Aritzia’s Q3 FY2026 was one of its best quarters ever—like a walk-off home run in the playoffs. For the first time in the company’s history, they crossed the CAD 1 billion revenue mark in a single quarter, hitting CAD 1.04 billion, up 42.8% YoY.

Aritzia grew sales by nearly 43% while increasing inventory by only 10%. This means their inventory turnover is accelerating and they’re selling clothes almost as fast as they can get them off the trucks. This leads to fewer markdowns and higher full-price selling, which is exactly why their gross profit margin expanded by 30 basis points to 46% this quarter. This 4.3x “Sales-to-Inventory” growth ratio suggests an operational efficiency that makes even the “Mag Seven” look sluggish.

Compare that to Lululemon: Their inventory grew by 11%, but revenue only grew by 7%. When inventory outpaces sales, it usually leads to one thing: markdowns. In fact, Lululemon’s Q3 earnings call explicitly noted that gross margins were squeezed by higher markdowns (up 90 basis points) and tariff impacts. They have ~$2 billion in yoga pants and gear sitting in warehouses that they’re struggling to move at full price.

Aritzia is actually running a more efficient operation relative to its growth than even Nvidia right now. Here’s a quick side-by-side:

Company

Sales Growth (YoY)

Inventory Growth (YoY)

Ratio (Sales/Inventory Growth)

Aritzia

42.8%

10%

~4.3x

Nvidia

62%

~32% (9M cumulative)

~1.9x

Lululemon

7%

11%

<1x

Aritzia’s ability to scale this aggressively while staying so disciplined on inventory is retail execution at its finest, turning hype into real, high-margin momentum. If you’re looking at consumer discretionary winners in this environment, Aritzia is flexing harder than most realize.

This quarter also saw the late-October launch of the Aritzia Mobile App, which hit 1.4 million downloads and became the #1 shopping app in North America on day one. E-commerce revenue surged 58.2%, proving that “Everyday Luxury” translates perfectly to a high-frequency digital experience.

In 2027, Aritzia isn’t just signing a lease; they’re opening a new 40,000 square foot flagship store of the former Nordstrom footprint in Vancouver’s CF Pacific Centre. Aritzia is officially planting its flag on the grave of the defeated old guard.

This is the coronation of a new king. It marks the definitive shift from the bloated, “everything-for-everyone” department store model to a new, aggressive power dynamic. Aritzia has engineered a psychological moat known as “Everyday Luxury.” This isn’t just fashion; it’s a socioeconomic pivot that captures the soul of the modern consumer:

High-End Design: The clothes look like they belong on a Paris runway (minimalist, high-quality fabrics, tailored fits).

Attainable Pricing: Because they control the supply chain, they can sell that “look” for $150–$400 instead of $2,000. By pricing themselves 30–40% below heritage luxury (The Row, Celine) but 20–30% above fast fashion (Zara, H&M), they’ve created a “sweet spot” of attainable exclusivity.

The Result: They’ve captured the “HENRY” (High Earner, Not Rich Yet) demographic. This group is remarkably resilient to macro downturns because they view Aritzia as a “reasonable” yet “necessary” indulgence rather than an extravagant splurge.

The Psychology: Since “big” milestones (real estate, stable pensions) are increasingly out of reach for many, the HENRY demographic is reallocating their discretionary cash into “micro-luxuries” that provide immediate status and emotional ROI.

As we are witnessing with Saks, the “department store” represents the old middle class: a place where you go to see a little bit of everything. It’s a dying generalist model in a world that’s increasingly specialized.

The Old Way: Middle class = Access to variety.

The New Way: Middle class = Access to a vibe. Aritzia doesn’t just sell clothes; it sells a lifestyle aesthetic. When you walk into their “Super Flagships,” you aren’t shopping; you’re participating in a brand-curated experience.

The stock is trading at record highs with a P/E that reflects “perfection.” But Aritzia is just hitting its stride. They’ve successfully moved beyond “leggings and hoodies” into a full-wardrobe solution. It isn’t just superb execution by management; it’s capturing the vibe of today’s consumer.

I bought the stock as a small position in 2023 and have held it and will continue to hold it. If we’re using a baseball analogy, we are still very early. For Aritzia’s growth, we haven’t even entered the 7th inning stretch. Aritzia currently has roughly 72 boutiques in the US (out of 139 total). For context, Lululemon has about 374 stores in the US. Aritzia’s stated goal is ~150 boutiques total by 2027, with long-term potential for 180- 200+ overall, focusing heavily on US expansion (8-10 new boutiques annually, mostly in the US). If Aritzia hits its 150-store near-term target, revenue will likely triple as brand awareness hits a tipping point.

I am officially pegging Aritzia as a stock to buy during a market correction or pullback. Unlike legacy retailers, Aritzia is currently expanding its US footprint into a demographic that views “Everyday Luxury” as a non-negotiable part of their personal identity. This psychological moat, combined with an operational efficiency that is scaling faster than its infrastructure costs, makes Aritzia uniquely qualified to weather consumer weakness better than almost any peer in the sector.

If the market gives me a discount on this level of execution, I’ll take it.

Revolve Group (NYSE: RVLV) is the forgotten champion of apparel retail. While Wall Street obsesses over hyper-growth names and retail investors chase the next meme stock, Revolve quietly operates one of the strongest, most defensible business models in the entire consumer sector. It’s dismissed as “just another overpriced clothing seller,” but that superficial take misses two genuine superpowers that are extraordinarily rare in the apparel sector. This unique combination creates a company that is antifragile in a brutal, cyclical, low-margin industry, a combination that deserves far more attention than it gets.

Superpower #1: A Pristine, Fortress-Like Balance Sheet

Revolve has more cash and cash equivalents than total liabilities. This isn’t total assets minus liabilities. This is cash-on-hand exceeding all debt. As of September 30, 2025, Revolve held $315 million in cash, with total liabilities of just $226, leaving it net cash positive by nearly $90 million. (Revolve Group Announces Third Quarter 2025 Financial Results, 2025) In an industry notorious for leverage-fueled boom-and-bust cycles, this is almost unheard of. Look at Revolve’s closest competitors and legacy apparel names:

The RealReal → Negative net cash, drowning in $500+ million of debt

Victoria’s Secret → $4 billion in long-term debt, with cash covering only a fraction.

Guess? → Leveraged with debt-to-equity over 2x

Macy’s, Kohl’s, Abercrombie in their prior incarnations → Perpetual debt refinancings amid endless store closures

Most apparel retailers use leverage as oxygen. Revolve doesn’t need it. Zero net debt (actually net cash) gives them a massive margin of safety that investors in this sector are simply not accustomed to. In a downturn, Revolve can keep the lights on indefinitely without ever visiting a bank. In an upturn, they can aggressively buy back stock (they’ve already repurchased over 20% of shares outstanding since their 2019 IPO, including $100 million authorized in 2023), or acquire distressed brands/competitors for pennies on the dollar. Having such a fortress balance sheet creates real optionality.

Superpower #2: Consistently Elite Gross Margins (54% and Climbing)

The average apparel retailer scrapes by with gross margins of 30-50%. Revolve delivered a 54.6% gross margin in Q3 2025 (up 350 basis points YoY) and has maintained a 50-55% gross margin range for years. For context:

Louis Vuitton (LVMH) → 66%

Lululemon → 59%

Zara → 55-57%

Most everyone else → 30-45%

Revolve is operating at the same rarefied level as the very best branded apparel players on earth, despite being a pure-play online retailer without a physical-store crutch. Why does this matter so much? Because elite margins are Revolve’s ultimate defense against Amazon. Retail investors see “expensive clothes” and assume the model is fragile. In reality, those premium prices are the moat. Millennials and Gen Z raised on Instagram and TikTok aren’t shopping for the cheapest white t-shirt: they’re buying an identity, or an outfit that photographs well at Coachella. Revolve sells social currency. Customers happily pay 2–3 times more for the outfit that might cost less elsewhere because they’re paying for curation, discovery, and status. That willingness to pay a premium is exactly what produces 54%+ gross margins and sustains an average order value of $306 in Q3 2025 (up 1% YoY).

And those margins are what keep Amazon at bay. Amazon dominates commodity fashion: fast, cheap, endless selection. If Revolve ever tried to compete on price, Amazon would crush them with its scale and logistics. But Revolve isn’t playing that game. They’re playing the art of the brand premium game, something Amazon isn’t going to win. Even after 25+ years and billions invested, Amazon has failed to crack premium or luxury fashion in any meaningful way, with a fashion gross margin hovering around 20-30%, far below the industry standard. Jeff Bezos himself has admitted that building a real fashion brand is one of the few things Amazon hasn’t figured out.

The Rare Combination

Put the two superpowers together, and you get something compelling:

A net-cash balance sheet → survives any storm, buys back stock aggressively, and is opportunistic with M&A.

54%+ gross margins → funds growth, defends against Amazon, produces torrents of free cash flow (up $265% YoY to $59 million in the first nine months of 2025.

This defensive balance sheet and offensive margin profile is the definition of antifragile in retail.

Revolve is clearly doing something different: one that builds on digital and social infrastructure to erect a curation and brand moat. They sell the Revolve experience, which allows them to charge premium, full-price prices (high Average Order Value). Using first principles, Revolve’s main product isn’t a dress; it’s the marketing expense. The influencer trip is not just a cost; it is the intangible asset that allows them to maintain a $300 price point for a dress. This experiential luxury marketing, powered by a network of 5,000+ influencers, has driven its owned-brand penetration to 35% of sales, further boosting margins.

The focus on experiential luxury marketing allows Revolve to build a digital model while using temporary pop-ups as low-CapEx market research before committing to a permanent location. Their Aspen pop-up in December 2024 converted to a full flagship in June 2025 after crushing performance metrics, and they’re replicating the playbook with a permanent store at LA’s The Grove. Focusing on brand experience, margins, and building a cash fortress creates optionality, which is a much different playbook than most apparel retailers play: heavy CapEx expansion to drive growth, which is more inflexible and likely requires leverage.

Very few companies in any industry possess both traits simultaneously. When you find one, especially one trading at a reasonable earnings multiple with a proven ability to grow, it’s worth paying attention. Revolve isn’t a “hot” stock. It doesn’t have 150% YoY growth. It is a quiet, compounding machine built on genuine structural advantages, like a pristine balance sheet and 54% margins that the market keeps overlooking.

Philadelphia Phillies starting pitcher Zack Wheeler

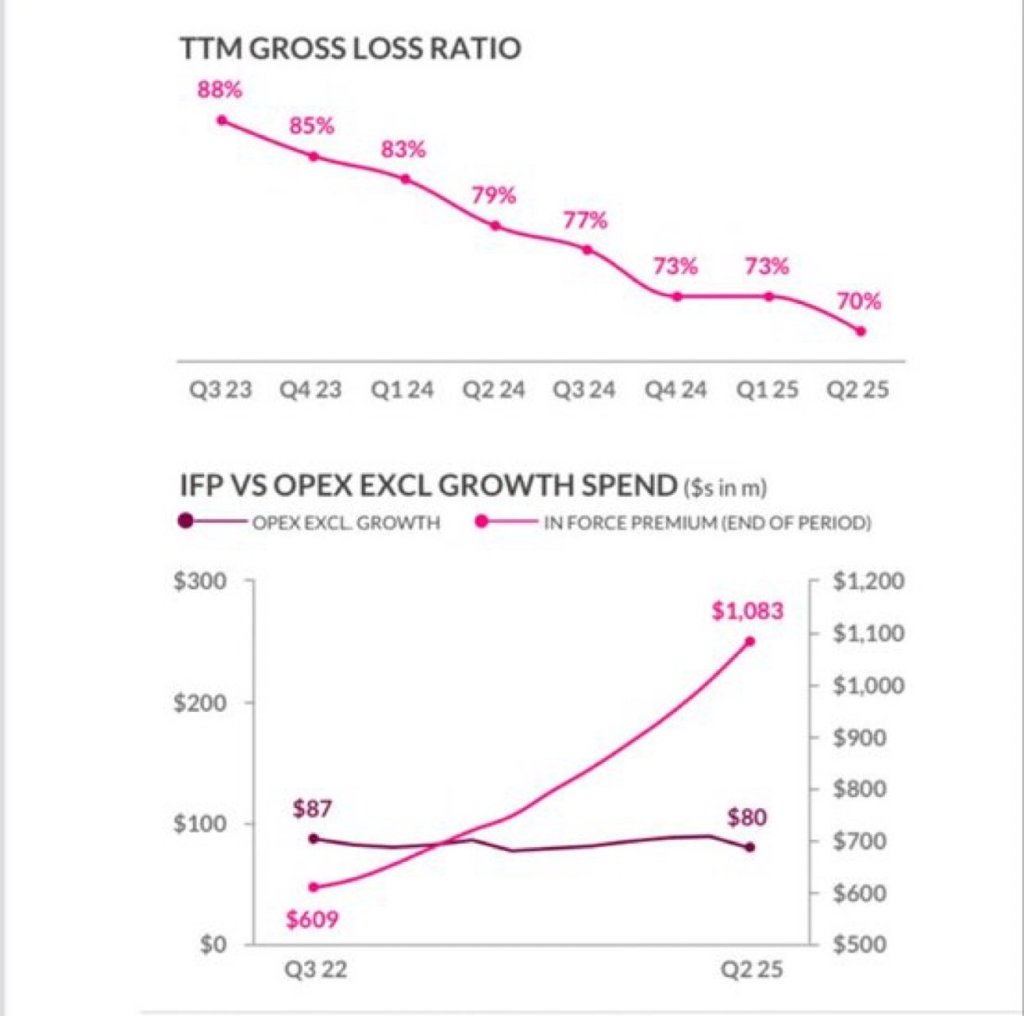

As an investor, I’ve had a love-hate relationship with Lemonade stock. I loaded up too heavily right after its 2020 IPO, only to regret not buying more aggressively when shares dipped into single digits. If you’re considering this name, approach it with caution—it’s a classic high-risk, high-reward bet. Lemonade remains a young company in its growth phase, far from maturity.

In hindsight, the stock’s wild ride in 2021 was fueled by meme-stock mania. It skyrocketed to $188.30 on January 12, 2021, despite the company having under one million policyholders and no auto insurance offering at the time. That bubble burst spectacularly, but beneath the surface, Lemonade’s fundamentals are showing real signs of improvement.

Back to the Drawing board:

The company has always excelled in technology, innovation, and customer acquisition. Profitability, however, has been its Achilles’ heel. I’d liken Lemonade to a highly touted high school baseball pitcher: a laser fastball and a nasty arsenal of pitches, but zero command on the mound. Without control, even the most talented arm flames out quickly; a great repertoire of pitches means nothing if you don’t know where the ball is going.

For a while, its business model reflected this wildness: impressive growth and customer attraction (the 103-mph fastball and filthy slider) were negated by sloppy underwriting (walks and hit-by-pitches). Critics often hammered the company’s high loss ratio as an unsustainable business model.

Think of Lemonade as a young Roy Halladay or Zack Greinke. Both were first-round draft picks who bombed early in their MLB careers, getting demoted to the minors amid mechanical issues and poor results. But they adapted, refined their approach, and emerged as Hall of Famers. Lemonade is on a similar trajectory.

Rebuilding the mechanics

The data over the most recent quarters tells a story of Lemonade tackling its core risks head-on:

Loss ratios are improving dramatically, signaling better risk management and a tighter command of its underwriting.

It has slashed its quota-share reinsurance from ~55% to ~20%, meaning it now keeps more of the premium (and risk) in-house.

After pulling back on its auto insurance rollout, underwriting discipline has strengthened, setting the stage for renewed expansion.

At its core, Lemonade’s business isn’t as complicated as it seems. It’s exceptional at drawing in new customers through its AI-driven, user-friendly platform. If it can continue tightening risk controls, revenue growth should accelerate while losses/expenses stabilize.

The Bull Case Ahead

Wall Street is sleeping on the roadmap ahead. I expect Lemonade to rev up its auto insurance product, expanding beyond the current nine states. New offerings like phone or travel insurance could further juice growth, pulling more users into the ecosystem and unlocking bundling discounts for multi-policy holders.

I’m not hyping this as a sure thing, but my optimism feels more grounded now: rooted in a business that appears primed for scalable profitability. That said, risks abound: Lemonade lacks a deep moat against competitors or economic headwinds, and plenty could still derail it, much like a pitcher blowing out their elbow on a single throw.

Analysts will likely pile in late, chasing momentum rather than leading the charge. I could be wrong, falling into the retail investor trap of being too early or clinging to a thesis that fizzles. Uncertainties remain, but Lemonade looks increasingly deserving of a small portfolio allocation. The bull case could spark explosive upside volatility, especially as AI evolves from infrastructure plays (like Nvidia or Google) to application-layer disruptors. Lemonade’s AI-powered insurance model positions it to capitalize on this shift, potentially delivering venture-like returns in the years ahead. While it’s no Palantir clone, the ride ahead could be like an epic roller coaster.

In 2016, I invested in Tapestry (TPR), betting on Coach as an undervalued brand poised for a turnaround. It was one of the first stocks I bought as a new investor. My thesis was straightforward: the stock could reclaim its March 2012 peak of $79.70. Nearly a decade later, my prediction proved correct, though the road was far from smooth.

Tapestry faced significant challenges, including the 2019 ousting of its CEO, the 2020 resignation of another due to ‘personal misconduct,’ and a 2024 court ruling blocking its merger with Capri Holdings. Yet, TPR has outperformed the likes of LVMH, Lululemon (LULU), Capri Holdings (CPRI), and Nike (NKE) over the past five years—the very stocks I eyed when TPR struggled. Those same peers now sit well below their prior peaks.

I acknowledge luck played a role. Had the Capri merger proceeded, TPR would likely be trading in the $50–$70 range today, far below its current levels. Now, with TPR soaring past its 2012 high, I’ve shifted my strategy and trimmed my position to lock in long-term gains. If the stock continues to climb, I’ll likely reduce my holdings further.

My original thesis—that Coach was trading at a bargain—no longer holds. In a tough luxury market, Coach has unexpectedly gained pricing power for a mid-tier brand, fueled by a reshaped brand narrative and the TikTok-driven success of its Tabby Bag. However, Kate Spade, accounting for about 15% of revenue, remains a weak link due to inconsistent branding and declining sales, tempering my optimism.

Management deserves credit for Coach’s turnaround, but I remain cautious. Tapestry’s cyclical nature ties its success directly to consumer spending and economic conditions. A weakening economy would likely pressure sales.

Tapestry’s acquisition strategy is my primary concern. Selling the unprofitable Stuart Weitzman brand was a smart move, but the pursuit of the Capri merger suggests management may doubt Coach’s standalone growth potential. Given the lackluster outcomes of the Stuart Weitzman and Kate Spade acquisitions, future M&A activity could increase debt and strain cash flow.

My suggestion? If Tapestry is set on acquisitions, it should issue new shares to fund a targeted purchase, such as a niche luxury brand with strong growth potential. This approach would preserve cash and avoid debt, though it risks diluting existing shareholders. It could create more long-term value than increasing the dividend or buying back stock to where it’s trading currently—an action that offers limited upside if the stock corrects.

While I’ve enjoyed reinvesting dividends during the stock’s recent climb, weaker economic indicators, like declining retail sales, suggest uncertainty ahead. Most companies in the consumer cyclical sector face headwinds from slowing spending, and TPR is no exception.

That said, TPR isn’t wildly overvalued. With an upcoming earnings report and Investor Day looming in September, short-term upside potential remains. I’m cautiously optimistic and will monitor these events. My goal is to sell more shares at a higher price before the end of the year.

After Joe Biden dropped out of the 2024 Presidential race in July, something notable happened: Zoom, the videoconferencing app, was used as a political rally call for Kamala Harris. On a Thursday summer night, a Zoom fundraiser attracted more than 200,000 viewers, making it the largest Zoom call in history. Several other Zoom fundraising calls have followed, started by diverse communities like “White Dudes for Harris,” “Dead Heads for Harris,” “Cat Ladies for Kamala,” and “Swifties for Kamala.”

I am not interested in discussing Harris’s surge in popularity but in why her supporters decided to use Zoom instead of Google Meet, Microsoft Teams, or Webex Meetings.

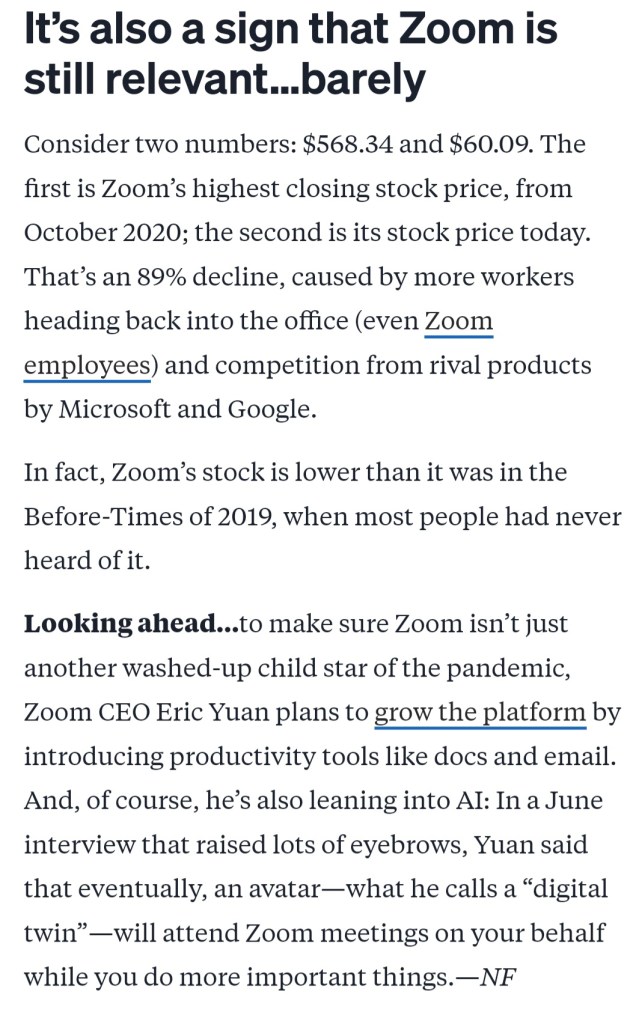

Investors in Zoom should feel confident in the business. Zoom’s death as a pandemic company is greatly exaggerated. The stock appears hated, I guess it’s a symbol or a vestige of a depressing moment in history, yet the fundamentals remain intact.

Zoom is the people’s choice because, through empirical testing, its audio and video quality ranked higher than its competitors.

Due to its ease of use, consistency, and complete/advanced features, it also flexes its brand power, even over Microsoft and Google.

Why does this even matter?

Despite the exceptionally bearish sentiment from Wall Street and the financial media, Zoom has proven its resilience. Sentiment, after all, is subjective and can quickly turn around as expectations and emotions change. This should reassure investors of Zoom’s potential.

Perhaps the narrative of Zoom being a pandemic boom-and-bust company is incorrect. The business is operating just fine and taking the necessary steps to transition from a popular one-trick video conferencing app to a full-fledged AI enterprise platform.

The video conferencing space is crowded, with heavy hitters who do not have the same relevance as Zoom on a consumer level.

How many people do you know to use Microsoft Teams outside of a work setting? Shouldn’t Teams or Google have more relevance or usage if it has the same functions and capabilities as Zoom?

Since Zoom is an enterprise tool, consumers downloading and using the app don’t move the needle or meaningfully impact the balance sheet.

It creates a halo effect for the enterprise business and enhances brand recognition.

Zoom is not a social media platform, yet it has brought an impressive amount of users for fundraising purposes, creating a sense of community and energizing supporters.

Unnecessary negative-slanted wording from a Morning Brew newsletter

If Zoom can impact an election and help elevate a candidate into the presidential office, something about the platform gives it a potential competitive advantage with a long-term wide moat. You can argue that Zoom cocktail parties and Zoom Yoga sessions are more of a pandemic-era fad, but affecting voter turnout is much more impactful.

Despite the recent downturn in Wall Street’s sentiment, I remain optimistic about Zoom’s long-term potential. The demographic most comfortable using the platform will eventually dominate the workforce, while those resistant to technological change will phase out. This bodes well for Zoom’s future growth.

Zoom’s platform is not just a tool; it has gained cultural phenomenon status. It’s the preferred choice among Gen Z across various industries, from education to healthcare, legal, events, government, and personal use. Understanding this trend is crucial for anyone interested in technology and its impact on society.

Zoom meetings, classes, and virtual court hearings are here to stay because they are widely popular, in high demand, and in a growing market.

Strong balance sheet: Zoom has approximately$7.5 billion in cash and zero debt. Roughly 40% of the company is cash (cash divided by enterprise value), signaling a high margin of safety. Compare that to Salesforce, which has an enterprise value of about $274 billion, $10.6 billion in cash, and $40 billion in debt.

Founder-led with strong key executives.

AI-infused with innovative ideas like AI avatars that trend towards the future of enterprise work tools.

Popular among a demographic that will make up most of the workforce in 10-20 years.

Zoom has become a popular company to “hate on” from Wall Street for various reasons that I believe are mainly irrational and short-sided. I fully expect Zoom to see a lift in revenue and guidance due to its solid fundamentals and riding the right enterprise software trends. If this happens, the narrative of how the company will dramatically shift more positively.

I wouldn’t call what Zoom has a network effect, but the virality appears very sticky. An enterprise app that transcends enterprise and has a profound impact on society outside of just business. Zoom is an attractive investment with much of the downside risk already priced in.

Once the undisputed athletic apparel champion, Nike has faced increasing challenges recently. With Mark Parker’s departure and John Donahoe’s subsequent leadership, the company is struggling to keep pace with rapidly changing consumer preferences, particularly among Gen Z and Millennial demographics. The stock has seen a significant decline, underscoring the urgency of the situation.

A New Playbook

Starbucks’ revival under Brian Niccol’s CEO appointment is a powerful example of the transformative potential of strategic leadership change. Nike, too, could benefit from a bold and quick decision, emphasizing the need for risk-taking in order to reap potential rewards.

Sheryl Sandberg: The Perfect Choice

With her experience as Facebook’s COO, Sheryl Sandberg possesses a unique blend of skills and insights that are directly relevant to Nike’s current challenges. Her deep understanding of social media and her passion for women’s empowerment aligns perfectly with the company’s visions and goals, making her the perfect choice to lead Nike into a new era.

Leveraging Women’s Sports and Social Media

The growing popularity of women’s sports, exemplified by the rise of athletes like Caitlin Clark, presents a significant opportunity. Nike can tap into a powerful cultural force by investing in women’s sports and leveraging social media to connect with younger audiences. As a female executive who has broken barriers in the tech industry, Sandberg is well-positioned to champion women’s sports and empower female athletes.

Cultural Understanding

According to a recent survey, 40% of Gen Z and Millennials find women’s sports more exciting to watch than men’s, compared to about 25% of Gen X and Baby Boomers. Moreover, social media has become integral to how consumers engage with sports. Six in 10 Zoomers are very interested in content creators on Twitch or YouTube chatting about sports on live streams, and 70% discovered or deepened interest in sports through fan communities on social. This indicates a significant opportunity for brands to leverage social media to connect with younger audiences.

A Game-Changing Move

Sheryl Sandberg’s leadership could be the game-changer Nike needs to regain its cultural relevance and standing. Her proven ability to drive revenue growth, build strong teams, and foster a positive company culture would be invaluable in navigating the challenges of a rapidly evolving market, instilling hope and optimism in the company’s future.

Sandberg’s expertise and track record are based on optimizing and fine-tuning advertising revenue. She can create a more effective ad strategy, creating engaging and shareable content that builds communities and drives engagement.

The Time is Now

By bringing Sheryl Sandberg on board, Nike would signal its commitment to innovation and demonstrate its understanding of the changing landscape of sports and consumer behavior.

Caitlin Clark’s meteoric rise is changing the narrative of how we talk about women’s sports and how to market women athletes effectively. It’s a shift that’s happening now. Nike needs to adapt quickly, and bringing in a proven winning rockstar CEO can dramatically turn things around.

I endorse giving Sandberg a blank check to turn around Nike. John Donahoe is the wrong CEO to revive the brand. Sandberg’s background in technology is not directly relevant to the athletic apparel industry, but Nike has never been just an athletic apparel company—it’s a global cultural brand that celebrates great athletes. This is the right time, and Sandberg is an even better fit. I urge the Nike board of Directors to take action because quite, honestly, it makes too much sense.

Revolve’s venture into brick-and-mortar retail with its first Aspen, Colorado store was not just a success, but a triumph. The initial pop-up store in December was a mere glimpse of the potential, and the decision to sign a multi-year lease was a resounding testament to Revolve’s ability to exceed its own expectations.

Why does this matter? Revolve, a digital-first business that has been diligently building its brand and e-commerce model, has made a strategic shift. Despite previous comments from earnings calls suggesting no serious plans for retail, Revolve has now embraced the potential of the physical retail space.

But the results were too good to ignore. It wasn’t so much that they sought retail, but demand called, and Revolve answered the call.

Aspen is just the beginning. With a robust digital marketing apparatus already in place, and the success of its first brick-and-mortar store, Revolve is poised for further expansion. This is a pivotal moment for Revolve, as it can now potentially translate its digital brand into a network of physical stores, paving the way for future growth.

This has the potential to increase an already impressive high average order value from the benefits of in-person shopping: impulse buyers from being able to feel and touch the merchandise. The Aspen store has also been a source of bringing in new customers, which is Revolve’s advantage and opportunity.

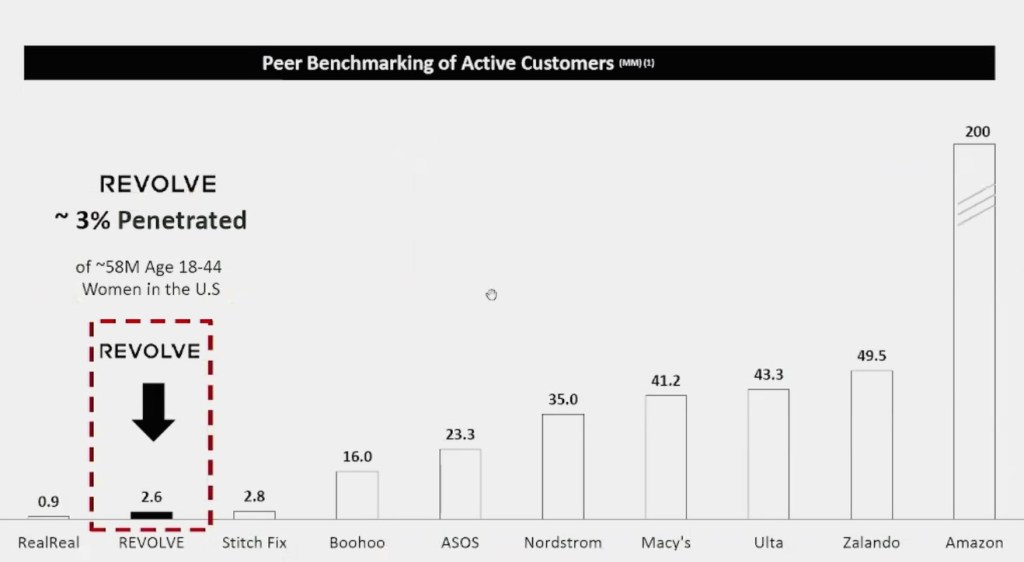

Advantage: Revolve’s customer base is mostly Millennial and Gen Z females. Roughly 60-70% of Macy’s and Nordstrom’s customers are Gen X and Boomers. I am not optimistic about legacy department stores. They have a problematic long-term business outlook. Macy’s is investing heavily in Bloomingdale’s and Bluemercury, but their brand name has declined significantly in the past decade. Nordstrom is doing a better job attracting young customers due to its off-price retail chain, Nordstrom Rack, but focusing on deals and discounts is a race to the bottom, and they will likely lose to Amazon, Walmart, and Target. I never understood Nordstrom’s business model because the off-price division does not complement the flagship stores. A “luxury” brand shouldn’t target consumers on a budget and vice versa.

Opportunity: Macy and Nordstrom need help mightily attracting Gen Z customers. It’s dire. Both companies will likely not show any year-over-year sales growth. Macy and Norstrom will eventually go private and leave the public market soon. It’s not a matter of if but when. These businesses may be able to restructure by going private, but it will likely take a very long time. Going private would also make raising capital difficult and cause a potential departure from key employees. Once the move happens, the capital and employees will likely shift towards a company like Revolve.

Is the Aspen store a signal for immediate retail expansion? I hope not. The focus should remain on building the digital platform and live events—Coachella, The Super Bowl, Cannes, etc. Physical retail should only complement the existing business unless the data overwhelmingly suggests otherwise. Much work is needed to build the brand through product/category expansion and international growth, which is more cost-effective through social media and pop-up events.

It would be premature for Revolve to make an aggressive retail push like Aritizia (3-5 new stores annually by FY27). They also don’t need it. Revolve has a much bigger online presence than other digitally native brands like Figs, Warby Parker, or Allbirds.

As a shareholder, I advise Revolve management to focus on curation rather than expansion. Identify 3-5 unique locations to create a highly personal and immersive experience. The stores should be bright and feature natural wood fixtures, making them engaging places to shop. Aspen works because it is an affluent city that blends luxury, charm, and scenic beauty. However, a store like Aspen is not scalable to a nationwide rollout. The ambiance is more subtle than in bigger cities like Las Vegas or Miami. It offers lesser-known brands in the high-end category to stand out more to a wealthy clientele.

I have identified some markets for Revolve to explore that can create a potential Aspen effect:

Park City, Utah Nantucket, Massachusetts Jackson Hole, Wyoming Charleston, South Carolina Carmel-by-the-Sea, California Key West, Florida Santa Fe, New Mexico

Entering smaller but highly profitable markets is a strategic move that makes perfect sense. Revolve, armed with ample marketing data, is poised to make prudent decisions and identify a few Aspen-like markets. The goal is to create a small footprint of high-ROI stores that offer a curated collection of luxury fashion brands—a blend of art, immersion, and boutique feel. The key is a luxurious bespoke experience, catering to the target audience’s preference for experiences over value or deal-hunting.

There is still plenty of room to grow. Despite a challenging macroeconomic picture for luxury retail, I haven’t sold any shares. I am confident in the business’s fundamentals and see a long-term pathway for growth and overperformance.

Why Tesla Shareholders should emphatically vote to approve Musk’s $56 Billion pay package

Musk’s compensation isn’t just about dollars; it’s about shaping Tesla’s destiny and soul. As shareholders, we are not just passive observers but active participants in this journey. Our votes on his pay package are a direct reflection of our belief in his vision and our commitment to Tesla’s future.

Under Musk’s guidance, Tesla’s stock price has skyrocketed, defying recent market turbulence. This dramatic rise starkly contrasts the stock’s value in 2018, which was a mere $21. Long-term shareholders have reaped substantial financial gains from this growth, a clear testament to Musk’s undeniable influence. This is not a personal viewpoint but an impartial, nonpartisan, indisputable reality.

Musk’s strategic decision-making has been a driving force behind Tesla’s success. Against all odds, he has led the charge in electric vehicle and clean energy innovation, reshaping entire industries. His ongoing leadership is not just important; it’s crucial for maintaining Tesla’s competitive edge and ensuring a prosperous future for the company. The potential loss of his leadership should inspire every shareholder to vote in favor of his compensation package.

Tesla’s long-term vision hinges on visionary guidance. Voting on compensation reflects shareholders’ trust in Musk’s ability to steer the company toward its goals. Elon’s compensation package is entirely contingent on achieving ambitious targets. If Tesla fails to meet specific triggers, Musk receives no compensation. This ensures that his pay is directly linked to the company’s success, aligning his interests with the shareholders. This alignment of interests should foster trust and confidence in every shareholder.

Tesla shareholders should ask themselves why they invested in the company in the first place. How many cars they sell this quarter or next quarter is less important than how they are positioning themselves for a Robotaxi world. This is an AI and Robotics company. Shareholders who dislike Musk or want to invest in a typical car company that achieves predictable quarterly numbers can choose from a bevy of other publicly traded companies.

Actual long-term Tesla shareholders don’t see Tesla as a car company; they see it as a venture with a start-up mindset into sustainable energy, AI, and software development. At heart, the vision is greater than just manufacturing vehicles. There is a clear line in the sand. Do you want Tesla to attempt to achieve moonshot or be a mediocre car company run by a Wall Street figurehead chasing predictable quarterly numbers?

If you vote no, you clearly communicate that you do not want Elon running Tesla. It’s a big middle finger to spite someone when the sentiment and stock price are low. Accelerate the transition to sustainable energy, revolutionize transportation, and produce humanoid robots at scale vs. grabbing low-hanging fruit and achieving goals with lower-moderate upside?

The rhetoric being spewed by pundits is biased, carrying a political agenda. Elon Musk’s loudest and most vocal critics are likely not Tesla shareholders, meaning they have no skin in the game. Think about it. Why would you “invest” in a company with a CEO you find deplorable? Does that make sense?

A story about business and technology has been hijacked by partisan fundamentalists. This rabid audience is tribal and less open to listening to opposing views. Elon Musk has been tagged as a villain that commentators will continue to deride. They have used the recent downturn in the stock as ammunition to defend their ideology.

Attacking Elon Musk has become a proxy for attacking President Trump. It’s that simple. These pundits are not your friends and are far from advocates of unbiased investment advice. Tesla stock could 100x and produce more than 200 million all-electric cars in a year; Elon Musk is still a con man to them, and the company is still a bad investment. Facts, data, and performance don’t change a fundamentalist’s opinion. It also won’t get them to admit they are wrong. The goal is to see Elon and Tesla fail spectacularly. Ask yourself if their interests align with yours as a shareholder.

I have voted yes because Elon’s pay compensation is necessary and mission-critical to Tesla’s future growth. Not voting for this package could potentially have catastrophic consequences. Losing his leadership would be a setback for Tesla and the future of our society as a whole. Musk is a man on a mission, and we as a society are in debt for his projects, which are critical to improving humanity through Tesla, SpaceX, Neuralink, The Boring Company, X, and xAI.

Elon Musk has revolutionized the electric car industry and taken on unimaginable financial and reputational risks. His sacrifices and suffering paved the way for Tesla’s success, allowing shareholders to thrive. This pay package is a testament to his past performance and a powerful incentive for future success. I voted yes because it keeps the trailblazer in place and re-positions Tesla into propelled growth for the next decade.

A Zoom court hearing in Michigan involved a defendant who was allegedly caught driving with a suspended driver’s license.

I invest in both companies.

I see solid fundamentals and strength in both businesses.

It is important to remember that the growth is still early in markets that are still evolving. Evaluating these companies based on traditional valuation metrics is problematic because these industries are far less static than other sectors. Both have bright futures, but Zoom would have a slight edge if I had to choose the better long-term investment based on a risk and reward estimation. This suggests a potential for high returns, inspiring optimism in potential investors.

Zooming in: Misunderstood as a one-product company:

Company

Revenue (Billions)

Gross Profit (Billions)

Earnings (Millions)

Palantir

2.23

1.8

209.8

Zoom

4.53

3.5

637.5

1. Core Functionality & Additional Services:

Zoom offers foundational features like video conferencing (Meetings), chat, and phone calls.

But on top of that, they provide additional services built around this core functionality like:

Rooms – dedicated video conferencing hardware for meeting spaces.

Events – hosting large-scale virtual events.

Contact Center – cloud-based call center solutions.

2. Openness and Integrations:

A key feature of platforms is openness. Zoom offers a Developer Platform (https://developers.zoom.us/docs/), allowing third-party developers to create custom applications that integrate with Zoom’s core services.

This extends Zoom’s functionality and caters to specific user needs. Imagine a Zoom app for scheduling meetings directly from your calendar.

3. Diverse User Base and Use Cases:

Zoom caters to a wide range of users, from individuals to large enterprises.

The platform’s flexibility allows it to be used for various purposes, such as business meetings, virtual classrooms, telehealth appointments, and even social gatherings.

In essence, Zoom provides a foundational communication platform and allows users and developers to build upon it to create customized experiences. This is a core difference from a product company that offers a fixed set of features.

Zoom has a larger TAM and a much easier pathway toward highly profitable growth.

According to the most recent reports, Zoom boasts 191,000 enterprise customers. While the exact number might fluctuate, Palantir has several hundred enterprise customers (1,300-1,500), significantly less than Zoom’s reported customer count.

Palantir primarily targets large enterprises, providing software platforms for data integration and analysis, often with over 10,000 employees and significant revenue. Zoom has a much broader customer base with businesses of all sizes.

One company targets a niche market of government agencies and large corporations with specific complex enterprise software solutions. The other offers a communication and collaboration solutions platform to businesses of all sizes, with its bread and butter being video conferencing.

Zoom is available in the Education, Financial Services, Government, Healthcare, Manufacturing, and retail industries. Palantir targets many of the same sectors; however, its platform is bulkier and has no actual application use for smaller enterprise businesses. Palantir’s software is generally considered expensive, with some estimates suggesting hundreds of thousands or even millions of dollars per year. Zoom offers a freemium model with tiered pricing plans, different features, and user capacities for businesses and government agencies.

A significant market opportunity ahead with an exceptional product:

Zoom saw 325.81% revenue growth in 2021 due to the pandemic. It is safe to say they will never see this type of year-to-year growth again, but it doesn’t need to.

Zoom is riding a consistent growth trend that began long before the pandemic. Work-from-home or Remote Work, whatever you want to call it, is the inevitable increased globalization of work. Fast Company coined the term “Gen Global” For Gen Z, who prefer “work from anywhere” and prioritize travel over education. Young workers grew up on social media and are more comfortable communicating via video conferencing.

Working full-time in the office is a dying trend. The new long-term trend is a form of hybrid work, from which Zoom will likely reap the rewards. As technology improves, the migration from On-Prem to the Cloud continues, and older CEOs phase out, companies will become more receptive to Zoom’s platform. Hybrid work is inevitably the future and growing; companies that resist the trend will lose out on talent, leading to a loss in profits. Zoom’s strategy to capitalize on this trend is to continue improving its platform and expanding its customer base, particularly in the government and healthcare sectors.

Zooms provides cloud-based products that the next generation of workers will use. Meetings offer a better mousetrap for workers and are becoming an essential product for employers to provide as an efficient way to communicate with each other.

It is popular among most workers who see it as a “perk.”

Reduced costs for real estate

Expanded pool of recruitable talent

Increased worker retention.

Adopted over time as hardline proponent CEOs of returning to work retire.

Fundamentals vs. Valuation:

Zoom and Palantir have been public for less than five years, so evaluating past performance based on limited data is difficult. With companies like these, it is more helpful to first zone in on the fundamentals to make an educated guess about the future.

The Artificial Intelligence Platform (AIP) is promising. I am a believer; however, the pathway is far from certain. Palantir’s commercial business is nascent, with even its most ardent supporters having to take a leap of faith that it will grow. Selling a product that companies don’t even know they need is almost impossible to map out five years out.

Palantir has a long sales cycle. Learning its solutions takes much longer because the learning curve is high. It will likely take a year before their platform shows any meaningful ROI.

AIP is intriguing and ambitious. The presentation deck is broad and alluring. It captures an investor’s attention when you help uncover human trafficking rings or battle the Russian army. I have determined the risk is worth the rewards as an investor, but valuing this as an investment is problematic because it assumes high optimism in a new space without a clear track record.

Can Palantir expand its commercial business and attract a broader and more diverse customer list? It is too early to know if the path is certain. A longer track record of low churn and increasing profits is needed to make a better determination.

Zoom’s software has already penetrated multiple enterprises, organizations, and businesses. However, its platform still has a lot of room to grow. Many analysts dismiss Zoom’s government business, which is largely untapped, more so than Palantir.

Another lockdown may not happen again, but the residual effects of the lockdown are seeing permanent work behavioral changes despite the pandemic being over:

Columbia University went fully remote due to Palestinian protests.

School districts in many U.S. cities went remote during the winter due to the flu/Covid outbreak.

Flu/Covid outbreaks will continue in the future.

Someone even had a Zoom court hearing while driving with a suspended license.

MLB’s league offices use Zoom Meetings, Zoom Rooms, Zoom Phone, and Zoom Webinar, while Zoom’s all-in-one collaboration platform is integrated across several MLB clubs, platforms, and broadcast outlets.

For a platform critics say is dying, people still use it daily. Zoom’s client list ranges from news broadcasts to hospitals, school districts, colleges, and courts. Its partnership with MLB is one of the best case studies of how Zoom’s suite of products can provide a large, multifaceted enterprise with various solutions.

The two biggest fundamental questions that I will be closely watching for the near future:

(1) Leadership execution, mainly if they can make intelligent acquisitions of smaller technology companies to complement and grow their existing businesses. Zoom has a large cash pile and will likely search for an acquisition target to grow its business.

(2) Increased sales and marketing. The CEO & Founder, Eric Yuan, acknowledged this on a previous earnings call: “One thing I think we did not do well, as I mentioned even before, is we did not do well on the marketing front. A lot of customers and users do not know Zoom has a greater presence in Team Chat functionality at no additional cost. And it works extremely well.”

Yuan has proven he can make great products, but Zoom must enter wartime sales mode. Zoom must ramp up S&M spending and sacrifice profits for growth. Zoom has a significant edge over Palantir because it has far more brand recognition. Conceptually, learning how Zoom’s products can help a business is easy. Practically, there is a low learning curve, with Meetings & Chat being extremely user-friendly. Foundry is a much more challenging platform to use and understand. Palantir would need to make Foundry less heavy to address many lukewarm and bad reviews. It’s an early and fixable problem but a potential red flag for future growth.

Both companies have potential opportunities, but Zoom has a bigger total addressable market. Despite the pandemic being over and Zoom becoming a target for other companies to criticize, Zoom’s platform is already becoming a mainstay in the enterprise ecosystem. The story is still early for its commercial and government businesses.

Low vs High Expectations and Sentiment

From a Price-to-Earnings Ratio and other traditional financial metrics, Palantir is an expensive stock. Is it overvalued? That depends on whether it can meet or exceed high expectations. Zoom is the opposite, an inexpensive stock with low expectations.

In the short term, Zoom has a low bar to jump. Analysts would view 5-10% YoY growth in 2025 as wildly optimistic and likely cause the stock price to double from today’s price. For Palantir, anything under 25%-plus overall growth would be disappointing and likely not well-received from Wall Street.

A company with high expectations can exceed them, but Zoom likely has better odds of meeting its target projections.

So why mention expectations? I discuss this to reflect the nuisance of investing and how to become a better, well-rounded investor. Suppose you are an investor and only consider the company’s qualitative aspects. That strategy probably works out in the long term, but you must ask yourself: Is there a compelling reason to buy the stock where it trades today? The better-discounted price you get, the more likely you have a higher return.

Analyst ratings for both companies are pretty tepid. Remember, Palantir traded above 35 in early 2021, and Zoom traded above 555 in 2020. Many bitter retail and institutional investors are underwater on their investments if they are still holding, but this is where the behavioral aspect of investing plays a factor. The mood of the market and macro environment was completely different during the pandemic than today.

The past is the past. An investor cannot change the price at which you bought the stock last year or five years ago. The company’s valuation is different, but if you are down 30-80% on your Zoom or Palantir shares, it doesn’t mean the company is 30-80% worse. Palantir has seen significant growth in its commercial business. Zoom is a high-quality company trading at a rare reasonable valuation with solid fundamentals. Zoom has yet to see its revenue decline, which likely would have happened if its platform was a pandemic fade. The low sentiment has manifested skepticism about the viability and feasibility of the Zoom platform. This creates a potential opportunity for patient longs who do not care about the lack of momentum. Shares for both companies are not overbought according to the relative strength indicator (RSI), a momentum-oriented technical analysis tool.

Final Thoughts:

Both of these companies have compelling evaluations. They meet the criteria for quality companies. I give the edge to Zoom because it trades more at a discount. Both companies have an opportunity because their balance sheets look healthy, and their cash flow is growing steadily.

I may seem down on Palantir, but as I said earlier, I invest in both companies. Although it looks fairly valued today, Palantir is not an overhyped AI company. I could be underestimating its fundamentals, meaning it is grossly undervalued today.

I love the fundamentals, but valuation matters. Can you ignore the possibility of an economic slowdown, a hiccup, or a U-turn in sentiment or the story’s narrative? Can you invest successfully, ignoring risk and assuming a large meteoric rise based on already-priced assumptions? I don’t have enough conviction to go all in on one name, but I do have enough of a risk appetite to stay on the ride and let it play out. Zoom’s sentiment today is low, and all the momentum it had during 2020 and 2021 seems to have evaporated. Although not dirt-cheap, Zoom appears like an inexpensive stock with better odds of overperforming.

Zoom CEO Eric Yuan (right) takes the photo opp on Zoom’s IPO day.

Zoom was a company I wanted to avoid. An app I was forced to download during the pandemic to communicate with the rest of the world. Since Cathie Wood made Zoom one of the more significant holdings in ARK Innovation ETF (ARKK), I assumed it was a hyper-growth, deeply unprofitable company with more hype than actual substance.

With the stock cratering since its pandemic day highs, I have done a deeper dive into the company and realized I may have judged this book superficially by its cover. The company is highly profitable, has no debt, and has proven it no BlueJeans, not even close. The company was built from scratch as an enterprise tool nearly a decade before the pandemic. Although its use as an app for virtual cocktail parties and meet-and-greets is declining, Its use in the business world is expanding rapidly.

Expectations for Zoom are ridiculously low for such a high-quality company. It trades at such low valuations it is screaming potential great opportunity. Many analysts have either given up or taken a wait-and-see approach. It appears there are two reasons why Wall Street is sitting on the sidelines:

Microsoft Teams will cut into Zoom’s videoconferencing software market share.

2022 was the peak for Zoom because of lockdown restrictions. It will not likely see this type of growth in a non-pandemic environment.

Analysts do not provide the specificity and context for why Zoom will lose its market share. Analysts assume Teams, Google Meet, and other big-name players will continue to erode Zoom’s 55% market share lead in video conferencing. Even if losing market share is inevitable, Zoom will remain an entrenched leader. The TAM for this market keeps accelerating and evolving, with hybrid work models now a permanent fixture.

The video and audio communication market alone is big enough for multiple winners. It isn’t a winner-take-all scenario. Zoom doesn’t have to be the leader to succeed, just one of the leaders. Audio and video communication in the enterprise sector was saturated before Zoom was founded. More likely, the industry is still growing and evolving with increasing AI adaption and innovation velocity. Even better, Zoom has less than a 6% market share in the overall office-suites market. Google Workspace is the dominant player in the market, providing Zoom and its suite of products an opportunity for solid growth over the next decade.

Zoom’s Edge over Microsoft and Google:

At its core, it is an artificial intelligence company. Its rapid implementation of AI into its products is slowly helping it create a powerful network effect for its enterprise business. They have built from the ground up and patented their cloud-based technology stack instead of being based on decade-old code trying to fit it into new technology; Zoom is a pure cloud-based platform based on Amazon’s AWS and Microsoft’s Azure servers. Its best-in-class products provide users with superior video & sound quality and overall better user-end experience. Zoom has a significant advantage over smaller players who do not have the capital or resources to bring a competitive product onto the market.

Regarding reliability and quality, Zoom ranks highly because of its premium technology stack infrastructure. Zoom’s growing patent portfolio shields itself from Microsoft or Google stealing or copying their products. Zoom holds patents in videotelephony, voice-over IP (VoIP), and AI-driven technology. These patents give Zoom a premium evaluation in the case of being acquired. These fundamental qualities are a hidden secret weapon that you cannot see on the company balance sheet or just based on the numbers.

Zoom’s technology and products integrate seamlessly with other applications like Salesforce, Slack, and Dropbox. Once integrated into the enterprise connective tissue, this creates a situation where the product becomes too costly and time-consuming to remove, creating a powerful network effect. Enterprise customers typically use several third-party application vendors, depending on their use case. Some customers want all their applications to be Microsoft products, which is atypical of how the enterprise ecosystem typically works. Most clients do not want to be completely locked into the Microsoft Office 365 ecosystem or have Microsoft as their sole vendor. As long as the multiple applications flow cohesively within the enterprise workstream, many companies will hesitate to go all-in on Microsoft.

Aside from having the best product, Zoom is pouching away key-level executives from Microsoft. Zoom’s Chief Product Officer, Strategy Officer, Development Officer, and Technology Officer bring over 84 years of experience from Microsoft! Overall, the leadership team is seasoned and well-rounded, many coming from Webex/Cisco. This team is a potential dream team in the making. The company is led by the founder and CEO, Eric Yuan, who is intensely focused and visionary. The leadership team understands the enterprise market and rapid product rollout, with a long-term plan to execute a go-to-market (GTM) strategy. They have already passed a real-time stress test during the pandemic, essentially repairing and upgrading a plane while in the air. Management passed with flying colors.

One of the biggest compliments of Zoom came from the CEO of Upstart, Dave Girourad, a former product manager at Apple and President of Google’s Enterprise division. In an interview with the Motley Fool last year, Girourad gave high praise about the team at Zoom:

Obviously you don’t want to act in fear, I’m one who has not historically done a lot of singular stock picking. I do it occasionally, but I usually will not do a lot of that myself. But occasionally I just have conviction and I have conviction through experience in seeing a product, and I will just give you an example. I put a big chunk of money recently, the first time I bought a singular stock in a long into Zoom. I was I know that business, we’re trying to build products like that at Google. I know how hard it is. That company executed incredibly well when suddenly their business just went through the roof in early 2020, and I had just so much respect for what they’ve done, and I know how hard the problem is to solve. How many times has like doing video like this has been just a nightmare in the past despite the fact that Microsoft’s coming after them, Google’s coming after them whoever else.

High praise from a highly credible executive in this industry. I value his opinion and personal experience much more than most Wall Street analysts.

Zoom Notes offers a robust editor with extensive formatting options like font, styling, bullets, colors, and more.

Technology stack advantage, quality of products, and execution by management will be the winning formula for Zoom. As we see rapid and intensive AI integration, this will likely force companies to take on higher expenses in multiple industries. Typically, the CIO or CTO decides to take on Zoom as a vendor vs the legacy apps. Video conferencing tools will be viewed as more of a need than a want. Taking on Microsoft Teams simply because it is free or provides several features businesses rarely use won’t be good enough. Is it intuitively running better for clients of Teams after collecting their data and information? Is the Teams platform increasing productivity? I and many others argue it underdelivers.

Imagine if Zoom automatically takes notes or creates an action plan during a meeting. It has already launched these products, and the higher costs associated with superior AI-implemented products will be worth it if they can unlock significant cost savings in the long run or significantly boost meeting productivity and collaboration. Zoom is winning the popular vote as its tools and applications are viewed as more intuitive and user-friendly than Teams. This will become more noticeable as technology improves.

From a valuation standpoint, ZM stock is trading at dirt-cheap levels. You have to ask, will Microsoft grow faster than Zoom? Which is more likely? One has a market cap of around 22 billion, and the other almost 2.8 trillion. Even if Zoom doesn’t achieve Ark’s $1,500 share price projection by 2026, the stock will likely be a big-time winner, even if management meets baseline expectations. Today, the stock is undervalued based on most financial metrics:

ZM Price to Sales ratio: 4.92 MSFT Price to Sales ratio: 12.81

An investor in Microsoft is paying a premium for a superb business. Expectations are sky-high, and they must deliver great numbers to maintain their high valuation. Is it possible? Absolutely. Is it more likely than Zoom, trading at low valuations and expectations, to outperform Microsoft? The probabilities appear to favor Zoom. These are the types of questions investors should be asking. I started a position in Zoom, hoping that not only is it undervalued but also misunderstood, with the growth story still early.

I see an investment in Zoom similar to that of Moderna. Two companies that multiplied during the pandemic for areas not of their original focus – Moderna developing cancer treatment and Zoom acquiring B2B customers. The narrative has shifted quite a bit for both companies as they have grown significantly from their start. Although the headlines read companies struggling to adapt in the post-pandemic world, they are fundamentally strong. Zoom may have received an artificial/temporary boost from consumers downloading the app for reasons outside of enterprise; what isn’t artificial is the increased brand awareness, obtaining verb status (zoom, tweet, google, Airbnb), and cash windfall, which can be invested in the overall business to further separate itself from Skype, FaceTime, and Google Hangout.

A glimpse of the future: Zoom changed how the world communicated from Zoom yoga sessions, weddings, and funerals. The transformation of workplace communication is still evolving.

Pros of Zoom as an investment:

Exceptional and best-in-class product offerings.

Impressive technology foundation and patent list.

Founder-led company that shined bright during a global emergency.

The beginning of a new intuitive human work communication system?

Risk factors:

A lot of execution risk and pressure.

The best product does not always win.

There is insufficient data to show that Zoom customers will keep them long-term and pay higher prices instead of switching to a less expensive platform.

The stock is inexpensive. That reason alone does not indicate future growth will be impressive despite lowered expectations. A short-term bounce back or recovery is possible, maybe even probable, but a sustained price increase will require consistent growth.