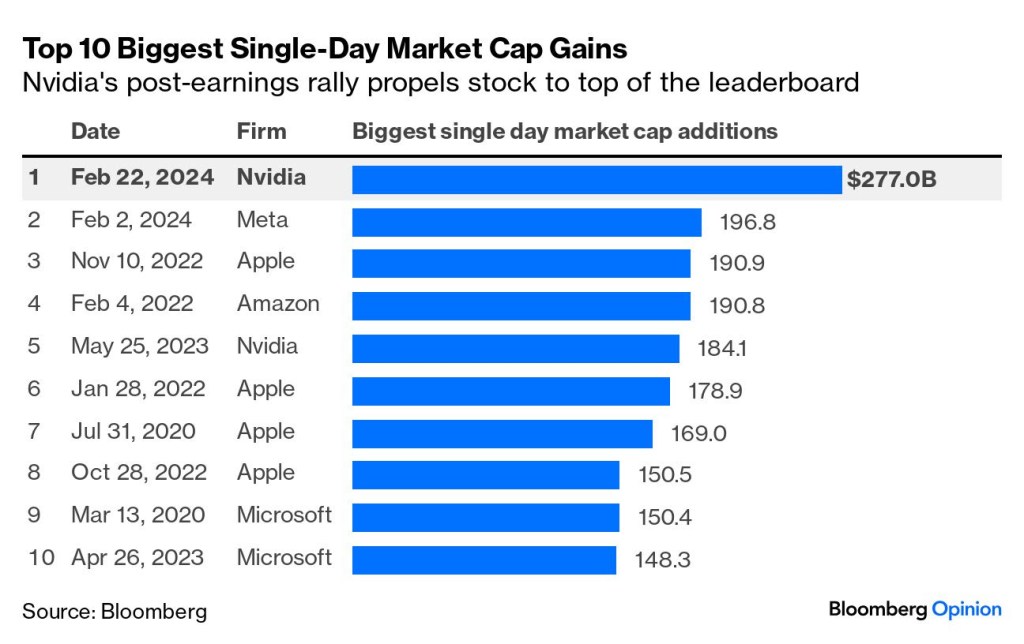

Nvidia has gotten toppy recently.

Nvidia has demonstrated an impressive growth trajectory, surging nearly 2,200% from $6 to briefly touching $140 in under five years. This meteoric rise even saw it surpass Microsoft as the most valuable stock in the market for a brief period.

Long-term investors, your perseverance and discipline have paid off. You’ve demonstrated two of the most crucial traits of successful investing: patience and discipline. While many struggle to hold a stock for even a year, you’ve shown the strength to hold on for much longer. This is an achievement worth celebrating.

The stock has made parabolic gains, but based on logic, rationality, and sound judgment, it’s time for long-time investors to cash out at least a small portion of your paper gains.

Nvidia is a fantastic company with A+ growth, leadership, and profitability. However, it is not immune to the macro economy, slowing demand, or a change in momentum/sentiment, which will inevitably happen.

As share prices rise, predictably, people with full-blown FOMO are joining the bandwagon late to the party. During this AI fever, consideration for valuation and rationality is put on the back burner as “dumb money” enters the market.

The people buying Nvidia stock now are momentum traders or dumb retail money. They admittedly have no idea what they are doing and are paying a premium for a very aggressive future outlook.

When I refer to ‘dumb money, ‘I’m not implying that these investors are unintelligent. It’s a term used to describe those who enter the market without a clear understanding of the investment they’re making, much like a dog chasing a car.

Here is a question from Linda in Illinois on a recent episode of Mad Money with Jim Cramer:

“I’m a retired postal employee who worked for 45 years. I have no financial investment knowledge. I wanted to know how to buy stocks, and I wanted to ask you if I should try to invest my Thrift Savings Plan (TSP) money in S&P Index Funds, or Magnificant 7, or Nvidia or all Nvidia.”

Or these types of posts on Reddit:

Think about the person in your family or at work who exhibits terrible financial acumen. The last person in the world you would want to take financial advice from.

The people considering buying Nvidia stock may have just learned about the company this year. They still may not even know what they do. If you’ve never heard of the company before last year, what happens if the stock craters? History shows people will justify their fears of a recession or market crash by selling at a deep discount and retreating into cash or gold.

This is perfectly normal animal behavior. But you are neither a dog nor a cat!

Again, Nvidia is a fantastic company—a best-in-breed company. But every company has a numerical valuation. With a straight face, can you say out loud that Nvidia will be a $10 trillion company by 2030? If you chase high growth, you typically pay a premium price for it and will likely underperform the market in the long run.

The risk-reward profile of buying Nvidia today significantly differs from a year ago. This may sound hard to believe, but shares are less valuable today because the valuation is far more uncertain than last year.

How many companies have gone from $3 trillion to $8-10 Trillion? Answer: None. Saying this happens with a level of certainty or confidence seems misplaced. It also ignores the risk of things going wrong. We are in uncharted waters with no precedent.

Recently, the Lakers hired former player and current podcaster/ESPN analyst JJ Redick as their new head coach. Redick is the same age as LeBron James. He also has no coaching experience beyond youth basketball. Yes, you have read that correctly—a professional basketball team has hired a coach who has not even coached middle schoolers!

There is nothing wrong with being optimistic about Redick as a coach, but how can anyone be confident that he will succeed when he has never done it before? Of course, Redick could be the next Pat Riley or Phil Jackson; it could happen, just like Nvidia can continue skyrocketing. Valuation is an imprecise art because the future is unpredictable. But can you say with confidence this is probable or more possible?

Let me summarize my gameplan:

Am I saying to go all-in cash or to sell out of everything tomorrow?

No.

There is no need to think so dramatically or immaturely.

Betting against Nvidia is extremely risky.

Putting fresh money into Nvidia is risky because investing is more than just about data points and figures. Investing has far more intangibles, making it both an art and a science.

The safe time to buy Nvidia was the second half of 2022 when the US government banned them from selling chips to China and Russia.

I will ride Nvidia long-term, but the growth path is not guaranteed or linear. Past performance is no guarantee of future results.

Jennifer Lopez’s It’s My Party tour grossed $54.5 million with 31 shows in 2019. She recently canceled her tour. The same is true for the Black Keys, while other stars like Pink and Justin Timberlake (pre-DWI) have canceled some tour dates.

Meanwhile, Olivia Rodrigo’s “Guts” tour tickets go for above $570 on the resale market. In 2019, Rodrigo was a relatively unknown 15-year-old.

There is nuance and context to life and investing.

As a long-term investor in Nvidia, I am strategically preparing my portfolio by gradually increasing my cash holdings during periods of strength. This approach allows me to prepare for potential market downturns while benefiting from the company’s growth.

Nvidia is undoubtedly a great company, but why pay premium prices for future assumptions? I am building my cash position not out of fear but of a rational understanding that market fluctuations are normal. This way, I am prepared to take advantage of more appealing risk-reward profiles in the future.

It’s a win-win situation. Hold most of your holdings and reap the reward if the companies perform well. Trim your position in small incremental amounts to build cash. If bad things happen in the market, you at least have more cash to take advantage of a more appealing risk-reward profile in either a cheaper Nvidia stock or another company with a better runway for growth.

The law of big numbers says Nvidia will not hit $10 trillion by 2030. We have never seen a $3 Trillion company triple in 5 years. I am a contrarian, but even that sounds like a stretch. There are compelling companies that can go from $1-10 billion to $10-$100 billion, which is more plausible and we have witnessed several times.

There is nothing wrong with using nuance and rationality in investing. Take some money off the table, even just a tiny amount.

That’s how you, as an investor, need to think. Buy stocks when the valuation becomes desirable. To buy stocks when they are desirable, you need cash on hand, which is best built during days like today. What better time to raise money when your initial investment has increased 10x or more?

Preparing for the future by slowly building a cash position is sound investing advice because the market will eventually experience an inevitable downturn, and prices will fall. When risk falls, that would be a more appropriate time to pounce (use that animal instinct) and buy more aggressively.

Great investing requires a solid strategy and not just emulating pure emotional instinct. Don’t be the dog chasing a car.