K-pop artist, embody this spirit of unorthodoxy.

Grappling with Valuation:

As a Palantir shareholder, am I saying this is the “peak” for the company? I don’t know. It seemed things were getting frothy when Palantir surpassed Lockheed Martin’s market cap; now it has a larger market cap than Lockheed Martin, Boeing, and Snowflake combined.

From a price-to-earnings or even price-to-sales ratio perspective, Palantir makes zero sense. While a projected growth rate of 36% is impressive, it falls short of what Zoom Communications achieved during the pandemic or what Nvidia has accomplished over the past three years.

It’s very possible that Palantir’s growth may have already peaked or is nearing its peak. I have little doubt, though, that the company has a long and successful future. However, I am highly uncertain if Palantir can grow enough to meet its sky-high valuation. Any signs of slowing growth could lead to a steep retracement. Any broader market correction or shift in sentiment could lead to a significant decline.

Even though I’m tempted to trim and sell more (if not all) of my shares every time the stock rises, it’s difficult to fight against momentum. Palantir is a profitable free cash flow machine, and its commercial business is in an early growth phase. The story remains compelling. There is little wrong with the actual fundamentals of the company; the focus of late has been predominantly on valuation metrics.

Lessons from Psy:

What Gangnam Style can teach us about Palantir is that a valuation doesn’t have to make sense to justify itself to keep rising. Momentum and narrative transcend numbers (even though Palantir’s numbers are solid).

As T-Pain said, words cannot describe how amazing the music video for Gangnam Style is. The video itself doesn’t make much sense, yet it has dominated globally:

This is an almost Dada-esque series of vignettes that make no sense at all to most Western eyes. Psy spits in the air while a child breakdances, sings to horses, strolls through a hurricane that shoots whipped cream in his face, there’s explosions, a disco bus, he rides a merry-go-round, dances on boats, beaches, in car parks and in elevators and generally makes you wonder if you have accidentally taken someone else’s medication.

I believe the numbers cannot fully capture the actual value of Palantir as a business. My brain struggles to grasp its market cap, and a voice within me says, “This is as good as it will get.” My heart tells me this growth story has a lot more breadth. It has the potential for a longer runway compared to unprofitable companies like Snowflake, CrowdStrike, and Cloudflare.

Perhaps this narrative about Palantir being grossly overvalued could be right and wrong at the same time. In the short term, Palantir is due for an inevitable and painful correction, but proves itself not as a ‘hype meme growth AI stock’ but more akin to a ServiceNow or Microsoft, where they are early in their business lifecycle and maintain a robust growth rate for an extended period.

Palantir’s story shows that powerful momentum can outpace solid fundamentals for a long time. Like Psy’s viral hit, its valuation may defy logic, but that doesn’t mean you sell the whole position. Stay disciplined: believe in the vision, but prepare for volatility.

Over the past two years, I have spent a lot of my free time gambling at the casino. I would experience the full buffett of offerings – blackjack tables, baccarat bets, craps rolls, roulette spins, sports wagers, and slot machines. The time spent on gambling has distracted me from more important activities like investment research. Overall, the experience was a slow bleed (surprise) on my wallet and created more negative expected value than any entertainment benefit I may have received. The silver lining is that I could reflect on this experience and re-examine my behavior with a more sharpened perspective, returning to my disciplined and patient approach to investing.

The Dopamine Trap: Chasing the High

I started gambling just to try it out. I was bored one night and willing to try something new. I had gambled once on a slot machine in my 20s. From starting this “hobby,” I could feel the anticipation build up, even driving to the casino. I knew from the start there was an issue because I sometimes would become irritated being stuck in traffic. I couldn’t get there fast enough. That’s the dopamine kicking in, which had always been highest before I gambled.

The reason I enjoy gambling is the exact reason I hate it: the allure of unpredictable outcomes, which causes a jerk in your emotions like a yo-yo.

I made my first sports bet on the Falcons vs. the Commanders and watched the game like a kid, living on every play. The game concluded in overtime, and I lost $700.

Betting over $100 on a single hand of blackjack.

Making over $1,000 in less than 15 minutues of craps.

Losing over $500 on a single roll of the dice in craps.

Losing over $1,000 in 7 minutes on a slot machine.

Winning it all back and more on a single $3 slot machine bet.

Even for a level-headed guy, this rollercoaster was dizzying. I chased losses for hours, blew past my budget, and felt the sting of regret more often than the thrill of victory.

The Mirage of “Getting Rich”

All gamblers want to make money. Unfortunately, gambling in the long run will likely lead you to lose money. A non-gambler (net return of zero) will beat 95% of the returns of all gamblers.

The reason most gamblers lose can be summed up very simply: The odds of losing money are much higher than the odds of making money. Even though slight, the mathematical advantage (house edge or vig) is likely insurmountable in the long run. Imagine the Los Angeles Lakers having to play all their games on the road, or the New York Yankees only allowed to carry a 24-man roster.

From a pure risk-reward perspective, every bet either carries too much risk that does not justify the reward like high coverage roulette strategies or the iron cross method in craps. Or the handful of wins does not overcompensate for the avalanche of losses you get from picking a few numbers on roulette or continuously grinding on a slot machine.

When I accepted that I was unable to beat the casino, gambling became much less appealing. Even with short-term variance and playing “smarter,” I finally admitted to myself that gambling is an inefficient way to make extra income and an even more unrealistic way to build wealth.

That’s why I chuckled when I heard a fellow gambler say, “I need to make smarter bets.” The reality is that “gambling smartly” or “responsible gambling” is an oxymoron. No matter how “smart” you play, the casino is built to outlast you.

When gamblers say this, they typically mean either making smaller bets or not going “full tilt.”

Whether you are betting in smaller increments or just a few large bets, the odds remain stacked against you. Betting with a smaller budget just means you are losing money less quickly. In the long run, the results will likely produce a negative return.

Naivety and Immaturity:

Some of you may be wondering how I can be so ignorant as to think I could prosper from gambling. I have made the “smart” decision to invest in Nvidia and Palantir early and continue to hold long-term. How could I be so gullible?

The casino often offers free food, play, gifts, and comped rooms to give the impression that you are winning. Many five-star resorts, like the Wynn or Venetian, provide a flawless, impeccable, best-in-class guest experience.

Winning several jackpots (over $1,200 on a single win) on slot machines has distorted my analytical thinking, providing a false sense of confidence in games where you have zero control based on random events.

I vastly underestimated how the casino environment clouded my discipline and made me more comfortable taking unnecessary risks.

Going to the casino was not purely motivated by financial gain but by the dopamine hits and escapism.

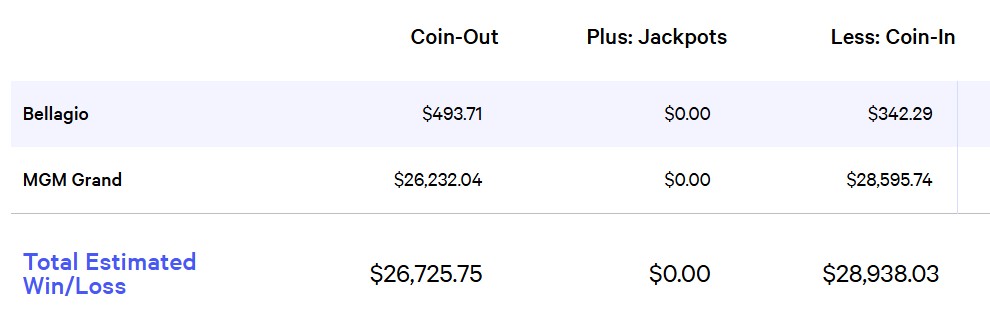

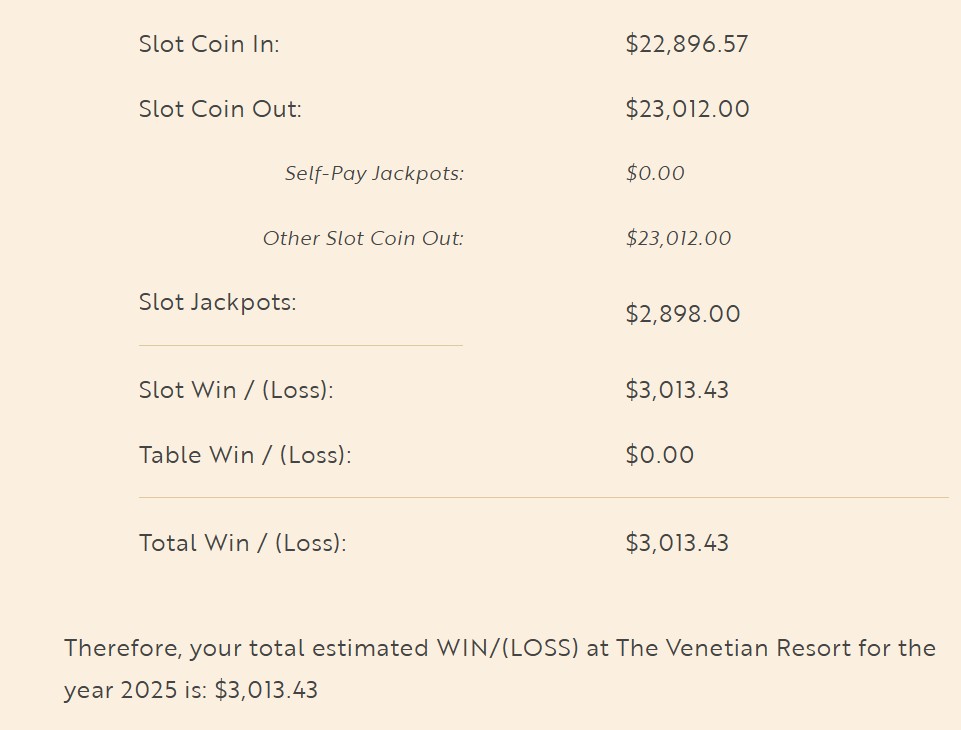

It wasn’t just about money. I was chasing dopamine hits and an escape from reality. Tying my checking account to sparkly animations or a dice roll feels absurd. My Las Vegas coin-in/coin-out statement? Humiliating. My local casino doesn’t even provide a detailed win/loss record, which only adds to the haze.

Reflection and Moving Forward

I am a super competitive person. Playing games where the advantage is not in my favor seems unwise. It is even sillier to build wealth based on sparkly animations on a screen or a random roll of the dice.

Since diving into gambling, I’ve lost about $5,000. To some, that’s pocket change; to pro gamblers, it’s amateur hour. My investment portfolio sees bigger swings daily. But here’s the potential impact: if I’d put that $5,000 in the S&P 500 five years ago, it’d be worth over $10,000 today. In Nvidia? Try $85,000. Instead, I’m down $5,000, with nothing but fleeting thrills and a gambling hangover to show for it—those mornings after a big loss when I’d rather call in sick from work than face the day.

Do I have a gambling problem?

My Problem Gambling Severity Index score of 6 flags me as moderate risk—not an addict, but not out of the woods. I’ve never touched debt or my investments to fund bets, and I trust my mental resilience to keep me grounded. Will I quit for good? Honestly, I’m not sure. Gambling has some entertainment value, but often feels like a second job. I’m too competitive to play without obsessing about how much I am up or down.

Investing vs Gambling: Two Different Games

Since gambling is a game of chance, you will often get variable outcomes. I have chased losses (not advisable) and won jackpots. I have doubled down on hands, risking my entire bankroll, and beat the dealer.

Could a hyper-disciplined “Rain Man” gambler break even or profit? Sure, it’s possible. But probable? No. And even if you’re that rare winner, is it worth the grind? There’s a smoother path: open your brokerage account, buy an index fund or a solid stock, and let time do the heavy lifting.

The casino’s relationship with you is a one-way street—it wants your money, not your success. No amount of complimentary cocktails or VIP perks changes that. For the broke, it’s a poverty trap. For the rich, it’s a slow drain. For everyone, it’s a time suck. Investing, though? It’s the greatest show on earth. Analysis and patience build wealth with the odds in your favor. It’s not as sexy as a jackpot but rooted in real economic value, not chance.

Be the Casino, Not the Gambler

“Well, it requires patience — which a lot of people don’t have. People would much rather be promised that they’re going to win [on] a lottery ticket next week than that they’re going to get rich slowly. Gus Levy used to say that he was long-term greedy, not short-term greedy. If you’re short-term greedy, you probably won’t get a very good long-term result.”

— Warren Buffett, preaching the gospel of patience

Early in life, I learned that investing is the true superpower in building wealth. For long-term investors, you have the house edge.

There are three main advantages investing has over gambling:

Control over risk: You choose your investments and manage exposure.

Purpose: You’re building wealth, not chasing chance.

Positive expected returns: Over time, markets trend up.

No poker pro has built a billion-dollar fortune from cards alone. Nevada’s richest? Miriam Adelson is worth $28 billion thanks to owning casinos. Want to win like the house? Invest in it. Stocks like MGM Resorts or Wynn Resorts let you own a piece of the action.

MGM Resorts International also presents a potential bargain. Its properties are valued at over $38B, exceeding its $8.77B market cap, suggesting the stock is also undervalued. Its steady share buybacks and Las Vegas focus make it a safer bet. If MGM Osaka is a major success, its business can find a new avenue for growth and become less reliant on Las Vegas tourists.

Wynn, with a market cap between $7.16B and $10.29B, carries more risk—negative equity and a high debt-to-equity ratio—but its premier luxury brand and global expansion (like Wynn Al Marjan Island in the UAE) offer serious growth potential. Wynn’s rooms cost 20-50% more than MGM’s, and the “wow factor” is unmatched. The sum of its current property values over $20B significantly exceeds its market cap, suggesting the market may not fully price Wynn’s assets.

Both are cyclical and tied to the global economy, but gambling’s demand is insatiable. With new markets opening in the UAE and Japan, casinos like MGM Osaka could spark a Vegas-style boom.

Forget scrolling through TikTok gambling influencers or waiting in line for electronic roulette. Spend a few hours researching. Investing in the house—not betting against it—is how you build real wealth. My casino days taught me a hard lesson: chasing quick wins is a sucker’s game. Let time and strategy tilt the odds in your favor.

The secret isn’t so much a secret. As Warren Buffett noted, short-term greed is unlikely to produce good long-term results. I was being short-term foolish, and fortunately, the damage is repairable. I will revert to being patiently long-term greedy.

Reflecting on my own experience, the seismic movement in Palantir’s stock price YTD led me to sell my original cost-basis two years ago. This decision was not made lightly; it seemed reckless not to convert some gains into actual profits.

A few thoughts:

Investing isn’t an exact science. A good story stock with solid fundamentals can sometimes have wild meteoric rises. The talent scouts who discovered Taylor Swift as a teenager probably couldn’t foresee what she would become today. Scouts watching Aaron Judge hit at Fresno State probably did not forecast his ability to hit over 50 home runs and bat over .300 an entire season. Companies can far exceed even the rosiest of expectations because a. the stock market isn’t static, and b. catalysts that propel a stock upward are not visible on a balance sheet.

Palantir has solid fundmantels. Although the upward volatility is similar, it isn’t a “meme” stock in the same vein as Gamestop or AMC. Long-term investors should consider this an investment, not a trade.

The stock is riding on euphoria in the short term, and traders are piling in on the AI wave. Even institutions or “smart money” ignore valuation and are piling in to catch up on AI. There is no way to predict how long this roller coaster ride up will last, but sentiment and “vibes” are variable factors. As good as a company’s fundamentals are, Palantir is punching well above its weight class by almost every financial metric, which creates a situation in 2025 where the actual earnings results won’t justify the current stock price. Investors buying the stock at these prices could be severely disappointed 6-12 months from now with demanding Year-Over-Year comparisons.

Palantir’s market cap has surpassed Lockheed Martin’s (if you are reading this now, it could have doubled), which indicates an overextended stock. Based on revenue and net income, the stock is overvalued today.

Why won’t I liquidate my entire position and try to buy back at a better price? I have a much more long-term mindset and believe Palantir will eventually grow into its valuation. I am willing to ride the inevitable wave downwards but concede that at least some profits need to be taken to build a more significant cash position for the potential of a better buying opportunity in the future.

Company

Q3 Revenue 2024

Net income

Adjusted EPS (USD)

Palantir

726 million

143.52 million

0.10

Lockheed Martin

17.1 billion

1.62 billion

6.80

Looking at the bigger picture:

High stock prices can lead to wildly optimistic, unrealistic expectations where investors do not consider things going wrong.

Cash is the lifeblood of any portfolio. Trying to build a cash position during a downturn is often a reactionary emotional response and not ideal. It’s crucial to maintain a balanced portfolio with a healthy cash position.

Cashing in on 500-1,000% long-term gains can seem like a victory, but I urge investors to be careful. Palantir’s focus on emerging technologies like AI and data analytics positions itself well for future growth. Anyone investing in this company should have patience (which most investors do not have) and a high-risk tolerance. It is overvalued, but the commercial business and AIP are in their infancy. As an investor, Palantir is a rare diamond. It is too valuable to avoid having this cash-compounding multiplier in your portfolio. At the same time, by not selling at least some gains, if the stock were to pull back significantly, it would be as if this rally and your paper gains never happened.

This rapid move-up reminds me of Nvidia from 2016 to 2018. Even for the best-performing company in the world, investors were given windows of opportunity to buy back in at more reasonable valuations later on. I am confident we will have similar retracements with Palantir.

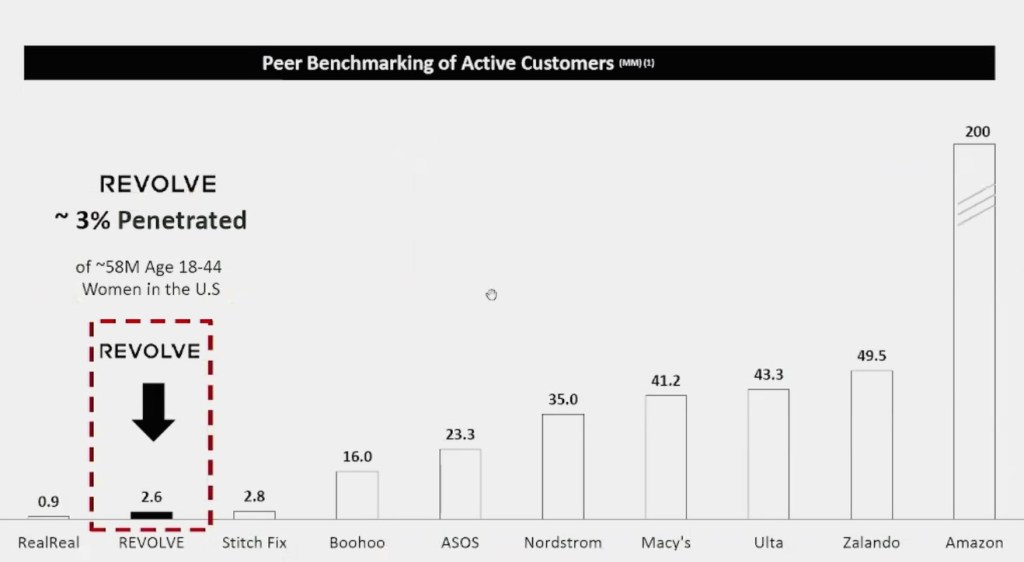

Revolve Group:

The biggest position in my portfolio from a total cost basis, I am optimistic about where Revole is headed in 2025. My stance on the fundamentals of Revolve has remained the same:

It’s not a homerun investment but a solid double

There is no single catalyst to propel exponential growth, and there are no glaring red flags or company-specific risks that would cause me to panic.

Guided by two co-founders with an entrepreneurial vision, no debt, a history of profitability, and a proven business model.

I remain patient because the growth strategy remains intact. Revolve’s biggest competitors are Nordstrom and Macy, legacy companies with the same problem: an inability to attract a Millenial and Gen Z audience. For a luxury department store, this is an existential looming threat.

Big Department store chains have become stale and lack the nimbleness to pivot their business models. Macy’s and Nordstrom likely need to leave the public markets to stay afloat, which is an excellent opportunity for Revolve. While most department stores need to downsize their retail footprint, Revolve’s brand is growing, and its presence in physical retail is just starting.

Some investors may feel this growth story is not appetizing enough, but I see a clear and easy opportunity. Among its e-commerce peers, it’s one of the few growing and GAAP profitable. Revolve isn’t trying to reinvent the wheel, like becoming “The Uber of the Skies” or “Revolutionizing Fitness.” Doing something never done before in investing comes with a higher reward but much more risk. The history of profitability gives me enough assurance to bet that Revolve will be a steadily growing winner.

I am cautiously optimistic. Many analysts are sleeping on Revolve, a small market cap company, becoming an emerging brand set for impressive results in the next decade. Their legacy competitors are in apparent crisis mode. At the same time, most of their e-commerce peers in the luxury industry lack the same financial and brand strength.

Devon Energy:

A position I started recently, Devon Energy, provides great diversity for investors looking to add value and non-tech growth to their portfolio. Oil and gas are highly cyclical commodities, but investors shouldn’t confuse cyclicality with speculation. The price of oil constantly fluctuates. Although oil stocks are sensitive to macroeconomics and geopolitics, Devon is among the best companies in the oil industry.

Reduction of expenses and increase in efficiencies from the Matterhorn Express & Blackcomb Pipeline.

Increase of oil production from the Grayson Mill Energy acquisition.

Dirt-cheap valuation with a strong balance sheet and consistent cash flow.

A company aggressively buys back its stock when said stock is deeply undervalued

An attractive variable dividend that allows investors to be long-term patient.

A “green light” from the Trump administration (less regulation and taxes) that Devon could benefit from significantly.

Companies in the energy sector aren’t every investor’s cup of tea, but building a robust portfolio requires some diversification and value. Although having an asset’s value strongly correlated to oil price may seem risky, investors should consider this a hedging investment rather than just a hedging tool.

I am not a big fan of derivatives or “buying insurance” in your portfolio other than cash. But if you are overweight tech, having an asset that can move up, even with rising interest rates, is quite enticing. Also, suppose you have positions for which you have a deep conviction that you would rather not sell in your portfolio. In that case, Devon Energy can be a great addition to your portfolio because it generates income and will likely rebound when oil prices fluctuate higher. From a long-term viewpoint, the price of crude Oil WTI today is neither high (140.00 in June 2008) nor low (18.84 in April 2020). It could be a good time to start a position in Devon Energy or other oil/natural gas energy companies, with their value being fair-to-good in the near short term.

Pfizer/Moderna:

Every investor has to prepare for the inevitable “truths” that will impact their portfolio: Recessions, pandemics, natural disasters, and geopolitical events are unavoidable and will happen again. Investors must stay disciplined during volatility and take preventive rather than reactionary measures before catalyst events happen. The latest information regarding H5N1 is quite alarming.

My current goal is not to put new money into something already expensive and hope it becomes even more expensive. A long-term investor needs a strategy that fits their goals instead of following a trading strategy and succumbing to behavioral biases of only buying stocks when they go up.

While the market is overweight in AI, I have been building and diversifying my portfolio over the past year by adding energy and biotech.

Pfizer is a more established biotech company that has made a big bet on oncology (cancer). Although the transition has been slow, I expect meaningful breakthroughs with cancer drugs in the next five years.

Moderna carries much higher risk and more significant potential rewards. Its focus isn’t on a specific drug approval but on utilizing AI and mRNA technology to create a “bioplatform.” If it succeeds, Moderna has the potential to unlock the holy grail for pharmaceutical drug companies. Vaccines and drugs that do not have patent expirations (assuming Moderna owns the mRNA vaccine intellectual property). A lot of this comes with unknowns and “ifs” with this bull thesis; however, we already know through data and science that mRNA technology works, and the reward is high (essentially a potential 100x payoff) with probabilities much higher than lottery odds.

Quick hits:

Hims & Her Health—I cannot fully grasp what will give Hims a long-term competitive advantage beyond branding and slick marketing. A brand’s impact on purchasing behavior in apparel works quite differently in telehealth. Your friends and social circle may care what and where you buy your clothes from; I don’t think it matters much with weight-loss drugs and erection pills. I am not bearish on Hims; just unsure how sticky brand loyalty will work in a B2C subscription telehealth platform.

Lemonade—Too early to sell. Investors should wait until Lemonade fully launches its car insurance product nationwide. Unlike most companies I write about, Lemonade has never been profitable. It will stay that way for the foreseeable future. It will remain a small position in my portfolio, but the company seems to be moving in the right direction. Like Roblox, these companies are about a potential story unfolding. The potential reward is a significant return based on a small initial investment. Look at it like a small fire; it could slowly burn or escalate into a major blaze. The stock is volatile and remains higher on the risk scale.

Nike—The turnaround story remains in play. Although sales have declined and the overall brand has stagnated, I am confident that the new CEO, Elliott Hill, can get Nike back on track. Although it seems like a somewhat oversimplified thesis, Nike should benefit from a Caitlin Clark halo effect. Clark was named Time Magazine Athlete of the Year and #100 on the Forbes 100 Most Powerful Women. I believe it is a safe bet Clark will rise up this list, as she is not even at her athletic peak. Clark’s fandom/demand is simmering, and Nike is known to historically promote and market athletes better than any other brand. It will be hard for Nike to screw this up.

Mercadolibre—I remain bullish. Most investors associate Mercadolibre with e-commerce, as it is the most valuable company in Latin America. Its strong infrastructure has created a fortified moat to protect itself from Amazon and other competitors. Next up is becoming the premier fintech bank in Latin America by leveraging its online ecosystem to extend into financial services. Mercardo Pago may never catch up to Nubank; it doesn’t have to. Mercardo Pago is penetrating a large market, and its competitive advantage comes from its ecosystem integration, much like how AWS benefited significantly from its integration with Amazon’s online business. The momentum and growth indicate that Mercado Pago will one day drive most of Mercdaolibre’s operating income, just like AWS does for Amazon. I am not bearish on Nu Holdings, but they are a pure fintech play. In contrast, Mercadolibe has several potential growth levers to pull, making it a superior investment.

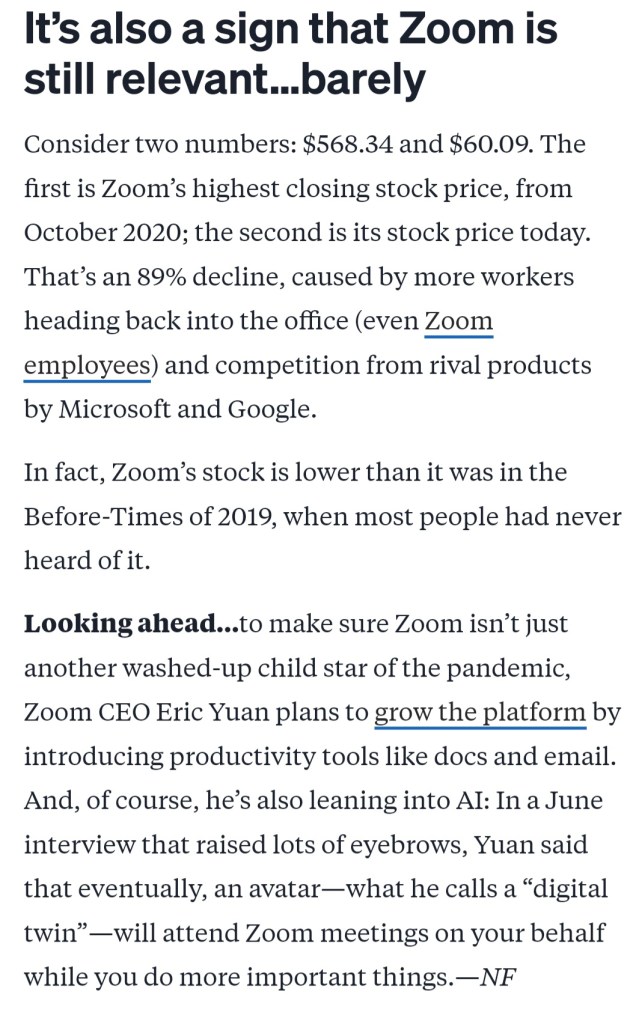

After Joe Biden dropped out of the 2024 Presidential race in July, something notable happened: Zoom, the videoconferencing app, was used as a political rally call for Kamala Harris. On a Thursday summer night, a Zoom fundraiser attracted more than 200,000 viewers, making it the largest Zoom call in history. Several other Zoom fundraising calls have followed, started by diverse communities like “White Dudes for Harris,” “Dead Heads for Harris,” “Cat Ladies for Kamala,” and “Swifties for Kamala.”

I am not interested in discussing Harris’s surge in popularity but in why her supporters decided to use Zoom instead of Google Meet, Microsoft Teams, or Webex Meetings.

Investors in Zoom should feel confident in the business. Zoom’s death as a pandemic company is greatly exaggerated. The stock appears hated, I guess it’s a symbol or a vestige of a depressing moment in history, yet the fundamentals remain intact.

Zoom is the people’s choice because, through empirical testing, its audio and video quality ranked higher than its competitors.

Due to its ease of use, consistency, and complete/advanced features, it also flexes its brand power, even over Microsoft and Google.

Why does this even matter?

Despite the exceptionally bearish sentiment from Wall Street and the financial media, Zoom has proven its resilience. Sentiment, after all, is subjective and can quickly turn around as expectations and emotions change. This should reassure investors of Zoom’s potential.

Perhaps the narrative of Zoom being a pandemic boom-and-bust company is incorrect. The business is operating just fine and taking the necessary steps to transition from a popular one-trick video conferencing app to a full-fledged AI enterprise platform.

The video conferencing space is crowded, with heavy hitters who do not have the same relevance as Zoom on a consumer level.

How many people do you know to use Microsoft Teams outside of a work setting? Shouldn’t Teams or Google have more relevance or usage if it has the same functions and capabilities as Zoom?

Since Zoom is an enterprise tool, consumers downloading and using the app don’t move the needle or meaningfully impact the balance sheet.

It creates a halo effect for the enterprise business and enhances brand recognition.

Zoom is not a social media platform, yet it has brought an impressive amount of users for fundraising purposes, creating a sense of community and energizing supporters.

Unnecessary negative-slanted wording from a Morning Brew newsletter

If Zoom can impact an election and help elevate a candidate into the presidential office, something about the platform gives it a potential competitive advantage with a long-term wide moat. You can argue that Zoom cocktail parties and Zoom Yoga sessions are more of a pandemic-era fad, but affecting voter turnout is much more impactful.

Despite the recent downturn in Wall Street’s sentiment, I remain optimistic about Zoom’s long-term potential. The demographic most comfortable using the platform will eventually dominate the workforce, while those resistant to technological change will phase out. This bodes well for Zoom’s future growth.

Zoom’s platform is not just a tool; it has gained cultural phenomenon status. It’s the preferred choice among Gen Z across various industries, from education to healthcare, legal, events, government, and personal use. Understanding this trend is crucial for anyone interested in technology and its impact on society.

Zoom meetings, classes, and virtual court hearings are here to stay because they are widely popular, in high demand, and in a growing market.

Strong balance sheet: Zoom has approximately$7.5 billion in cash and zero debt. Roughly 40% of the company is cash (cash divided by enterprise value), signaling a high margin of safety. Compare that to Salesforce, which has an enterprise value of about $274 billion, $10.6 billion in cash, and $40 billion in debt.

Founder-led with strong key executives.

AI-infused with innovative ideas like AI avatars that trend towards the future of enterprise work tools.

Popular among a demographic that will make up most of the workforce in 10-20 years.

Zoom has become a popular company to “hate on” from Wall Street for various reasons that I believe are mainly irrational and short-sided. I fully expect Zoom to see a lift in revenue and guidance due to its solid fundamentals and riding the right enterprise software trends. If this happens, the narrative of how the company will dramatically shift more positively.

I wouldn’t call what Zoom has a network effect, but the virality appears very sticky. An enterprise app that transcends enterprise and has a profound impact on society outside of just business. Zoom is an attractive investment with much of the downside risk already priced in.

Once the undisputed athletic apparel champion, Nike has faced increasing challenges recently. With Mark Parker’s departure and John Donahoe’s subsequent leadership, the company is struggling to keep pace with rapidly changing consumer preferences, particularly among Gen Z and Millennial demographics. The stock has seen a significant decline, underscoring the urgency of the situation.

A New Playbook

Starbucks’ revival under Brian Niccol’s CEO appointment is a powerful example of the transformative potential of strategic leadership change. Nike, too, could benefit from a bold and quick decision, emphasizing the need for risk-taking in order to reap potential rewards.

Sheryl Sandberg: The Perfect Choice

With her experience as Facebook’s COO, Sheryl Sandberg possesses a unique blend of skills and insights that are directly relevant to Nike’s current challenges. Her deep understanding of social media and her passion for women’s empowerment aligns perfectly with the company’s visions and goals, making her the perfect choice to lead Nike into a new era.

Leveraging Women’s Sports and Social Media

The growing popularity of women’s sports, exemplified by the rise of athletes like Caitlin Clark, presents a significant opportunity. Nike can tap into a powerful cultural force by investing in women’s sports and leveraging social media to connect with younger audiences. As a female executive who has broken barriers in the tech industry, Sandberg is well-positioned to champion women’s sports and empower female athletes.

Cultural Understanding

According to a recent survey, 40% of Gen Z and Millennials find women’s sports more exciting to watch than men’s, compared to about 25% of Gen X and Baby Boomers. Moreover, social media has become integral to how consumers engage with sports. Six in 10 Zoomers are very interested in content creators on Twitch or YouTube chatting about sports on live streams, and 70% discovered or deepened interest in sports through fan communities on social. This indicates a significant opportunity for brands to leverage social media to connect with younger audiences.

A Game-Changing Move

Sheryl Sandberg’s leadership could be the game-changer Nike needs to regain its cultural relevance and standing. Her proven ability to drive revenue growth, build strong teams, and foster a positive company culture would be invaluable in navigating the challenges of a rapidly evolving market, instilling hope and optimism in the company’s future.

Sandberg’s expertise and track record are based on optimizing and fine-tuning advertising revenue. She can create a more effective ad strategy, creating engaging and shareable content that builds communities and drives engagement.

The Time is Now

By bringing Sheryl Sandberg on board, Nike would signal its commitment to innovation and demonstrate its understanding of the changing landscape of sports and consumer behavior.

Caitlin Clark’s meteoric rise is changing the narrative of how we talk about women’s sports and how to market women athletes effectively. It’s a shift that’s happening now. Nike needs to adapt quickly, and bringing in a proven winning rockstar CEO can dramatically turn things around.

I endorse giving Sandberg a blank check to turn around Nike. John Donahoe is the wrong CEO to revive the brand. Sandberg’s background in technology is not directly relevant to the athletic apparel industry, but Nike has never been just an athletic apparel company—it’s a global cultural brand that celebrates great athletes. This is the right time, and Sandberg is an even better fit. I urge the Nike board of Directors to take action because quite, honestly, it makes too much sense.

Despite Nike’s current slump and the deserved hit its stock has taken, the growth potential is significant. Many of the issues are fixable, and with Nike’s robust financial and brand muscle, it can weather these storms, even a potential recession, as it did in 2008. Nike’s infrastructure and ecosystem have been stress-tested for decades, a testament to its resilience.

You won’t find it here if you’re seeking a deep security analysis of Nike Stock with a sophisticated review of Nike’s business. But that’s not a cause for concern. Nike is a simple business, and my investment thesis is relatively straightforward.

I am bullish on Nike because Caitlin Clark has the potential to propel it into a new hyper-growth phase, similar to the impact we saw with Michael Jordan in the 1980s and 1990s. This growth potential seems evident (the right time and place) for a magical story to unfold.

When Wall Street talks about Nike, it seems rather blah. Where is the creativity or outside-the-box thinking? Almost everyone analyzing this company is talking about the wrong thing. Nike can be summed up simply through a Steve Jobs quote:

“The best example of all, and one of the greatest jobs of marketing the universe has ever seen is Nike,” Jobs explained. “Remember, Nike sells a commodity. They sell shoes. And yet when you think of Nike, you feel something different than a shoe company. In their ads, they don’t ever talk about their products. They don’t ever tell you about their air soles and why they’re better than Reebok’s air soles. What does Nike do? They honor great athletes and they honor great athletics. That’s who they are, that’s what they are about.”

It’s not about the shoes; it’s about the people wearing the shoes!

It’s that simple.

A shoe is just a shoe. Proprietary shoe technology doesn’t move merchandise. Nike is an aspirational lifestyle brand. No other company in the world does a better job selling and promoting great athletes. They have an invisible superpower in their brand value, an intangible asset that drives a high level of engagement in selling apparel, shoes, and merchandise.

Nike isn’t the company it is today without Michael Jordan, who signed a five-year, $2.5 million deal in October 1984.

The contract was an absurd overpay for a basketball player at the time. Yet, now it looks like a slam dunk for Nike because Jordan transcended basketball and became a global cultural phenomenon.

The NBA and Nike didn’t elevate Jordan; it’s the opposite. The Jordan brand elevated basketball and sneakers to new heights. His sponsorship with Nike turned into a billion+ industry.

Nearly 30 years after Jordan signed with Nike, Clark signed an eight-year deal worth $28 million. This deal is bafflingly low for what could be a future brand worth $1-5 Billion.

Nike stock appreciated over 1,000% from when they signed Jordan to when he retired for the first time in 1993. It gained another 100% from when he returned in 1995 to when he retired for good in 2003.

In the story unfolding with Caitlin Clark today, we are witnessing the early stages of another cultural phenomenon that undeniably impacts culture.

How Clark can elevate Nike:

The Clark Effect:

A name that is trending up: Clark transcends sports. Very few athletes trend like this with long-term staying power. We already see this in the WNBA, a sport with an extremely niche following pre-Clark. The fanbase was small, with fans not spending “big” money on the product. That is changing.

Clark is now part of daily sports talk shows and debates. The more people talk about it, the longer it remains relevant and stays in the mainstream discussion.

Record WNBA attendance and viewership:

When the Indiana Fever played the Los Angeles Sparks, 19,103 fans attended Crypto.com Arena. That was more than the largest home game crowd for the Los Angeles Lakers, and LeBron James drew 18,997.

The cost of Indiana Fever tickets has doubled and, in some marquee matchups, nearly tripled compared to last year!

WNBA games are averaging 1.32 million viewers, almost tripling last season’s average of 462,000.

The WNBA has expanded, adding two new teams: the Golden State Valkyries in 2025 and a Toronto team in 2026. More stars will join the WNBA in the next four years – Paige Bueckers, Juju Watkins, Hannah Hidalgo, etc.- which will increase viewership and the league’s star power.

Based on ESPN personalization data, the WNBA has seen the largest YoY growth (+47%) among sports with 1M+ favorites

Caitlin Clark led all players with +373% MoM growth to become the 4th most-favorited active athlete, only behind LeBron James, Tiger Woods and Steph Curry

She is only trailing LeBron James, Stephen Curry, and Tiger Woods. Clark could quickly ascend to #1 in the next 3-5 years as the most famous athlete today, just entering her physical peak. The top three athletes in this list are nearing the tail end of their respective careers.

She’s a superstar:

We have seen hyped-up college athletes like JJ Redick and Jimmer Fredette before. We have witnessed Linsanity in the NBA and Tebow Mania in the NFL. None of these players were superstar athletes on the pro level, and their fandom eventually diminished.

No checkered past with a pristine record:

Clark seems similar to Jordan, a no-nonsense athlete intensely focused on basketball and obsessed with winning. No demons or scandals that diminished or brought down other athletes – Kobe Bryant, Johnny Manziel, and Michael Vick come to mind.

I don’t see Clark posting dances on TikTok or starting her podcast. She’s not an activist who is getting involved in politics. Eat, Sleep, Breathe, and play basketball. There are no distractions.

A new brand within a brand: Bigger than Air Jordan?

Clark already has a rabid, dedicated, and obsessive fanbase. Comparing Clark with LeBron James or Stephen Curry is the wrong comparison. Clark’s brand is more similar to that of Taylor Swift and Barack Obama.

Swift can make her fans spend over $1,000 on a non-premium seat ticket for a show and make them feel they are getting a reasonable deal.

Obama brought in millions of first-time voters to vote for him because (insert whatever reason you believe is correct) he propelled himself to a cultural phenomenon status.

A market largely untapped by Nike:

Nike’s women’s segmented business makes up just 22% of its sales.

Think of all the girls and women who want to buy Clark’s shoes. The market is largely untapped. Nike is seeing early success with Sabrina Ionescu and the Sabrina 1, a top ten WNBA player.

Clark’s brand could evolve beyond sneakers and boost Nike’s lifestyle segment into an entire product line of different types of shoes, socks, tracksuits, etc.

Identity with mass appeal:

Victor Wembanyama is a French basketball player and could be the best men’s basketball player in the next five years. He is also a Nike athlete, but I don’t see him coming close to bringing in what Clark does. “Wem-bany-am-a,” the name isn’t catchy or memorable. “Clark’s” is already a well-known popular shoe retailer in the UK. Besides the name, Clark is from the heartland and plays in the heartland.

I am not knocking Wembanyama or Ionescu as athletes, but like performers, style points matter in our culture. The top recording artists aren’t the top vocalists. Popularity and fandom are more a feeling than a rational thought. Competitive sports fall into a performance art category. What you won’t hear on CNBC or Bloomberg is the intrinsic relationship between Clark and her fans in the arena and online.

Get in while you can:

Wall Street will react once the shoe is released and the numbers are in an earnings report. I am getting in now. As we saw with Jordan, this feverish support can last for years, even decades. I see a noticeable halo effect for Nike, and this is like investing in Taylor Swift if she were a stock in 2010.

What I also love about this investment is that it isn’t binary. It could be a solid long-term investment rather than a trade.

Nike’s dividend (1.96%) is low, but given its financial health, it is well-covered by earnings and has increased over the past ten years. This trend should easily continue in the next ten years.

Nike trades at about 21x forward earnings. There is no expected earnings growth this year, so the stock is cheap (for a growth company) and reasonably priced, with low expectations.

Nike has a solid business that doesn’t need saving, but Clark could elevate the brand to a level that even Nike executives do not anticipate. A signature shoe deal was originally off the table during the initial negotiation, showing skepticism about the confidence that a shoe line by a female basketball player could drive sales. At this point, the skepticism doesn’t matter. It would be hard for Nike to mess things up and not capitalize on Clark’s meteoric rise in fame.

The biggest question is whether men will buy Clark shoes. I empathically believe yes. Hype and cultural shifts are not gender or even age-exclusive.

Take, for example, Donald Trump, who has said deplorable things against women. His actions against women have been equally disgraceful, yet he has millions of supporters who are women.

Taylor Swift’s fanbase is distributed uniformly across various ages. Almost half the people who attend her concerts are over 45, and her fanbase is almost evenly split 50-50 between males and females.

Humans are generally programmed to follow a herd. The more popular Clark becomes and achieves on the court, the more valuable her brand name becomes, making her a powerful force in selling merchandise to anyone worldwide, not just sneakerheads or young girls.

Even if Clark flops, this isn’t an all-or-nothing type of risk. The business is highly robust. Nike has missed trends and made mistakes in the past, but it always recovers because it excels at sales and marketing better than almost everyone else. If there is lightning in a bottle with Clark, Nike will know how to maximize sales. That’s what they do.

Nvidia has demonstrated an impressive growth trajectory, surging nearly 2,200% from $6 to briefly touching $140 in under five years. This meteoric rise even saw it surpass Microsoft as the most valuable stock in the market for a brief period.

Long-term investors, your perseverance and discipline have paid off. You’ve demonstrated two of the most crucial traits of successful investing: patience and discipline. While many struggle to hold a stock for even a year, you’ve shown the strength to hold on for much longer. This is an achievement worth celebrating.

The stock has made parabolic gains, but based on logic, rationality, and sound judgment, it’s time for long-time investors to cash out at least a small portion of your paper gains.

Nvidia is a fantastic company with A+ growth, leadership, and profitability. However, it is not immune to the macro economy, slowing demand, or a change in momentum/sentiment, which will inevitably happen.

As share prices rise, predictably, people with full-blown FOMO are joining the bandwagon late to the party. During this AI fever, consideration for valuation and rationality is put on the back burner as “dumb money” enters the market.

The people buying Nvidia stock now are momentum traders or dumb retail money. They admittedly have no idea what they are doing and are paying a premium for a very aggressive future outlook.

When I refer to ‘dumb money, ‘I’m not implying that these investors are unintelligent. It’s a term used to describe those who enter the market without a clear understanding of the investment they’re making, much like a dog chasing a car.

Here is a question from Linda in Illinois on a recent episode of Mad Money with Jim Cramer:

“I’m a retired postal employee who worked for 45 years. I have no financial investment knowledge. I wanted to know how to buy stocks, and I wanted to ask you if I should try to invest my Thrift Savings Plan (TSP) money in S&P Index Funds, or Magnificant 7, or Nvidia or all Nvidia.”

Think about the person in your family or at work who exhibits terrible financial acumen. The last person in the world you would want to take financial advice from.

The people considering buying Nvidia stock may have just learned about the company this year. They still may not even know what they do. If you’ve never heard of the company before last year, what happens if the stock craters? History shows people will justify their fears of a recession or market crash by selling at a deep discount and retreating into cash or gold.

This is perfectly normal animal behavior. But you are neither a dog nor a cat!

Again, Nvidia is a fantastic company—a best-in-breed company. But every company has a numerical valuation. With a straight face, can you say out loud that Nvidia will be a $10 trillion company by 2030? If you chase high growth, you typically pay a premium price for it and will likely underperform the market in the long run.

The risk-reward profile of buying Nvidia today significantly differs from a year ago. This may sound hard to believe, but shares are less valuable today because the valuation is far more uncertain than last year.

How many companies have gone from $3 trillion to $8-10 Trillion? Answer: None. Saying this happens with a level of certainty or confidence seems misplaced. It also ignores the risk of things going wrong. We are in uncharted waters with no precedent.

I’m actually coaching 8/9 year olds. Hoping to move up to middle school in the next 3-5 years.

Recently, the Lakers hired former player and current podcaster/ESPN analyst JJ Redick as their new head coach. Redick is the same age as LeBron James. He also has no coaching experience beyond youth basketball. Yes, you have read that correctly—a professional basketball team has hired a coach who has not even coached middle schoolers!

There is nothing wrong with being optimistic about Redick as a coach, but how can anyone be confident that he will succeed when he has never done it before? Of course, Redick could be the next Pat Riley or Phil Jackson; it could happen, just like Nvidia can continue skyrocketing. Valuation is an imprecise art because the future is unpredictable. But can you say with confidence this is probable or more possible?

Let me summarize my gameplan:

Am I saying to go all-in cash or to sell out of everything tomorrow?

No.

There is no need to think so dramatically or immaturely.

Betting against Nvidia is extremely risky.

Putting fresh money into Nvidia is risky because investing is more than just about data points and figures. Investing has far more intangibles, making it both an art and a science.

The safe time to buy Nvidia was the second half of 2022 when the US government banned them from selling chips to China and Russia.

I will ride Nvidia long-term, but the growth path is not guaranteed or linear. Past performance is no guarantee of future results.

Jennifer Lopez’s It’s My Party tour grossed $54.5 million with 31 shows in 2019. She recently canceled her tour. The same is true for the Black Keys, while other stars like Pink and Justin Timberlake (pre-DWI) have canceled some tour dates.

Meanwhile, Olivia Rodrigo’s “Guts” tour tickets go for above $570 on the resale market. In 2019, Rodrigo was a relatively unknown 15-year-old.

There is nuance and context to life and investing.

As a long-term investor in Nvidia, I am strategically preparing my portfolio by gradually increasing my cash holdings during periods of strength. This approach allows me to prepare for potential market downturns while benefiting from the company’s growth.

Nvidia is undoubtedly a great company, but why pay premium prices for future assumptions? I am building my cash position not out of fear but of a rational understanding that market fluctuations are normal. This way, I am prepared to take advantage of more appealing risk-reward profiles in the future.

It’s a win-win situation. Hold most of your holdings and reap the reward if the companies perform well. Trim your position in small incremental amounts to build cash. If bad things happen in the market, you at least have more cash to take advantage of a more appealing risk-reward profile in either a cheaper Nvidia stock or another company with a better runway for growth.

The law of big numbers says Nvidia will not hit $10 trillion by 2030. We have never seen a $3 Trillion company triple in 5 years. I am a contrarian, but even that sounds like a stretch. There are compelling companies that can go from $1-10 billion to $10-$100 billion, which is more plausible and we have witnessed several times.

There is nothing wrong with using nuance and rationality in investing. Take some money off the table, even just a tiny amount.

That’s how you, as an investor, need to think. Buy stocks when the valuation becomes desirable. To buy stocks when they are desirable, you need cash on hand, which is best built during days like today. What better time to raise money when your initial investment has increased 10x or more?

Preparing for the future by slowly building a cash position is sound investing advice because the market will eventually experience an inevitable downturn, and prices will fall. When risk falls, that would be a more appropriate time to pounce (use that animal instinct) and buy more aggressively.

Great investing requires a solid strategy and not just emulating pure emotional instinct. Don’t be the dog chasing a car.

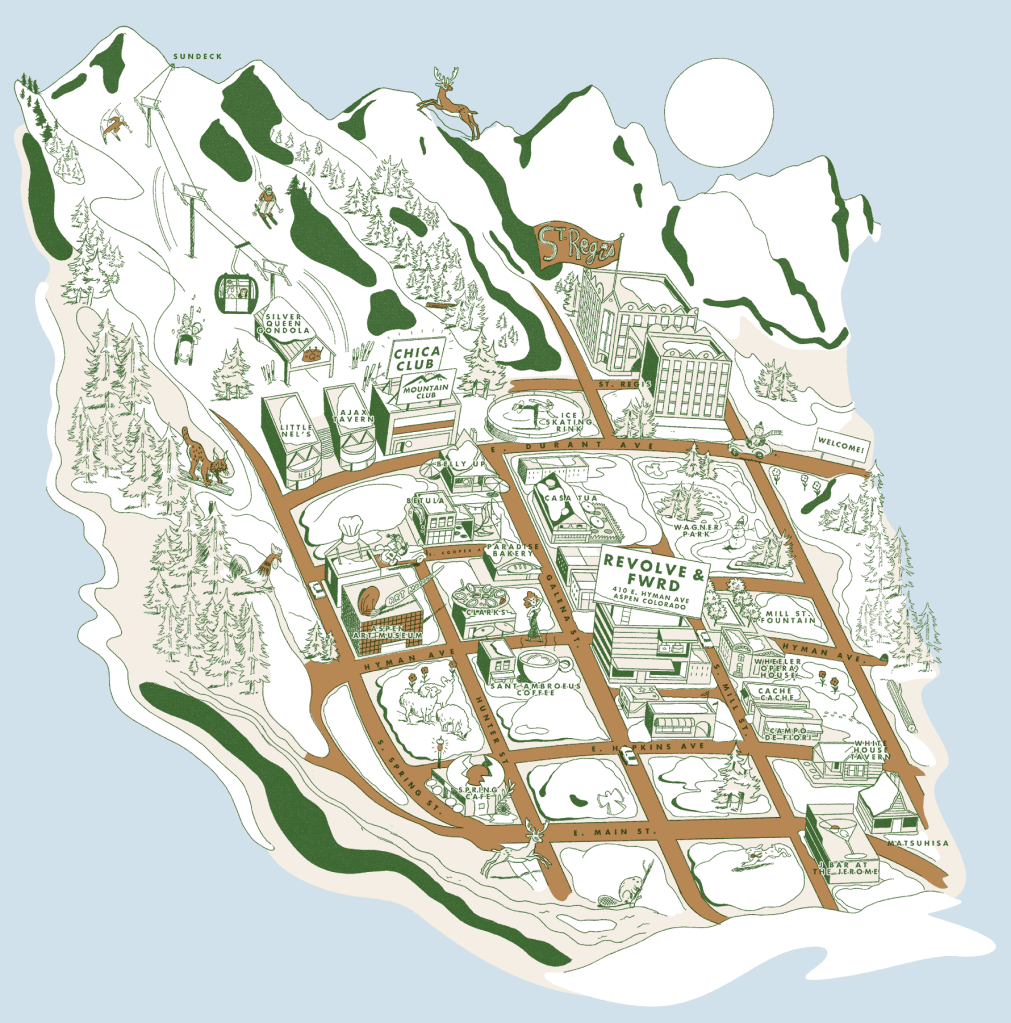

Revolve’s venture into brick-and-mortar retail with its first Aspen, Colorado store was not just a success, but a triumph. The initial pop-up store in December was a mere glimpse of the potential, and the decision to sign a multi-year lease was a resounding testament to Revolve’s ability to exceed its own expectations.

Why does this matter? Revolve, a digital-first business that has been diligently building its brand and e-commerce model, has made a strategic shift. Despite previous comments from earnings calls suggesting no serious plans for retail, Revolve has now embraced the potential of the physical retail space.

But the results were too good to ignore. It wasn’t so much that they sought retail, but demand called, and Revolve answered the call.

Aspen is just the beginning. With a robust digital marketing apparatus already in place, and the success of its first brick-and-mortar store, Revolve is poised for further expansion. This is a pivotal moment for Revolve, as it can now potentially translate its digital brand into a network of physical stores, paving the way for future growth.

This has the potential to increase an already impressive high average order value from the benefits of in-person shopping: impulse buyers from being able to feel and touch the merchandise. The Aspen store has also been a source of bringing in new customers, which is Revolve’s advantage and opportunity.

Advantage: Revolve’s customer base is mostly Millennial and Gen Z females. Roughly 60-70% of Macy’s and Nordstrom’s customers are Gen X and Boomers. I am not optimistic about legacy department stores. They have a problematic long-term business outlook. Macy’s is investing heavily in Bloomingdale’s and Bluemercury, but their brand name has declined significantly in the past decade. Nordstrom is doing a better job attracting young customers due to its off-price retail chain, Nordstrom Rack, but focusing on deals and discounts is a race to the bottom, and they will likely lose to Amazon, Walmart, and Target. I never understood Nordstrom’s business model because the off-price division does not complement the flagship stores. A “luxury” brand shouldn’t target consumers on a budget and vice versa.

Opportunity: Macy and Nordstrom need help mightily attracting Gen Z customers. It’s dire. Both companies will likely not show any year-over-year sales growth. Macy and Norstrom will eventually go private and leave the public market soon. It’s not a matter of if but when. These businesses may be able to restructure by going private, but it will likely take a very long time. Going private would also make raising capital difficult and cause a potential departure from key employees. Once the move happens, the capital and employees will likely shift towards a company like Revolve.

Is the Aspen store a signal for immediate retail expansion? I hope not. The focus should remain on building the digital platform and live events—Coachella, The Super Bowl, Cannes, etc. Physical retail should only complement the existing business unless the data overwhelmingly suggests otherwise. Much work is needed to build the brand through product/category expansion and international growth, which is more cost-effective through social media and pop-up events.

It would be premature for Revolve to make an aggressive retail push like Aritizia (3-5 new stores annually by FY27). They also don’t need it. Revolve has a much bigger online presence than other digitally native brands like Figs, Warby Parker, or Allbirds.

As a shareholder, I advise Revolve management to focus on curation rather than expansion. Identify 3-5 unique locations to create a highly personal and immersive experience. The stores should be bright and feature natural wood fixtures, making them engaging places to shop. Aspen works because it is an affluent city that blends luxury, charm, and scenic beauty. However, a store like Aspen is not scalable to a nationwide rollout. The ambiance is more subtle than in bigger cities like Las Vegas or Miami. It offers lesser-known brands in the high-end category to stand out more to a wealthy clientele.

I have identified some markets for Revolve to explore that can create a potential Aspen effect:

Park City, Utah Nantucket, Massachusetts Jackson Hole, Wyoming Charleston, South Carolina Carmel-by-the-Sea, California Key West, Florida Santa Fe, New Mexico

Entering smaller but highly profitable markets is a strategic move that makes perfect sense. Revolve, armed with ample marketing data, is poised to make prudent decisions and identify a few Aspen-like markets. The goal is to create a small footprint of high-ROI stores that offer a curated collection of luxury fashion brands—a blend of art, immersion, and boutique feel. The key is a luxurious bespoke experience, catering to the target audience’s preference for experiences over value or deal-hunting.

There is still plenty of room to grow. Despite a challenging macroeconomic picture for luxury retail, I haven’t sold any shares. I am confident in the business’s fundamentals and see a long-term pathway for growth and overperformance.

Why Tesla Shareholders should emphatically vote to approve Musk’s $56 Billion pay package

Musk’s compensation isn’t just about dollars; it’s about shaping Tesla’s destiny and soul. As shareholders, we are not just passive observers but active participants in this journey. Our votes on his pay package are a direct reflection of our belief in his vision and our commitment to Tesla’s future.

Under Musk’s guidance, Tesla’s stock price has skyrocketed, defying recent market turbulence. This dramatic rise starkly contrasts the stock’s value in 2018, which was a mere $21. Long-term shareholders have reaped substantial financial gains from this growth, a clear testament to Musk’s undeniable influence. This is not a personal viewpoint but an impartial, nonpartisan, indisputable reality.

Musk’s strategic decision-making has been a driving force behind Tesla’s success. Against all odds, he has led the charge in electric vehicle and clean energy innovation, reshaping entire industries. His ongoing leadership is not just important; it’s crucial for maintaining Tesla’s competitive edge and ensuring a prosperous future for the company. The potential loss of his leadership should inspire every shareholder to vote in favor of his compensation package.

Tesla’s long-term vision hinges on visionary guidance. Voting on compensation reflects shareholders’ trust in Musk’s ability to steer the company toward its goals. Elon’s compensation package is entirely contingent on achieving ambitious targets. If Tesla fails to meet specific triggers, Musk receives no compensation. This ensures that his pay is directly linked to the company’s success, aligning his interests with the shareholders. This alignment of interests should foster trust and confidence in every shareholder.

Tesla shareholders should ask themselves why they invested in the company in the first place. How many cars they sell this quarter or next quarter is less important than how they are positioning themselves for a Robotaxi world. This is an AI and Robotics company. Shareholders who dislike Musk or want to invest in a typical car company that achieves predictable quarterly numbers can choose from a bevy of other publicly traded companies.

Actual long-term Tesla shareholders don’t see Tesla as a car company; they see it as a venture with a start-up mindset into sustainable energy, AI, and software development. At heart, the vision is greater than just manufacturing vehicles. There is a clear line in the sand. Do you want Tesla to attempt to achieve moonshot or be a mediocre car company run by a Wall Street figurehead chasing predictable quarterly numbers?

If you vote no, you clearly communicate that you do not want Elon running Tesla. It’s a big middle finger to spite someone when the sentiment and stock price are low. Accelerate the transition to sustainable energy, revolutionize transportation, and produce humanoid robots at scale vs. grabbing low-hanging fruit and achieving goals with lower-moderate upside?

The rhetoric being spewed by pundits is biased, carrying a political agenda. Elon Musk’s loudest and most vocal critics are likely not Tesla shareholders, meaning they have no skin in the game. Think about it. Why would you “invest” in a company with a CEO you find deplorable? Does that make sense?

A story about business and technology has been hijacked by partisan fundamentalists. This rabid audience is tribal and less open to listening to opposing views. Elon Musk has been tagged as a villain that commentators will continue to deride. They have used the recent downturn in the stock as ammunition to defend their ideology.

Attacking Elon Musk has become a proxy for attacking President Trump. It’s that simple. These pundits are not your friends and are far from advocates of unbiased investment advice. Tesla stock could 100x and produce more than 200 million all-electric cars in a year; Elon Musk is still a con man to them, and the company is still a bad investment. Facts, data, and performance don’t change a fundamentalist’s opinion. It also won’t get them to admit they are wrong. The goal is to see Elon and Tesla fail spectacularly. Ask yourself if their interests align with yours as a shareholder.

I have voted yes because Elon’s pay compensation is necessary and mission-critical to Tesla’s future growth. Not voting for this package could potentially have catastrophic consequences. Losing his leadership would be a setback for Tesla and the future of our society as a whole. Musk is a man on a mission, and we as a society are in debt for his projects, which are critical to improving humanity through Tesla, SpaceX, Neuralink, The Boring Company, X, and xAI.

Elon Musk has revolutionized the electric car industry and taken on unimaginable financial and reputational risks. His sacrifices and suffering paved the way for Tesla’s success, allowing shareholders to thrive. This pay package is a testament to his past performance and a powerful incentive for future success. I voted yes because it keeps the trailblazer in place and re-positions Tesla into propelled growth for the next decade.