Randominvestorhttps://investinmyselfcom.wordpress.comThis is my personal blog about finances, the stock market, and investments. Disclaimer: I am not a financial advisor. Take anything I say for entertainment purposes only.

Neither political party is better for the stock market. Neither party cares about your portfolio returns.

Tesla and Elon Musk are imploding. It feels like the company is headed toward an existential crisis or bankruptcy.

Investors must understand that investing isn’t a game of certainties or possibilities. It’s a game of probabilities. Many people do not invest because of the potential of stocks going to zero, even though the likelihood of that happening is highly unlikely.

Business goes through cycles. Although most stocks are down in 2022, energy, healthcare, and defense are areas that have done quite well.

Look at the stock of companies like United Health, Bristol Meyers, Gilead, Chevron, and many others in these industries. All are doing quite well. These are the stocks “experts” are saying you are supposed to be buying now, not selling. If you went back 3-4 years ago, these names were loathed, and now they are beloved. This is how cycles work. They turn. If you assume tech stocks will always be uninvestable, you may need to look at investing through a probabilities lens. Are companies like Meta, Tesla, and Netflix going bankrupt? Again, look at it through possibilities rather than probabilities.

One of the greatest investors people have never heard of was Shelby Davis. Davis was a long-term investor who started investing at age 38. From 1947 until he died in 1994, he turned $50,000 into $900 million.

Shelby preaches many of the same principles that Warren Buffett does in long-term investing:

The biggest history lesson you can learn is that the market cycles from bust to boom and back again. Investor behavior flows with it. Each time is slightly different but similarities abound and the cycle always rolls on,” he said.

“Between these two extremes, and what investors forget, is a great long-term track record at compounding money that no other asset class offers. The few times in history when there is an exception, investors rarely seized the opportunity because they projected their short-term pessimism far into the future,” he said.

Shelby Davis and Warren Buffett are legendary investors, but their gains are attainable even for everyday investors. When someone tells you it is nearly impossible to beat the market by picking stocks, it is an arbitrary statement that can make investors take inappropriate actions. Saying investing in single stocks is an impossible game to win is like saying sticking to a diet is impossible because most people fail at it.

These are some of my thoughts, and I could be completely wrong. Some of the views I am expressing cannot be proven quantitatively, but if I had to bet money, I am more right than wrong. I have always preached investing is more behavioral and philosophical than numerical.

Take a room of 10,000 random investors. 2/3 of those investors, or at least 6,666, will fail to beat the market not because they are uninformed or bad stock pickers but from self-inflicted wounds.

Investing money you can’t afford to lose. You can categorize these investors into two groups. People who shouldn’t be investing either live paycheck to paycheck or have no emergency fund. The other group is people that are invested but will likely need to dip into their portfolio in the near to mid future – to buy a house or fund retirement, for example. These people are not in a dire financial situation but will likely have to sell out of positions for non-investing reasons because they do not have enough discretionary income.

Lack of emotional control or patience. Suppose you have a strong conviction to buy a stock but a few months later sell out because the stock has fallen or everyone in the media is saying to sell. In that case, you most likely shouldn’t be investing. Humans aren’t hard-wired to be good investors. Humans hate losses twice as much as they like gains. A 50% loss feels as bad as a 125% gain feels good. This is one of the reasons why many investors never see exponential gains. They don’t have the stomach to wait for it. For many people, once they see 30-40% losses, they just sell and leave the market altogether.

The 6,666 investors will have one or two of these problems, like having one hand tied behind your back. This provides a significant advantage to investors that can follow basic long-term investing principles. Not an arbitrary rules-based methodology but an ability to think independently, be patient, and learn.

If you can invest money you can afford to lose and have balls of steel, you will likely be in the 70th percentile of investors. Notice I didn’t mention anything about a person’s ability to analyze/value stocks because this is a subjective practice that can be learned over time.

You will get little debate from anyone about not using your rent money on stocks. You will get a lively discussion on whether stock x is overvalued or undervalued. As you gain experience, if you are adequate at analyzing equities and can think independently, you can likely be in the 80th percentile or higher of top investors.

If you are in the 70th percentile of investors, you have beaten the market rather easily. How likely is this? Not that improbable.

If you are having trouble following, I will provide an example:

A 1200 SAT score can be considered good or bad, depending on one’s expectations. A 1200 SAT score puts you at the 74th percentile, which from one perspective, sounds great – you scored higher than 74% of your peers! On the other hand, a 1200 SAT score will not get you into Harvard or Yale.

So, when people say you aren’t likely to beat the market, it depends on the individual investor. The entry of barrier to investing is low. Are you an investing hobbyist, or do you view your portfolio like a business? The average Robinhood user is 31 years old with an account balance of $240. That is not enough skin in the game.

A large number of investing hobbyists skews the number of people that fail to beat the market at a higher percentage than it should. More than 2/3 of investors fail to beat the market, which is a conservative guestimate given how many Americans live paycheck to paycheck or do not have the proper investment mindset.

The majority of people that fail to beat the market are breaking simple investing rules. Think again about the high percentage of people who break their diet. Does that automatically mean you shouldn’t diet because most people fail or abandon their diet? Again, you have to individualize the experience.

Investors shouldn’t give up investing and automatically go into index funds. Tesla is a perfect example. A tremendous long-term stock going through short-term negative sentiment.

Returning to investors being able to control their emotions, this includes not being blinded by arrogance or ideology.

“Worldly wisdom teaches us that it is better for reputation to fail conventionally than to succeed unconventionally.” John Maynard Keynes.

Framing forward-looking expectations through an ideological prism is a terrible idea for investing. Getting investing advice from political commentators about Tesla stock is foolhardy. Partisan politics, by nature, is tribalistic, negative, and biased. Tesla sells electric vehicles for over $50,000. Most consumers on the fence about buying a Tesla base their decision-making on non-political reasons.

Potential Tesla buyers don’t care what Elon Musk thinks about Dr. Anthony Fauci or his tweets about Democrats. That is not how consumer behavior works. That is not how consumers think. Those that do most likely make up a fringe minority or weren’t that interested in buying a Tesla in the first place. Imagine buying a house: how much does a potential home buyer weigh the seller’s political affiliation or social media activity before making an offer.

The great Telsa story has been hijacked by politics. Political commentators and politicians do not care or understand the company’s financials. The declining stock price drives whatever narrative is spun by the media and curmudgeons on Twitter.

Investing and politics should not mix. You may disagree, but a CEO’s political affiliation is meaningless. Tesla is a fantastic company producing phenomenal growth results. I have seen this play out before:

“Tesla is doomed.”

“Elon Musk is unstable.”

“Tesla is a car company, not a technology company.”

“Tesla has no competitive advantage.”

I think I’ve seen this film before

And I did like the ending.

Where Tesla bears don’t admit they were wrong, they just say I got lucky.

The stock may enter a bust cycle, but this creates an opportunity. As Davis said, “out of crisis comes opportunity… A down market lets you buy more shares in great companies at favorable prices. If you know what you’re doing, you’ll make most of your money from these periods. You just won’t realize it until much later.” Unfortunately, many investors will fall into the same trap of selling stocks during a bust cycle and buying during a boom cycle.

The Tesla fundamental story is solid. The growth numbers are impressive. The future is incredibly bright. The Tesla Bears have already been defeated. Refuting decade-old talking points is a waste of time.

Politics is mainly theatre. It is entertaining to watch, but it typically has no material impact on a company’s earnings, profits, or shareholder value. Trying to turn political commentary into investment tips is dangerous in investing. Politics has a definite space for society, but how do political programs on CNN, MSNBC, and Fox put money in your pocket? In investing, it doesn’t. I view these shows on the same level as watching pro wrestling, or comedy shows, purely for entertainment.

Having insurance is one of the best ways to preserve your wealth. Another way to say this is that insurance protects your downside risk and makes it less likely for you to go into financial ruin.

Did you know that medical bills cause over 62% of all bankruptcies? Health insurance isn’t a cure-all solution since it doesn’t cover all medical expenses. Still, it would be reckless today to voluntarily opt out of health insurance.

Being young and healthy is not a smart reason to opt-out of insurance. The risk of paying the total cost of a health emergency is the equivalent of being trapped in a building with a bomb in it. The explosion will hurt you.

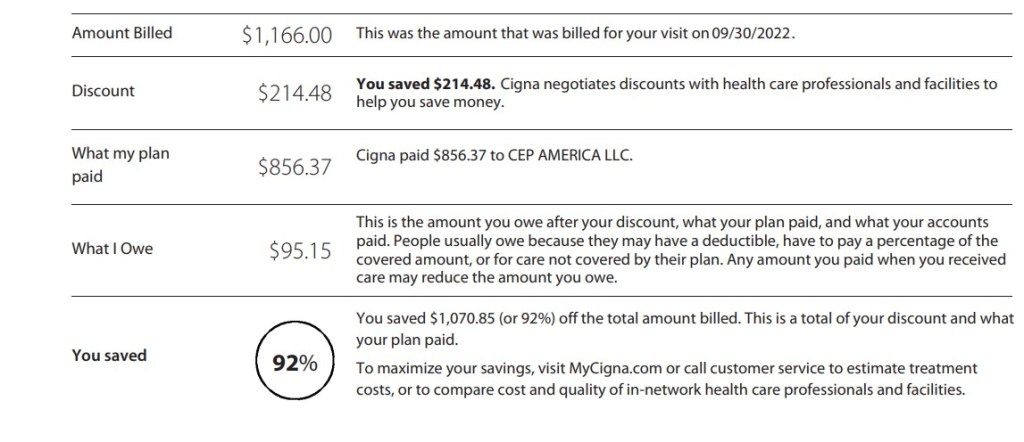

A few months ago, I had chest pains, which could have been a precursor for a heart attack. Luckily, I went to the emergency room, and all my tests returned back as normal. I never found out why I suffered chest pains, but I was still billed $5,716 for a few tests. Insane right? No treatment or diagnosis, just a few bills to find out I didn’t have a heart attack.

Put yourself in my shoes. I am relatively healthy, with no serious medical history or preexisting conditions. Do you avoid a trip to the ER and hope the pain goes away but risk suffering from a heart attack in your home?

One of four medical bills I received for getting tests done. Luckily my insurance covered the majority of this bill.

I was lucky and considered myself fortunate to have insurance. Is it worth saving $100-200 monthly in premiums but risking paying medical expenses at full cost? No investment or opportunity is worth the uninsured risk. Multiple medical bills can create an avalanche effect, wipe out your net worth, or bury you in debt. Remember, unpaid medical debt doesn’t go away or expire.

Get Health Insurance! Being uninsured is not worth the risk!

The amount you would save in a decade by not paying premiums ($200 monthly) with no health insurance: $24,000

The average cost of a hospital stay for one day is $2,873

Main takeaway: Many Americans are doing okay financially but are entirely unprepared to absorb a major financial shock. A cataclysmic health crisis, even a mini one, can crumble your net worth. Staying at a hospital for over a month without insurance will cost you easily over six figures.

I agree that health insurance in the United States is broken and unfair however people have to best navigate through this rigged system with intelligent financial decisions. Just complaining about the system and hoping the government will fix it isn’t a viable solution. Health insurance is one (but not the only) way of not becoming another American healthcare system victim.

If getting good health insurance requires working a part-time or full-time job you hate, so be it. Educate yourself and take prudent steps before soliciting donations on GoFundMe becomes your only option. Ignoring the issue isn’t going to resolve the issue. Crying foul on how rigged the system isn’t a viable solution either; take steps to protect yourself.

Another valuable insurance is renters or home insurance. Many landlords and banks require insurance, but it isn’t required by law like car insurance. Ironically about the same percentage of people who file for bankruptcy from medical bills is about the same percentage of renters that do not have renters insurance.

Many think paying $10-15 a month in renters insurance is a waste of money, even at that low cost. I used to think this way until I was recently robbed.

The robbers took nearly all of my belongings. Luckily I was not injured or required any medical attention. My insurance through Lemonade reimbursed me for my phone, laptop, and glasses. Getting those funds wired from Lemonade provided a great sigh of relief. They made me realize how paying for renters insurance was worth every penny.

Please consider getting renters, pets, car, home, or life insurance through Lemonade here. My experience with the claims agent, Jose, was pleasant, and the process was smooth. Once I provided a copy of the police report, Lemonade immediately wired the funds to my bank account. I couldn’t have received better service from any other insurance company, and I am thankful for being a policyholder through Lemaonde.

Think of insurance as a safeguard for yourself. You do not typically profit from insurance, but it keeps you whole or restores what you lost. I write a lot about how investing can create financial freedom, but with wealth building, you need to start with a strong base or foundation. Insurance is necessary to protect that foundation and can prevent it from collapsing. Investing can create wealth, but insurance can protect it. Insurance will act as a safety net even if you have a small net worth. If you voluntarily opt out of insurance or are thinking about it. I strongly advise you to reconsider. In risk management, not having insurance is one of the riskier decisions you can make.

Taylor Swift performs in Houston in 2017. Photographer: Frazer Harrison/Getty Images North America

Taylor Swift fans, or “Swifties,” will spend ridiculous money on seeing her perform live. For many fanatics, the motto is “I’ll spend the money now and worry about paying it off later.”

Spending $3,000 or even more for a Taylor Swift ticket is ridiculous. Looking at it from a surface level, even if you are affluent, spending this money on a concert is a bit irrational.

I will not judge Swifties or fans of Beyoncé, Lady Gaga, etc., for spending this kind of money because experiences have a different price tag for everyone. For one person, the experience can be transformative; for another, it’s $1,000 an hour to watch someone sing live. These stars have built large, dedicated communities, and fans will spend; this is nothing new in fandom or consumer behavior.

The problem with Taylor Swift as an artist is that she isn’t generational. She is a product of Wall Street. A talented songwriter/musician who understood the business aspect of the music industry and cashed in. Taylor Swift’s father is Scott Kingsley Swift, a financial advisor at Merrill Lynch. Her mother was a mutual fund marketing executive. Her career is managed like a wealth portfolio, and it shows.

I am not questioning Taylor’s talents or abilities. The problem with Taylor is that she didn’t break down any barriers or transform the music industry. America loves artists saved by the music industry or musicians who went from rags to riches. Tayor was born into a well-off family that provided her the resources and connections to become the star she is.

My theory is that the most influential artists are highly flawed individuals. These “broken” musicians can manifest their struggles and life experience into their music. The music produced can be volatile, raw, and out-of-the-box, ultimately redefining music genres and reshaping the industry.

Many of the most influential musicians suffered from abusive parents, alcoholism, drug abuse, violence, trauma, or something tragic that happened to them. Mixing that in with Hollywood and paparazzi can create an explosive solution that garners a lot of eyeballs. None of the above fits Taylor. Her story is kind of uninteresting. Imagine a millionaire who already manages their money well, winning the lottery.

Taylor is a highly talented artist who manifests a whimsical/cookie-cutter view of capitalism. With her music, I don’t feel a real sense of struggle, passion, or purpose. The most passion she has shown was fighting for her music catalog rights, which was more about profits than the actual music.

There are better role models for musicians than Taylor Swift. As an entrepreneur, yes, but as an artist, no. Taylor’s music is highly curated and manufactured. More about ROI and profit margins than taking risks and breaking barriers. More about image control than raw vulnerability. Around the world, you can find thousands of talented undiscovered artists playing at smaller intimate venues and watch them perform live at a fraction of the price of an Era Tour Ticket.

Unfortunately, we see a lot of Taylor Swift clones emerging in the industry with younger artists like Olivia Rodrigo, who are drawing inspiration from the more commercialized version of Taylor. Do people remember when she was a country singer?

Gustavo Coutinho, who’s never seen Swift perform live, came up with a $2,000 budget after 10 months of savings. The 25-year-old consultant in Boston ended up spending about $1,500 to attend two concerts. “I would pay $3,000 if I had to.”

Truly, generational artists take risks, even dangerous ones, and the audience decides whether that risk is worth taking. Taylor’s career arc has been a consistent slope towards playing it safe and mediocrity. That is a slam on her as an artist, not an entrepreneur. Unlike a lot of musicians, she thinks like an executive. She’s more Sheryl Sandberg than Amy Winehouse.

In the future, I would expect her to launch her own record label and become a billionaire. In 10 years, her empire will be worth more than Ye, Rihanna, and even Jay-Z/Beyoncé. Taylor has the Millennials and Gen Z demographic locked down pat, who will continue to pay their hard-earned savings to watch her perform live.

I am not knocking Swifties. However, they should evaluate the actual reason for their worship of Taylor. Rooting for Taylor is the equivalent of rooting for TicketMaster, Alabama Crimson Tide, Facebook, or Amazon. She doesn’t look at her fans as fans but as lifetime customers who pay, in essence, an annual subscription for her merchandise and events. To Swifties, she may seem down-to-earth, but in reality, she is an opportunistic savvy business genius.

“If you are working on something that you really care about, you don’t have to be pushed. The vision pulls you.”

Steve Jobs

Many of the best companies are born during tough times. It feels like we are in a macroeconomic depression.

For Lemonade investors, you have to be comfortable being uncomfortable. Currently unprofitable and not forecast to become profitable over the next three years.

That is not new.

The stock will suffer because there isn’t a short-time pathway toward profitability. In a market like today, unprofitable companies get punished, especially with the ongoing inflationary pressure.

I’m highly confident that at some point in the future — it might be six months or three years — we’re going to look back at some point over the next few months, and we’ll say, ‘that was a phenomenal time to buy Lemonade.’

Every investment opportunity has risks. You have to assess if the risk is worth the reward. Sometimes the risks are either exaggerated or hidden. Some companies can overcome risk, while others can’t. An investment in Lemonade is worthwhile for the potential reward. I could see this being the start of something big.

The good news:

The story is simple. Lemonade will either realize the economies of scale or not. To achieve this, they must continue to grow. The good news is customer growth is scaling nicely.

Where Lemonade shines brightest: Gateway policies

Lemonade is among the leaders among all insurance companies in acquiring first-time buyers of renters insurance, especially if they are under 35 years old. The growth in pet insurance is also impressive.

The growth rate for these gateway policies is very positive, but renters and pet insurance are just appetizers for Lemonade’s growth. These businesses are niche, and customer churn is high.

Renters and pet insurance have to be looked at the same as the rice and asparagus of insurance policies. Nobody eats rice or asparagus by itself, but when eaten with steak, chicken, or mac and cheese, it creates a perfect synergy. Lemonade renters and pet insurance policyholders will bundle more policies together as they become available. If they need term insurance, it is available. Lemonade has a 300k waitlist for Lemonade car without advertising. Most of those on that waitlist are in the Lemonade ecosystem.

Customer growth has been consistent and steady. I expect that to continue as they enter more markets. When Lemonade grows with more 2-4-product policyholders, you will see the flywheel spin.

Evolution of a policyholder at lemonade:

$60 a year: Renters Insurance $600 a year: Renters, Car, Pet Insurance $6,000 a year: Home, Car, Pet, Term

The bad news:

I fully expect loss ratios to fluctuate in the short term. Lemonade is an insurance company that isn’t profitable. Not what you want to hear, but they are a newer company. I don’t hold it against them, just as I don’t hold it against SoFi or Block for being unprofitable banks. It is about the future forecast.

That being said, any catastrophic natural disaster like Hurricane Ian will have a more crippling effect on Lemonade’s balance sheet than a more stable insurance company. A rise in claims will hurt any insurance company’s bottom-line results, but for Lemonade, the cut will be felt deeper since they are still trying to diversify their business book.

Lemonade home and car are low frequency-high severity products. When paying out claims for home and car, the payouts can be crippling. It creates a double-edged sword. The juicy TAM and profits are in car and home insurance, but so are the expenses and payouts.

The question remaining:

How to determine if Lemonade will be a big-time winner: If their technology – LTV models, leveraging AI and machine learning can lead in the long run to better underwriting results.

A natural event like Hurricane Ian can push insurance companies to the brink of bankruptcy. How Lemonade navigates through this in the future will determine if they succeed.

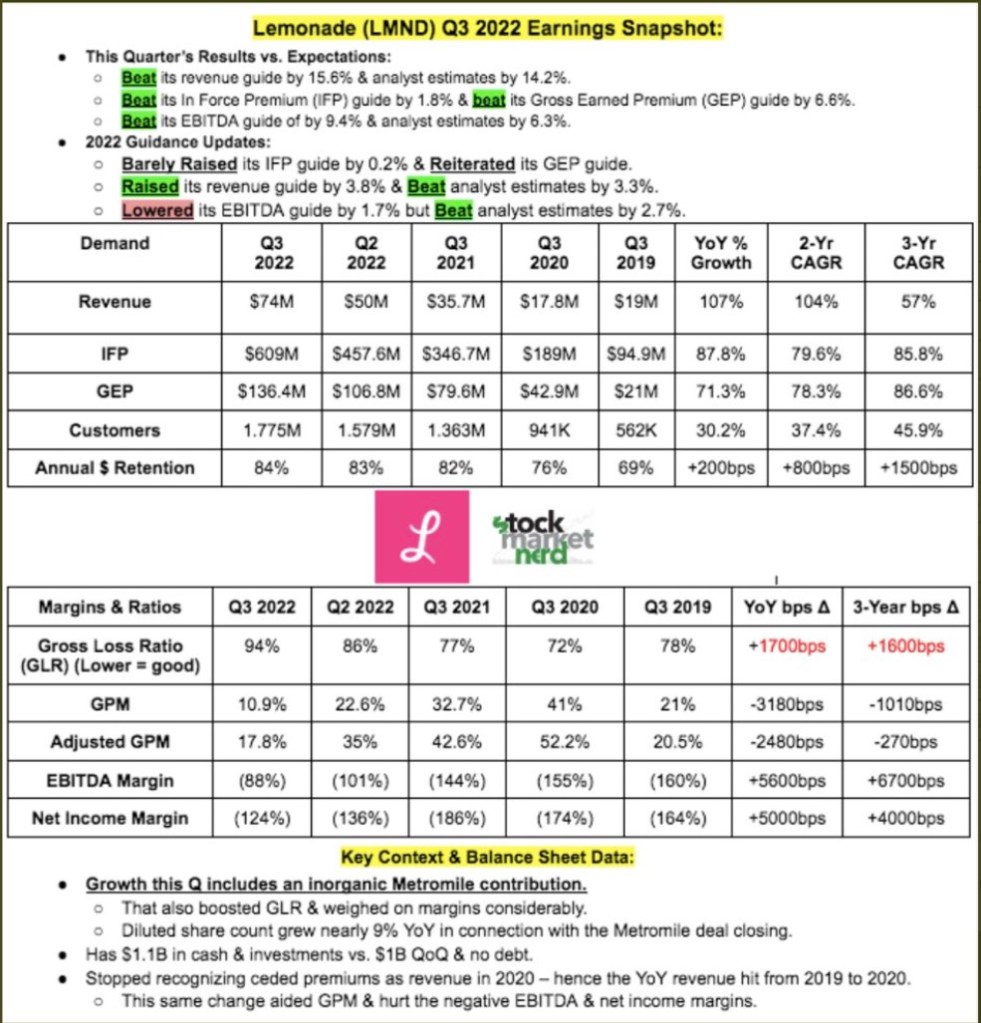

From Q3: Total Customers: 1,775,824. Premium per customer: $343. As the customer count grows and more products become available, the premium per customer should steadily increase. As this happens, the LTV Models and AI provide better predictive data, leading to better underwriting. The result is providing more desirable customers with less expensive premium costs and riskier customers with more expensive premium costs.

That is it. Lemonade’s stock will likely go sideways in short to medium term. It may even go down significantly. It might take several quarters for Lemonade to hit its stride fully, but the groundwork now will be unlocked and prove significant in time.

Expenses may continue to grow, but if Lemonade can gain exponential customer growth, that will be the key to unlocking a network effect. If Lemonade gets a network effect, revenue growth will far exceed expenses.

I could never see myself selling Lemonade stock anytime soon because the potential reward is so big. The company could 10x, twice, and still have a small share of the overall insurance market.

Lantern Consciousness and First Principles Thinking

Many investors are looking at Lemonade as a big loser, which is fine. The stock is not for everyone. I would argue that narrowly focusing on just a few key metrics can create blind spots and tunnel vision in investing.

Consider the difference between spotlight and lantern consciousness. Spotlight consciousness illuminates a single focal point of attention. This is how most adults think. Lantern consciousness illuminates a broader point of attention. This is how most children think.

Spotlight consciousness is fantastic. Drugs like caffeine and certain medications enhance it better. The problem with spotlight consciousness is that it may not be helpful for long-term investors.

Projecting a company’s stock price in 5-10 years is silly, focusing on the balance sheet or discounted cash flow model. Lantern consciousness in investing can provide an advantage because it doesn’t lead toward a predictable tract. Financial measures and formulas don’t help see where a stock will go long-term, as too many variables can change. Figures can be interpreted differently based on preconceived notions and biases. If a few prominent analysts make a prediction, it shapes everyone else’s perception, leading to a herd mentality. Humans generally want a feeling of belonging, so popular opinions often become the “right” opinion.

What is needed is a more philosophical viewpoint or first principles thinking. This is why investing is hard. Humans desire to belong, and investing requires you to go against the popular decision. When utilizing lantern consciousness and first principles thinking, it allows you to peel the onion and gain a more introspective viewpoint:

In layman’s terms, first principles thinking is basically the practice of actively questioning every assumption you think you ‘know’ about a given problem or scenario — and then creating new knowledge and solutions from scratch. Almost like a newborn baby.

On the flip side, reasoning by analogy is building knowledge and solving problems based on prior assumptions, beliefs and widely held ‘best practices’ approved by majority of people.

People who reason by analogy tend to make bad decisions, even if they’re smart.

Elon Musks’ “3-Step” First Principles Thinking: How to Think and Solve Difficult Problems Like a Genius

Lemonade can be a big winner because they have a culture and model wholly divorced from how legacy insurers operate. Could they fail? Obviously, but what if they succeed? Something improbable is improbable until it isn’t. The insurance market is incredibly inefficient and outdated. A lot of it needs to make more sense to the consumer. Why do male drivers pay higher insurance than female drivers? Simple because of their gender? Why do older drivers pay less than younger drivers? Simply because of their age?

Calculating premiums based on how groups of people within a demographic behave is outdated and unfair. Lemonade addresses many of these inefficiencies because they utilize technology to create a more efficient business model, and if they succeed, the stock has no real ceiling. Again, they can go bankrupt, but from where they were in 2015 to now, the company has made meaningful progress and is still in the early innings of growth.

“The world only exists in your eyes… You can make it as big or as small as you want.”

F. Scott Fitzgerald.

The majority of my crypto holdings are gone. My assets are frozen in the custodial custody of BlockFi, who halted all withdrawals on their platform this past Thursday. I will give you my raw thoughts on the situation, what I learned, and what I plan on doing in the future.

Warren Buffett was right:

“To invest successfully does not require a stratospheric IQ, unusual business insights, or inside information. What’s needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding the framework.”

Sam Bankman-Fried is a pretty smart guy, maybe even a genius. He is one of the smartest people in the world, based on IQ. Unfortunately, he and his inner circle only had a little experience running a crypto empire.

SBF fooled everyone. He misled his sponsors, institutional investors, retail investors, the media, news outlets, and even members of congress to build a $32 billion crypto kingdom. SBF could go down as one of the greatest fraudsters of all-time, even worse than Bernie Madoff and Elizabeth Holmes.

Blame the exchanges and not crypto

I am hearing through Twitter and Reddit that many people will stop investing in crypto altogether. We have to remember the exchange represents the custodian or gatekeeper of your assets. The assets, such as Bitcoin and Ethereum, have value. The exchanges failing, like FTX, Voyager Digital, Celsius Network, and others, were caused by a mix of bad actors, incompetent management, a lack of financial regulation, and a broader downturn in financial markets.

In short, crypto and crypto exchanges are not the same thing.

As a matter of principle, we fundamentally believe in protecting client funds. Not only because it’s absolutely the right thing to do, but this also benefits the ongoing health and adoption of crypto financial services worldwide.

You may ask why I kept my money in BlockFi instead of a hard wallet. Honestly, I do not have a good answer. I got complacent. Clients who put their money on exchanges are not investing in them. Just as if you are putting your money in a bank, you are not investing in the bank; you are using the bank as a custodian to safeguard your account.

Part of it was laziness on my end. Call it the ‘Boiling Frog’ syndrome. Another part of me believed in BlockFi CEO Zac Prince, who explained why Blockfi was a safer exchange compared to Celsius and Voyager. There was no exchange token, and the company acted like a legitimate financial holding company.

From my research and due diligence, putting my assets with BlockFi was a safe decision.

Despite the turmoil, Marquez and Prince thought they’d built a cyber-winter-proof organization. BlockFi is a centralized finance (CeFi) company, structured more like a bank, with an audit and risk committee that reports to the board. The committee was peopled with Wall Street types who had experienced the financial crisis of 2008. “We didn’t offer Luna to our U.S. clients,” says Marquez. “We didn’t have direct exposure to that market event.”

By trusting BlockFi, I was de facto trusting FTX since FTX agreed to buy BlockFi in the summer. I was duped and made the wrong decision, but I was not alone and made the best decision at the time.

From my interpretation, a group of entitled millennials from prominent wealthy families took advantage of a highly unregulated market. SBF and his inner circle were highly educated, understood a market better than most of everyone else, and used that to their advantage, running a Ponzi scheme. SBF is a likely sociopath with no moral compass; his squad wreaked financial havoc but was done in by his arrogance or greed, probably a mix of both.

FTX built a pyramid scheme of trust. You assume they are credible when you see big-name backers like Paradigm, SoftBank, and Sequoia Capital and partnerships with Tom Brady, Stephen Curry, and Major League Baseball. Tom Brady, for example, likely has his own paid team that researches the best partnerships and investments for him.

On a scale of 1-10, 1, having no trust and 10, having complete trust, when I signed up with BlockFi originally in 2021, my trust level was at 8. At the beginning of 2022, I enjoyed the platform and weekly emails from BlockFi. I would assess my level of trust in January at a 9.

During the summer, when FTX agreed to buy BlockFi, my confidence level fell to a 7, but I assumed the worst was over, and I was satisfied by Zac Prince and Flori Marquez’s responses in interviews and podcasts. They said all the right things and passed my BS test.

When FTX collapsed, my confidence had fallen to a 6, but BlockFi kept assuring me my money was safe all week! I was contemplating, even preparing to transfer my assets into Coinbase by Thursday afternoon, but by that evening, it was too late.

Do not blame the victim:

A lesson in emotional intelligence. Saying, “not your keys, not your crypto,” to someone that just had their funds frozen on FTX or BlockFi is a bit insensitive and cold. It would be like telling someone uninsured that got hit by a car “should have signed up for coverage.”

There is a time and place to talk about hard wallets and cold storage, but this isn’t it

Many advocates of “not your keys, not your crypto” still have a portion of their assets in exchanges like Crypto.com, Coinbase, and Kraken.

Exchanges falling will cause a niche market to get smaller as many crypto supporters will leave permanently.

The crypto ecosystem does not need more bank runs and exchanges to fall. This will depress the price of BTC further and longer. For selfish reasons, crypto holders should want their assets to increase in value, not decrease.

None of us have the benefit of hindsight. It is easy to play Monday morning quarterback after the events have unfolded.

The actual assets didn’t default; the exchanges did, and you had bad actors who committed crimes.

For the people who are saying crypto is a scam, remember that many clients of FTX and BlockFi did not buy speculative coins and weren’t even trading. A lot of us bought USDC or other stablecoins. Some of us were gaining interest from Crypto Asset Interest-bearing Accounts.

If you searched for the most secure and best crypto exchanges, FTX and BlockFi were on that list. I am a crypto novice, which is a leg up on the average person, but this industry is still very new and foreign. If the “experts,” who did their due diligence on evaluating how safe and secure an exchange was, got duped, what hope does an average investor have in making what should be a simple decision on where to store their assets safely?

I can live with a stock or asset falling 90% as an investor. I assume the risk. Unfortunately, many clients who lost money are not investors or have an investors mindset. They viewed these exchanges as pseudo-banks like Venmo or Cash App and may not be prepared to handle such a loss. We are victims of a likely crime and shouldn’t be labeled degenerate gamblers.

If you need help, dial or chat 988 for the Suicide and Crisis Lifeline. For the Crisis Text Line, text 741741. Help is available if you need it.

Tony Blair, Bill Clinton, and Sam Bankman-Fried on stage at the Crypto Bahamas conference.

What this means for crypto:

The amount of damage done to institutional/retail interest in crypto and the crypto ecosystem is immense. You can look at this as a “buy the dip” moment for BTC or ETH but what happened this past week is not good for the industry. It will likely take at least a few years, if not more, to recover.

I could see this as a possible great depression for crypto. Imagine waking up and hearing your bank is filing for Chapter 11 bankruptcy, and all your holdings are frozen. You contact the Federal Deposit Insurance Corporation, which says the bank owns your money according to the Terms of Service you agreed to. The good news is after the bankruptcy procedures; you might receive 10% of your original holdings.

That’s what the crypto community is going through. Unless there is quick regulation, I do not see any recovery in the price of BTC or ETH anytime soon. The price of BTC is more likely to fall below 10,000 and stay there for a while than shoot above 30,000.

The idea of having to own a hardware wallet in cold storage is something I will entertain, but I am not happy. Exchanges provide convenience and simplicity. If people cannot trust exchanges, it will destroy widespread adoption and erode trust in crypto. If we cannot trust the exchanges, many investors will have no confidence to hold.

Many people do not want to store a bunch of gold bricks in their homes or store their cash under their mattresses. The industry will take a big hit if hard wallets are the only way to store crypto securely.

I would like to see all crypto exchanges with something similar to FDIC or SIPC insurance protection in the future. Financial regulation is required for investors to stay invested.

These exchanges were less secure and solvent than regular banks. The influencers, media, credible blogs, and financial publications marketed and advertised these products like banks.

I take full responsibility for my actions; however, the DOJ or whoever will investigate this must prioritize providing restitution to the defrauded depositors first, much before the investors who assumed the risk to receive a potentially greater reward.

A highly credible source very close to the Sam/FTX situation on what was going on internally: pic.twitter.com/iGO3sbvRr0

Crypto represented about 5% of my net worth. Not a lot, but still painful.

Watching the price of BTC and ETH holdings fall 70% this year barely fazed me. The **** show that happened this past week rattled me. At this point, the trust is gone. I would be nervous if my crypto were under the custody of Coinbase, Binance, Gemini, or even a “real” bank like SoFi or Robinhood.

Most of my holdings are in stocks, and it has been a while since I bought sizeable amounts of crypto. Ultimately, the course remains the same. I view this similarly to an investment in a small-cap growth company that went south. I am mentally writing this off as a 100% loss. I am still pro-crypto, but I need to figure out where I stand with crypto exchanges now. I had no intentions of buying any crypto before this mess, and I do not see the contagion ending soon. I will reassess when the crypto market stabilizes, which may take years.

I made a mistake, and I will continue to make mistakes. I will learn and move on. The three worst traits for an investor are fear, arrogance, and complacency. It is easy to be fearful at this moment. I will continue investing but do more rigorous due diligence. I will still take a lot of risks. Proper dd is important but only sometimes possible. Investing in an index seems prudent, but can most investors even name 20 companies in the S&P 500? The QQQ has Pinduoduo as a holding. How can one do proper dd on a company based in China? I advise taking risks, especially if you have a long investing time horizon.

I am numb to the news and the duplicity of SBF. I wonder if Flori Marquez and Zac Prince were maliciously deceitful actors or pawns in SBF’s shell game. At best, they were poor stewards of my assets and lost my complete trust.

Could a white knight rescue BlockFi? CZ, Jack Dorsey, Brian Armstrong?

Possibly. PayPal is worth over $100 billion and is considered the mature adult of fintech. If they want to enter the crypto market at a floor-bottom price, this would be an excellent opportunity for pennies on the dollar.

PayPal would acquire many new users as there is a low overlap between Paypal and BlockFi users. Venmo, owned by PayPal, already offers crypto, so they are interested in the space and already have a team that can run BlockFi. If the SEC approves BlockFi Interest Accounts, the value of BlockFi could be 10x. Pure speculation and ramblings at this point, or just pure hopium.

BlockFi is filing for Chapter 11 bankruptcy. That is my educated guess, as the BlockFi credit card no longer works, and the “Meet The Team” page has gone dark on the main website.

I hope Prince keeps true to his words and protects BlockFi’s clients first. “As a matter of principle, we believe in protecting client funds,” Prince tweeted; doing so was both good business and promoted crypto financial services generally.

Make good on your word Zac and Flori and do everything in your power to return us whole again and help restore faith in your clients and the crypto community.

I wish everyone the best during this cold crypto winter. As a community, we can learn and grow with each other. We can flesh out the bad actors and achieve widespread crypto adoption. 2023 could be even bumpier. Stay hopeful and reach out if you need help. We will grieve but get through this ordeal much stronger.

Our customer satisfaction score in the third quarter was the highest level in at least 5 years, and we intend to continue to set the bar even higher.

Average order value, or AOV, was a very healthy $320, an increase of 16% year-over-year.

Our partner is entertainment studio Muus Collective, which is backed by Griffin Gaming Partners — one of the world’s largest investment venture funds exclusively focused on gaming.

With our technology-driven DNA, operational excellence, strong brands, and connection with the next-generation consumer, we believe we are well-positioned to capture market share.

My takeaway:

Revolve is focused on long-termism or long-term growth opportunities. As a long-term investor, this is what I want to hear. The company is financially profitable yet focused on growth initiatives that will bear fruit 5-10 years from now. It paints a bright future when you have improved customer satisfaction scores, high social media engagement, and a robust balance sheet.

The economy is challenged in the short term, but Revolve is positioned well in a recessionary environment due to its operational success.

Companies like Nordstrom and Macys, or old apparel retail, are not focused on brand connection or long-termism. They have to deal with hundreds of physical retail stores and over 60,000 employees. These companies deploy inefficient advertisement strategies and are not forecast for future growth. Revolve is thriving and slated to continue to grow. Macy’s offers a 3.22% dividend yield, and Nordstrom’s offers 3.97%. When a company offers a dividend of that size, its priorities are to manage what they have, not grow it.

Revolve’s partnership with Muus Collective is the key highlight of this earnings report.

The importance of Revolve entering Web3:

48% of gamers in the U.S are women. The demand is rising while the supply is low.

Male gamers tend to game because of boredom or competition. Female gamers differ in motivation, more for social reasons and to create relationships.

Female gamers prefer simulation games, where the goal isn’t competing but to collect, build, and customize.

The gaming market needs more products catered to women and their preferences.

Revolve through physical fashion is now connected with Muus Collective, which represents digital fashion and gaming.

“REVOLVE is a trailblazer in the fashion industry with an incredibly loyal community,” said Amber Bezahler, Co-Founder and CEO of Muus. “Through our partnership, players will connect with their favorite brands from REVOLVE and FWRD, and engage with trends through a gamified shopping and styling experience, collectible assets, and deep social interaction. The platform will serve as a fashion playground, empowering players to become their own tastemakers by providing tools for creative expression, peer-to-peer engagement and social sharing.”

REVOLVE GROUP AND MUUS COLLECTIVE FORM STRATEGIC PARTNERSHIP WITH A VISION TO REVOLUTIONIZE FASHION IN GAMING AND WEB3

The partnership has a lot of synergies and makes a lot of sense. It allows Revolve to expand its reach and increase its total addressable market. Muus is female-founded, making for an organic connection between the customer base.

Getting at the forefront of an emerging market is another example of the shovel work Revolve is doing to fortify its moat in eCommerce and fashion. For old apparel retail, these companies have too much of an old-head mentality to get into web3 or digital fashion.

Revolve will receive intense competition from other fast fashion brands like SHEIN, Farfetch, and Fashion Nova, but I am not too worried. Revolve isn’t a Chinese company, which at this moment is like a Scarlett letter. California is the sixth largest economy in the world, giving Revolve a unique proximity advantage – Other cities do not have Los Angeles’ soul or essence.

The luxury apparel market is growing fast, so there will be multiple winners in this space. Although Revolve isn’t the first fashion company entering web3, they are at the forefront of an industry that is just beginning. Apparel companies that do not have technology in their DNA or can connect with their audience via social media will be challenged financially in the future.

I am not a quarter investor, meaning I do not make investment decisions based on every quarterly earnings report. It can take years, even decades, for a great story to materialize. Revolve has a strong brand name in the luxury apparel market, which is a moat. No matter how much money or shiny a new entrance in this market is, they cannot expect to match the prices of, say, a Lululemon or Louis Vuitton and expect the same demand from consumers immediately. Creating brand strength is a slow, organic process that can take decades to build.

Overall, the quarter was very positive. 2022 was a very challenging year, but in the future, we will look back at this time as a great buying opportunity for companies that kept their houses in order so they could keep their foot on the gas toward growth initiatives. Over the next few years, Revolve will separate itself by fortifying its digital infrastructure and strengthening its brand, while many of its competitors will realize they built their houses on sand.

In the early 90s up until the late ’00s, people discounted and underestimated Jeff Bezos.

Stock analysts called Amazon “Amazon.toast” and “Amazon.bomb.” It wasn’t that so many analysts and journalists were wrong; it’s how confident and loud they were in predicting that Bezos would fail.

Amazon as a business made little sense not long ago. Now it is the new normal. Buying things online was more an experiment than an actual business. The process was slow and clunky. Try and remember (if you were born in the 90s) how engaging in AOL chatrooms was a daily activity for internet users in the early 00s.

Amazon worked because Bezos understood the potential of a market that did not exist in the 90s. When that market did materialize, Amazon reaped massive rewards.

Look at Meta the same way. Meta is pouring money into the metaverse, a market that does not exist today. How people use and view the metaverse today is more of an experiment, just like how the internet was in its earlier days.

Mark Zuckerberg sees the bigger picture and is leading Meta to an even bigger powerhouse technology company in the long term. Zuckerberg sees the potential total addressable market in the metaverse. By building the infrastructure now, he is making sure Meta is leading rather than following from behind.

Wall Street and most stock analysts are wrong on Meta because they are trained and taught to look at profitability in a certain way. Zuckerberg has a vision, and Wall Street doesn’t see it. He is on a different level of impact and importance than most journalists and stock analysts.

Am I going to side with the people who said Facebook wouldn’t make it as a business? The same people who said Zuckerberg should have sold Facebook for $1 billion in 2006 to Yahoo, and they overpaid to buy Instagram in 2012?

I think it’s some of the most historic work that we’re doing that I think people are going to look back on decades from now and talk about the importance of the work that was done here.

Zuckerberg’s words and actions have more weight than the best stock analysts and commentators.

I see Meta as a long-term winner, and you can also thank the extremists for that. Amazon was a success story because Bezos was doubted by so many for over a decade. On December 6, 1999, Amazon’s stock price was $106.69. By April 2, 2001, the price had dropped 92% to $8.37 per share.

A price drop of 92% doesn’t just happen unless a consensus of “experts” writes you off as a leader and discounts your company’s business model. The Amazon allure was created because of how wrong and loud the doubters were. The share price appreciation was greater than it should have been because the stock was artificially discounted and pumped downwards for many years.

Meta has its share of detractors, but they appear much more extreme lately. Calling Zuckerberg/Meta “evil” and other bold adjectives is not productive. The debate seems to have been hijacked by the extremists who use righteousness and condemnation to explain their position. The number of negative articles about Meta earnings was predictable, yet journalists’ vitriol is becoming more transparent. You can hear the disdain in people’s voices when discussing anything related to Zuckerberg or Meta.

The number of negative articles about Meta earnings was predictable, yet journalists’ vitriol is becoming more transparent. You can hear the disdain in people’s voices when talking about anything related to Zuckerberg or Meta.

If you have an extremist or slanted narrative, there is not much hope in having an honest dialogue. There is no room for compromise or understanding. Imagine debating with someone about abortion who believes abortion should be illegal with no exceptions for rape, incest, or the mother’s life. The same goes for someone who believes in the right to an elective abortion up to the delivery time under any circumstance.

The Meta hate manifests from an extreme herd mentality based on principle and purity. Much of the biased criticism against Meta overexaggerates the problems they are causing and simplifies a more complicated social issue.

My first question for Meta detractors. Do you want Meta to fail, or do you actually think they will fail? There is a difference between rooting for an outcome vs. looking at a situation objectively.

Lost in the reports were that Instagram Reels had a $3 billion annual revenue run rate in Q3 vs. a $1 billion annual revenue run rate in the previous quarter. That’s a $2 billion increase in just a quarter!

But Facebook is dying, and the metaverse is a waste of money……right?

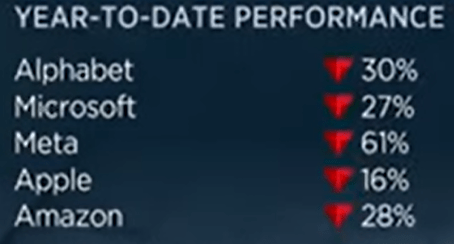

Meta reported a mediocre earnings report but so did Alphabet and Amazon, yet look at which company received the most vitriolic commentary. Meta was tagged as a dying company on freefall, yet Alphabet and Amazon were considered automatic rebound candidates.

Once Meta announced its earnings, the negative articles were ready in full force. The narrative was pre-written.

My last pet peeve is about those that invoke morality into investing. Using morality in investments is silly. If one wants to make a moral impact, volunteer, adopt a child, or start your own business. Investing in companies whose goal is to make a profit and trying to tie that in with morality……I do not get it.

Investors should be intelligent enough to realize investing in a company is not equivalent to a donation. Just as stock buybacks and dividends are not charitable acts to shareholders.

If you think it is morally wrong to invest in Meta, you are likely throwing stones from a glass house and ignoring the moral trade-offs in everyday life.

If it is morally wrong to invest in Meta, does that disqualify you from investing in Alphabet or Apple? What about companies that exploit Chinese workers?

Uber? A history of breaking the law, discrimination, and sexual harassment.

Pfizer? Pandemic profiteering.

Johnson & Johnson? Selling Talc-based baby powder that causes cancer.

Any pharmaceutical companies? Unethical.

Walmart and Amazon? They kill off small businesses.

Big Banks? Just pure greed.

Investing based on morality is not a thing. These are not charities or NGOs. Putting money into a company stock is not a social good or a moral action. It, by definition, is a selfish act since you expect a return. Do people who invest morally (whatever that means) trade off lower returns for investing in companies that are “good.” A lot of this is a bunch of malarkey.

“The fact is, when men carry the same ideals in their hearts, nothing can isolate them – neither prison walls nor the sod of cemeteries. For a single memory, a single spirit, a single idea, a single conscience, a single dignity will sustain them all.” – Fidel Castro

Meta acquiring Oculus Rift VR in 2014 will eventually be the most profitable and vital acquisition for Mark Zuckerberg, by a lot.

Republicans and Democrats have both scapegoated Meta to drive their political agendas.

The Federal Trade Commission has followed the same ethos as Chinese regulators and is blocking every attempted acquisition Meta tries to make.

As Warren Buffet said, “diversification is a protection against ignorance.” Zuckerberg doesn’t need to spread his bets around. He has a clear, singular vision to reshape Meta.

Zuckerberg built Facebook in his dorm room at the age of 19-years old. The odds were against him then. Zuckerberg now has the experience and finances to build the metaverse and make Wall Street look clownish.

At 32, Fidel Castro led the Cuban Revolution and took over Cuba in 1959 until he retired in 2008. At the age of 38, Zuckerberg is conducting a massive undertaking to capture the heart and soul of the metaverse. The battle is already underway. Meta investors like Altimeter Capital CEO Brad Gerstner want Meta to cut back on their metaverse spending. Wall Street says it is draining Meta’s Capex and an unnecessary pet project.

Betting against Zuckerberg is Wall Street’s biggest mistake since it gave up on Tesla and Elon Musk.

Meta is on the right track; ignore the media, shareholders even their employees. Meta is at war to create an open metaverse ecosystem vs. Apple’s closed ecosystem. The time for comfort is over. The next few years will be uncomfortable. Employees treating Meta more like a playground instead of a workplace will likely need to update their resumes soon.

Meta needs to double down on the metaverse. It is time to embrace the chaos.

In business, there are no democratic solutions or proportional representation. Competition is cutthroat, especially in the technology sector. A new start-up company that wants even a 1% market share will need to fight for it, even if it is crushed by Amazon, Microsoft, Apple, and Google.

If Meta wants a meaningful share of the metaverse, it must spend aggressively, not passively, to avoid Apple and Google from catching up to them.

Meta has spent over $15 billion since last year on the metaverse. The losses will likely increase in 2023. Whether they spent $15 billion or only $1 billion, the stock price would have plunged anyway due to the deteriorating macro environment. Okay, maybe not 60% this year, but it still would have been down a lot. There is nothing Zuckerberg or the leadership at Meta could have done to avoid the stock plunge.

Look at Meta and its core advertising business similar to Amazon’s core e-commerce business. Meta is looking to create their own AWS. Amazon, without AWS, is a significantly less valuable company.

I am not saying that Meta should ignore or neglect its core business – Facebook and Instagram. Meta’s core businesses are safe for the next 3-5 years, but the days of being a high-growth company are over if they focus on their social media platforms.

Meta has been hampered by Apple Inc’s privacy changes to its iOS platform, allowing users to opt out of data tracking or Apple’s ATT framework. They are also experiencing fierce competition from TikTok. These headwinds aren’t going away.

Apple is very much like a mafia boss. They wield tremendous power, influence, and control with their app store. Apple, unfortunately, has created a hostile environment, pissing off companies like Meta, Snap, Epic Games, and Spotify with their 30% Apple Tax. Tim Cook holds tremendous political influence and control. Apple is the most owned stock by members of Congress. It is not surprising how the Federal Trade Commission seems more focused on stopping Amazon from acquiring iRobot or Meta from purchasing a startup VR fitness app. Where is the action to prevent Apple’s app store monopoly?

Privacy changes by Apple and competition from TikTok are sealing Meta’s fate to a slow death, just like what happened to Yahoo. That’s why the metaverse is essential. Zuckerberg is trying to create a growth engine where they control their destiny, not Apple.

What Gerstner and other Meta investors are getting wrong about Meta is based on two flawed arguments. They first argue that Meta should heavily focus on improving its core businesses. As a long-term investor, that is a terrible idea. Sure, beefing up Facebook, Instagram, and WhatsApp can help improve EPS margins and elevate the stock price in the short or medium term, but more is needed to address the long-term outlook.

Making incremental improvements to Facebook, Instagram, and WhatsApp is the equivalent of rearranging furniture and remodeling a house. The problem is the house of Facebook and Instagram itself is slowly sinking. Zuckerberg needs to pivot and build another home or universe in the metaverse. Making another world will require time, money, and, most importantly, vision.

The social media industry is no longer investor-friendly, and unpredictable Facebook needed Instagram in 2012, but the landscape is much more competitive now. TikTok is having its moment, but eventually, an even better platform (perhaps BeReal or Gas) will gain prominence, further deteriorating Meta’s market share. These headwinds are irreversible, and the sector is getting more toxic.

Does Zuckerberg need to be more of a caretaker and manage Meta until they get disrupted or lead them as the preeminent technology company of the world? The latter requires Meta to continue to pour money into the metaverse and focus on innovation rather than pleasing short-minded investors who want to make a healthy ROI over the next few years.

Investors’ second flawed argument is that the metaverse is an unknown pipedream and not guaranteed to drive revenue for Meta.

“Some of these VR applications are actually scary good and starting to look better than the non-VR version.”

Meta seems to be making steady progress with Quest Pro and Horizon Worlds, but the current project is still crude. Palmer Luckey, the founder of Oculus, stated, “it is terrible today, but it could be amazing in the future. Zuckerberg will put the money in to do it. They’re in the best position of anyone to win in the long run.”

Of course, it looks a bit clunky and awkward, but the metaverse today is not the metaverse in 2032, and that metaverse will be different in 2042. We have seen plenty of examples of what happens when big companies enter emerging markets too late or unprepared.

Microsoft Zune 2006 Microsoft Kin 2010 Google+ 2011 Amazon’s fire phone 2014 RIP

My goal is not to own shares of Meta and sell them 10-20% higher in one or two years, like most investors. I want to own shares of Meta and sell them 2,000-3,000% higher in the next ten to twenty years.

If Zuckerberg starts listening to popular opinion, Meta will end up just like Yahoo, which didn’t have an alternative growth lever. Zuckerberg must maintain that founder’s vision, not just operating Meta but growing it exponentially.

It is laughable how Wall Street is betting against Zuckerberg again. All he did was create the number-one social media website in the world. Zuckerberg is a founder, not an operator like Tim Cook or Sundar Pichai. Founder-led companies are rare breeds because founders often see the company as an extension of their legacy, which motivates them to do what’s best in the long term. Meta has that edge, and Wall Street is laughably discounting it. Cook is not an innovator. Zuckerberg is. Zuckerberg is a builder, while Cook is a manager.

Meta needs to embrace its start-up roots and become disruptive again. People generally have trouble equating investments with exponential ideas. Wall Street fears uncertainty and embraces certainty, with the metaverse representing much uncertainty. Wall Street invests in the way they want the world to work rather than how it actually works.

Many seasoned Wall Street analysts are very good at analyzing events that have already happened. It’s easy to evaluate a quarterly result, as it is old news. People are terrible at predicting the future, and for some dumb reason, Wall Street thinks the future is easier to predict than in the past.

Morgan Housel wrote an excellent article about probabilities and numbers here:

“There are about eight billion people on this planet. So if an event has a 1-in-a-million chance of occurring every day, it should happen to 8,000 people a day, or 2.9 million times a year, and maybe a quarter of a billion times during your lifetime. Even a 1-in-a-billion event will become the fate of hundreds of thousands of people during your lifetime. And given the media’s desire to promote shocking headlines, you will hear their names and see their faces.

A 100-year event doesn’t mean it happens every 100 years. It means there’s about a 1% chance of it occurring on any given year. That seems low. But when there are hundreds of different independent 100-year events, what are the odds that one of them will occur in a given year?

When eight billion people interact, the odds of a fraudster, a genius, a terrorist, an idiot, a savant, an asshole, and a visionary moving the needle in a significant way on any given day is nearly guaranteed.“

When analysts say Meta has a 1% probability of succeeding in the metaverse, they are full of it. Technological growth is not linear and almost impossible to predict.

I encourage people to save and archive articles today, predicting the metaverse being nothing more than a fad.

Now go back in before 2007 and read articles about Apple’s phone:

“The Apple phone will be exclusive to one of the major networks in each territory and some customers will switch networks just to get it, but not as many as had been hoped.

As customers start to realise that the competition offers better functionality at a lower price, by negotiating a better subsidy, sales will stagnate. After a year a new version will be launched, but it will lack the innovation of the first and quickly vanish.

The only question remaining is if, when the iPod phone fails, it will take the iPod with it.“

“The problem here is that while Apple can play the fashion game as well as any company, there is no evidence that it can play it fast enough. These phones go in and out of style so fast that unless Apple has half a dozen variants in the pipeline, its phone, even if immediately successful, will be passé within 3 months.“

The people that said the iPhone would fail or that consumers would not pay $1,000 for a phone without a keyboard aren’t dumb. The problem is consumer behavior and technology are dynamic. The metaverse is still 3-5 years away. Seamless integration will happen when the software and technology are ready. After that, more advancements will stack on each other.

Mark Zuckerberg said in an interview with Lex Fridman that in the future VR users may use an “expressionist” avatar in casual games and a “realistic” avatar in work meetings.

There will be a time when the metaverse will have widespread adoption. Those who think the metaverse is just a gaming market opportunity should see the bigger picture. The metaverse market is valued at $50-100 billion today and could be worth more than $5-10 trillion by 2030. Think of everything you do online – gaming, shopping, watching videos, zoom meetings, etc. If you make all those things into virtual reality, where the immersive experience is not just comparable but better than real life, that is what Meta is trying to capture, and Wall Street doesn’t understand.

Think about zoom meetings. They are convenient but lack a personal touch where you cannot make eye contact. I prefer face-to-face interactions, but they can be logistically challenging. If a business meeting in the metaverse can re-create those natural interpersonal dynamics without being there in person, that’s easily a market size of over ten trillion. You can apply that to dating, gaming, and classroom education; the possibilities are endless.

As Peter Thiel said: “the best startups might be considered slightly less extreme kinds of cults. The biggest difference is that cults tend to be fanatically wrong about something important. People at a successful startup are fanatically right about something those outside it have missed.”

The metaverse is a future revenue producer that can bring in more than Facebook, Instagram, and WhatsApp combined. For Meta to win the metaverse, Zuckerberg needs to lead maniacally. The way Steve Jobs led Apple to introduce the iPhone and Musk led Tesla to introduce the Roadster. Zealots tend to run highly successful founder-led companies, and Zuckerberg needs to embrace his inner Jobs and act more like a tyrannical dictator.

I advocate our government as a democracy; however, most workplaces do not operate like a democracy. Democratic leadership is not a successful model in high-growth tech companies. Jobs’ leadership at Apple was akin to Fidel Castro or Kim Jong Un than Barack Obama.

Going all-in on the metaverse instead of dipping their toes in the water is necessary for Meta to win. The Cuban Revolution could not have happened Fidel Castro had tried to negotiate peacefully with Cuban President Fulgencio Batista. By cutting back spending to the metaverse, Zuckerberg would admit defeat, and Meta would become the caretaker for legacy social media.

During Meta’s most recent conference call, Zuckerberg sounded like the voice of reason; passionate and confident. Wall Street analysts were the ones who appeared confused, providing dizzying lazy narratives on why Meta had it wrong.

The battle for the metaverse is happening right now, and companies like Apple and Meta are fighting for control. My advice for current investors of Meta, get out if you cannot handle the volatility. Put your money in more mature, stable companies like Alphabet or Apple, which operate more to the expectations of an investment management company. These companies are fine, but that strategy can lead to complacency and laziness. Meta’s approach is poised to capture a large share of the metaverse. A piecemeal approach toward the metaverse means less of a windfall for Alphabet and Apple.

Many people in the government and media desire Meta to fail and are openly rooting for it to happen. If Meta is harmful to society, why invest in it? I invest in how I believe the world works, not how it should work. It is also important to remember the stock price is not an accurate indicator of a company’s health, stability, and growth. Stock prices are based on perception, expectations, and sentiment, especially in the short term.

Zuckerberg is acting with great valor, while Wall Street is motivated by short-sided greed. Meta may fail; epically, however, my money is on a founder who will surpass Jobs, Bezos, and Musk as the greatest entrepreneur of our time.

Elon Musk: “You remind me of when I was a kid and my friend’s angry Mom would just randomly yell at everyone for no reason.”

Senator Elizabeth Warren, aka “Senator Karen,” is at it again. The Senator from Massachusetts is leading a group of her colleagues trying to block Amazon’s $1.7 billion acquisition of iRobot.

She sent the Federal Trade Commission a letter stating: “We urge the FTC to oppose the proposed Amazon – iRobot acquisition. Amazon’s anticompetitive practices stifle innovation and harm consumers, workers, small businesses, and the economy as a whole. The FTC should use its authority under the Clayton Act to prevent the company from further violating our competition laws.”

I find this type of language and posturing from the likes of Senator Karen eerily similar to the actions of the Chinese Communist Party and their regulation against Tencent and Alibaba.

Will the FTC attempt to block every acquisition attempt made by Amazon, Google, and Meta? It seems that way. The Chair of the FTC is Lina Khan. When Khan was a Yale Law Student, The Yale Law Journal published her article, “Amazon’s Antitrust Paradox.” How is Khan supposed to be impartial in evaluating antitrust law with anything regarding Amazon?

Amazon is a profitable company. Many founders build startup companies to get acquired by companies like Amazon. Not all founders of startup companies want to continue competing and potentially get wiped out by their competitors. Many want to cash out on a lifetime of hard work instead of heading a publically traded company. Do you think Brynn Putnam regrets selling her connected fitness company, Mirror for $500 Million to Lululemon? Does Jamie Siminoff have a lifetime of regret selling Ring to Amazon for over $1.2 billion? Many of these startups can use their parent company’s resources and expertise to reach more users when they become subsidiaries. Most importantly, they don’t have to deal with the likes of Senator Karen or Lina Khan trying to regulate their companies to death.

Both Warren and Khan act on ideology and politics. Earlier this year, the FTC sued Meta to stop them from buying Within Unlimited, a small startup virtual reality fitness company. Khan did so against the advisory of her staff, which recommended the FTC not sue Meta.

This crusade against Big Tech is all about gaining power and influence. Companies that became too profitable, and now the government wants to intervene. Remember when Warren ran for President, she was clamoring to break up Amazon, Google, and Facebook but at the same time gladly took their donations.

From an investment standpoint, I see the government meddling in every acquisition as a bad result for everyone. Based on Warren and Khan’s vision, they want to break up these companies and turn Big Tech into the airline industry – A bunch of barely profitable companies with no differentiating advantage and subservient to the government. If the government continues to regulate Big Tech, they will eventually have to bail them out just like they did with airlines, the auto industry, and banks.

I am reminded of Chapter 3 of Zero to One: All Happy Companies Are Different:

U.S. airline companies serve millions of passengers and create hundreds of billions of dollars of value each year. But in 2012, when the average airfare each way was $178, the airlines made only 37 cents per passenger trip. Compare them to Google, which creates less value but captures far more. Google brought in $50 billion in 2012 (versus $160 billion for the airlines), but it kept 21% of those revenues as profits—more than 100 times the airline industry’s profit margin that year. Google makes so much money that it’s now worth three times more than every U.S. airline combined.

Is the goal to turn Amazon into United Airlines? I hope not.

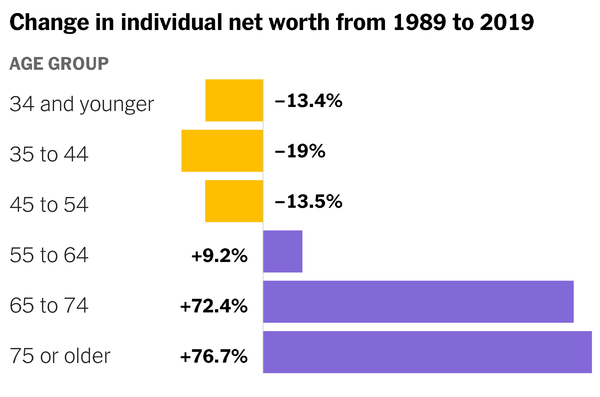

The economy is uncertain. Inflation is raging on. Americans under 54 have less money than adults three decades ago. The journey to wealth-building is challenging; however, investing is one of the greatest equalizers in skyrocketing your net worth. It is accessible to nearly everyone. Not everyone has the time, skillset, or education to become a neurosurgeon. Not everyone can become a senior manager at a Fortune 500 company. Anyone can invest, and the need to do is more important than ever.

The chart shows the median net worth, adjusted for inflation. | Source: Federal Reserve

For people to get ahead, they cannot keep their cash in inflation-losing savings accounts, CDs, or I Bonds. If you have a finite amount of discretionary funds to grow wealth, why put it in vehicles that cannot beat inflation?

A certain amount of risk is needed to get an edge. Even index investing is not enough.

I look at investing as owning a productive asset or a piece of a business. I specifically look at the underlying assertion of the productivity of that business, the return on cash based on cash flows coming out over time, and the general fundamentals around it. Over time I pull money out of my investments and hopefully get more out of them than I originally put in when I bought them.

Fewer people today look at investing like this. The average investor today holds a stock for about 5.5 months. In the 1950s, the average investor held onto their shares for nearly a decade.

Today more people look at investing as paying x amount for x asset and look to sell it to someone else for y. Many people treat their stocks more like collectibles or poker chips than shares of an actual company.

There is absolutely nothing wrong with this mindset; however, it is clear that this is not long-term investing, which is one of the best pathways to becoming wealthy. I look at my managing my portfolio as operating a business. Typically, business owners do not start a business and make day-to-day decisions to sell it for a profit six months later.

Here is where I would allocate $100,000 today under the heavy influence of long-termism. The average holding period is 5-10 years, probably longer if the company’s fundamentals remain favorable.

$10,000

Revolve Group Inc Industry: E-commerce/Fashion Retail Risk: Medium Holding Period: 5-10 years Do I already own it? Yes An alternative company to consider: Lululemon Athletica

In the e-commerce industry, you will have trouble finding a cash flow-positive growing company with no long-term debt. Revolve Group managed through the pandemic and will likely weather a recession better than its competitors. Revolve caters to a higher-income segment, which is less affected by inflation. They will survive while many of their debt-burdened peers will crater, clearing away the competition.

Why am I so bullish on Revolve? They can operate nimbly compared to a larger department store chain like Macy’s or Nordstrom. Traditional apparel retail struggled before the pandemic, so it is no surprise they would have trouble as the economy turned. Revolve has no physical retail presence with a business model that can be modeled globally. They can grow quickly and more efficiently with a concentration on technology, data, and social media influencers.

Revolve advertises where consumers spend most of their time on Tik Tok and Instagram. This digital-first approach strengthens their brand name and allows them to connect with Millennial and Gen Z consumers. Most big-chain apparel retailers spend significant money on traditional media advertisements – magazines, TV, radio, and billboards. In the All-in Podcast, David Friedberg said, “if you don’t naturally have content creation in your blood, you have to go buy a content business, or you are going to die. In the future, all advertising and marketing get replaced by content creation.” Revolve will continue to eat Macy’s and Nordstrom’s lunch while growing its massive social media following, leading to partnerships and collaborations with emerging designers.

More companies will utilize influencer marketing and copy Revolve’s advertising strategy; however, it takes decades, if not more, to develop a luxury brand. The balancing act from being a cool, aspirational lifestyle brand to being affordable to mass consumers is tricky. Revolve knows its core demographic: college-educated women with an income of around $100,000. They target that specific demographic instead of value-oriented customers. By elevating the brand, you can raise prices. Most mid-tier luxury brands like Nordstrom or Macy’s have failed to elevate their brand over the past decade. I believe Revolve is on the path to becoming a valuable luxury brand. The fear of a recession will not cause me to sell my shares; I will likely buy more.

$10,000

MercadoLibre, Inc. Industry: Multinational Technology/Shipping/Financial Risk: Medium Holding Period: 5-10 years Do I already own it? Yes An alternative company to consider: Amazon

MercardoLibre, in a simplistic explanation, is the Amazon of Latin America. Mercado libre, envios, crédito, shops, pago, and publicidad means a lot of industries and growth opportunities.

MercadoLibre is a rare company because of the many positive catalysts; investing in the stock is a no-brainer. The more important question is, why would I pick them over Amazon? There is no right or wrong answer; however, MercadoLibre is building a profitable moat. The total addressable market is enormous, and MercadoLibre is creating an impenetrable business apparatus in Latin America. They have a regional/first-mover advantage, giving them an edge over Amazon and Sea Limited.

The stock to buy and hold forever. One of the biggest knocks on single-stock investing is the risk of investing in one company. MercardoLibre is, in reality, six different businesses in multiple countries, all under one parent company.

Barring a leadership change or extreme political volatility in Latin American countries, this is one stock I am not selling.

$10,000

Roblox Industry: Online gaming/Metaverse Risk: Medium-to-High Holding Period: 10 years Do I already own it? No An alternative company to consider: Unity Software

Question: Do you think the Metaverse will be massively popular and profitable in the future? If the answer is no, there is no reason to invest in Roblox or other Metaverse companies.

Roblox is widely popular, with a robust number of daily active users. My question for the CEO David Baszucki is whether he wants to prioritize monetizing its users or building a high-quality immersive metaverse-like experience.