Aritzia’s Q3 FY2026 was one of its best quarters ever—like a walk-off home run in the playoffs. For the first time in the company’s history, they crossed the CAD 1 billion revenue mark in a single quarter, hitting CAD 1.04 billion, up 42.8% YoY.

Aritzia grew sales by nearly 43% while increasing inventory by only 10%. This means their inventory turnover is accelerating and they’re selling clothes almost as fast as they can get them off the trucks. This leads to fewer markdowns and higher full-price selling, which is exactly why their gross profit margin expanded by 30 basis points to 46% this quarter. This 4.3x “Sales-to-Inventory” growth ratio suggests an operational efficiency that makes even the “Mag Seven” look sluggish.

Compare that to Lululemon: Their inventory grew by 11%, but revenue only grew by 7%. When inventory outpaces sales, it usually leads to one thing: markdowns. In fact, Lululemon’s Q3 earnings call explicitly noted that gross margins were squeezed by higher markdowns (up 90 basis points) and tariff impacts. They have ~$2 billion in yoga pants and gear sitting in warehouses that they’re struggling to move at full price.

Aritzia is actually running a more efficient operation relative to its growth than even Nvidia right now. Here’s a quick side-by-side:

Company

Sales Growth (YoY)

Inventory Growth (YoY)

Ratio (Sales/Inventory Growth)

Aritzia

42.8%

10%

~4.3x

Nvidia

62%

~32% (9M cumulative)

~1.9x

Lululemon

7%

11%

<1x

Aritzia’s ability to scale this aggressively while staying so disciplined on inventory is retail execution at its finest, turning hype into real, high-margin momentum. If you’re looking at consumer discretionary winners in this environment, Aritzia is flexing harder than most realize.

This quarter also saw the late-October launch of the Aritzia Mobile App, which hit 1.4 million downloads and became the #1 shopping app in North America on day one. E-commerce revenue surged 58.2%, proving that “Everyday Luxury” translates perfectly to a high-frequency digital experience.

In 2027, Aritzia isn’t just signing a lease; they’re opening a new 40,000 square foot flagship store of the former Nordstrom footprint in Vancouver’s CF Pacific Centre. Aritzia is officially planting its flag on the grave of the defeated old guard.

This is the coronation of a new king. It marks the definitive shift from the bloated, “everything-for-everyone” department store model to a new, aggressive power dynamic. Aritzia has engineered a psychological moat known as “Everyday Luxury.” This isn’t just fashion; it’s a socioeconomic pivot that captures the soul of the modern consumer:

High-End Design: The clothes look like they belong on a Paris runway (minimalist, high-quality fabrics, tailored fits).

Attainable Pricing: Because they control the supply chain, they can sell that “look” for $150–$400 instead of $2,000. By pricing themselves 30–40% below heritage luxury (The Row, Celine) but 20–30% above fast fashion (Zara, H&M), they’ve created a “sweet spot” of attainable exclusivity.

The Result: They’ve captured the “HENRY” (High Earner, Not Rich Yet) demographic. This group is remarkably resilient to macro downturns because they view Aritzia as a “reasonable” yet “necessary” indulgence rather than an extravagant splurge.

The Psychology: Since “big” milestones (real estate, stable pensions) are increasingly out of reach for many, the HENRY demographic is reallocating their discretionary cash into “micro-luxuries” that provide immediate status and emotional ROI.

As we are witnessing with Saks, the “department store” represents the old middle class: a place where you go to see a little bit of everything. It’s a dying generalist model in a world that’s increasingly specialized.

The Old Way: Middle class = Access to variety.

The New Way: Middle class = Access to a vibe. Aritzia doesn’t just sell clothes; it sells a lifestyle aesthetic. When you walk into their “Super Flagships,” you aren’t shopping; you’re participating in a brand-curated experience.

The stock is trading at record highs with a P/E that reflects “perfection.” But Aritzia is just hitting its stride. They’ve successfully moved beyond “leggings and hoodies” into a full-wardrobe solution. It isn’t just superb execution by management; it’s capturing the vibe of today’s consumer.

I bought the stock as a small position in 2023 and have held it and will continue to hold it. If we’re using a baseball analogy, we are still very early. For Aritzia’s growth, we haven’t even entered the 7th inning stretch. Aritzia currently has roughly 72 boutiques in the US (out of 139 total). For context, Lululemon has about 374 stores in the US. Aritzia’s stated goal is ~150 boutiques total by 2027, with long-term potential for 180- 200+ overall, focusing heavily on US expansion (8-10 new boutiques annually, mostly in the US). If Aritzia hits its 150-store near-term target, revenue will likely triple as brand awareness hits a tipping point.

I am officially pegging Aritzia as a stock to buy during a market correction or pullback. Unlike legacy retailers, Aritzia is currently expanding its US footprint into a demographic that views “Everyday Luxury” as a non-negotiable part of their personal identity. This psychological moat, combined with an operational efficiency that is scaling faster than its infrastructure costs, makes Aritzia uniquely qualified to weather consumer weakness better than almost any peer in the sector.

If the market gives me a discount on this level of execution, I’ll take it.

Revolve Group (NYSE: RVLV) is the forgotten champion of apparel retail. While Wall Street obsesses over hyper-growth names and retail investors chase the next meme stock, Revolve quietly operates one of the strongest, most defensible business models in the entire consumer sector. It’s dismissed as “just another overpriced clothing seller,” but that superficial take misses two genuine superpowers that are extraordinarily rare in the apparel sector. This unique combination creates a company that is antifragile in a brutal, cyclical, low-margin industry, a combination that deserves far more attention than it gets.

Superpower #1: A Pristine, Fortress-Like Balance Sheet

Revolve has more cash and cash equivalents than total liabilities. This isn’t total assets minus liabilities. This is cash-on-hand exceeding all debt. As of September 30, 2025, Revolve held $315 million in cash, with total liabilities of just $226, leaving it net cash positive by nearly $90 million. (Revolve Group Announces Third Quarter 2025 Financial Results, 2025) In an industry notorious for leverage-fueled boom-and-bust cycles, this is almost unheard of. Look at Revolve’s closest competitors and legacy apparel names:

The RealReal → Negative net cash, drowning in $500+ million of debt

Victoria’s Secret → $4 billion in long-term debt, with cash covering only a fraction.

Guess? → Leveraged with debt-to-equity over 2x

Macy’s, Kohl’s, Abercrombie in their prior incarnations → Perpetual debt refinancings amid endless store closures

Most apparel retailers use leverage as oxygen. Revolve doesn’t need it. Zero net debt (actually net cash) gives them a massive margin of safety that investors in this sector are simply not accustomed to. In a downturn, Revolve can keep the lights on indefinitely without ever visiting a bank. In an upturn, they can aggressively buy back stock (they’ve already repurchased over 20% of shares outstanding since their 2019 IPO, including $100 million authorized in 2023), or acquire distressed brands/competitors for pennies on the dollar. Having such a fortress balance sheet creates real optionality.

Superpower #2: Consistently Elite Gross Margins (54% and Climbing)

The average apparel retailer scrapes by with gross margins of 30-50%. Revolve delivered a 54.6% gross margin in Q3 2025 (up 350 basis points YoY) and has maintained a 50-55% gross margin range for years. For context:

Louis Vuitton (LVMH) → 66%

Lululemon → 59%

Zara → 55-57%

Most everyone else → 30-45%

Revolve is operating at the same rarefied level as the very best branded apparel players on earth, despite being a pure-play online retailer without a physical-store crutch. Why does this matter so much? Because elite margins are Revolve’s ultimate defense against Amazon. Retail investors see “expensive clothes” and assume the model is fragile. In reality, those premium prices are the moat. Millennials and Gen Z raised on Instagram and TikTok aren’t shopping for the cheapest white t-shirt: they’re buying an identity, or an outfit that photographs well at Coachella. Revolve sells social currency. Customers happily pay 2–3 times more for the outfit that might cost less elsewhere because they’re paying for curation, discovery, and status. That willingness to pay a premium is exactly what produces 54%+ gross margins and sustains an average order value of $306 in Q3 2025 (up 1% YoY).

And those margins are what keep Amazon at bay. Amazon dominates commodity fashion: fast, cheap, endless selection. If Revolve ever tried to compete on price, Amazon would crush them with its scale and logistics. But Revolve isn’t playing that game. They’re playing the art of the brand premium game, something Amazon isn’t going to win. Even after 25+ years and billions invested, Amazon has failed to crack premium or luxury fashion in any meaningful way, with a fashion gross margin hovering around 20-30%, far below the industry standard. Jeff Bezos himself has admitted that building a real fashion brand is one of the few things Amazon hasn’t figured out.

The Rare Combination

Put the two superpowers together, and you get something compelling:

A net-cash balance sheet → survives any storm, buys back stock aggressively, and is opportunistic with M&A.

54%+ gross margins → funds growth, defends against Amazon, produces torrents of free cash flow (up $265% YoY to $59 million in the first nine months of 2025.

This defensive balance sheet and offensive margin profile is the definition of antifragile in retail.

Revolve is clearly doing something different: one that builds on digital and social infrastructure to erect a curation and brand moat. They sell the Revolve experience, which allows them to charge premium, full-price prices (high Average Order Value). Using first principles, Revolve’s main product isn’t a dress; it’s the marketing expense. The influencer trip is not just a cost; it is the intangible asset that allows them to maintain a $300 price point for a dress. This experiential luxury marketing, powered by a network of 5,000+ influencers, has driven its owned-brand penetration to 35% of sales, further boosting margins.

The focus on experiential luxury marketing allows Revolve to build a digital model while using temporary pop-ups as low-CapEx market research before committing to a permanent location. Their Aspen pop-up in December 2024 converted to a full flagship in June 2025 after crushing performance metrics, and they’re replicating the playbook with a permanent store at LA’s The Grove. Focusing on brand experience, margins, and building a cash fortress creates optionality, which is a much different playbook than most apparel retailers play: heavy CapEx expansion to drive growth, which is more inflexible and likely requires leverage.

Very few companies in any industry possess both traits simultaneously. When you find one, especially one trading at a reasonable earnings multiple with a proven ability to grow, it’s worth paying attention. Revolve isn’t a “hot” stock. It doesn’t have 150% YoY growth. It is a quiet, compounding machine built on genuine structural advantages, like a pristine balance sheet and 54% margins that the market keeps overlooking.

In 2016, I invested in Tapestry (TPR), betting on Coach as an undervalued brand poised for a turnaround. It was one of the first stocks I bought as a new investor. My thesis was straightforward: the stock could reclaim its March 2012 peak of $79.70. Nearly a decade later, my prediction proved correct, though the road was far from smooth.

Tapestry faced significant challenges, including the 2019 ousting of its CEO, the 2020 resignation of another due to ‘personal misconduct,’ and a 2024 court ruling blocking its merger with Capri Holdings. Yet, TPR has outperformed the likes of LVMH, Lululemon (LULU), Capri Holdings (CPRI), and Nike (NKE) over the past five years—the very stocks I eyed when TPR struggled. Those same peers now sit well below their prior peaks.

I acknowledge luck played a role. Had the Capri merger proceeded, TPR would likely be trading in the $50–$70 range today, far below its current levels. Now, with TPR soaring past its 2012 high, I’ve shifted my strategy and trimmed my position to lock in long-term gains. If the stock continues to climb, I’ll likely reduce my holdings further.

My original thesis—that Coach was trading at a bargain—no longer holds. In a tough luxury market, Coach has unexpectedly gained pricing power for a mid-tier brand, fueled by a reshaped brand narrative and the TikTok-driven success of its Tabby Bag. However, Kate Spade, accounting for about 15% of revenue, remains a weak link due to inconsistent branding and declining sales, tempering my optimism.

Management deserves credit for Coach’s turnaround, but I remain cautious. Tapestry’s cyclical nature ties its success directly to consumer spending and economic conditions. A weakening economy would likely pressure sales.

Tapestry’s acquisition strategy is my primary concern. Selling the unprofitable Stuart Weitzman brand was a smart move, but the pursuit of the Capri merger suggests management may doubt Coach’s standalone growth potential. Given the lackluster outcomes of the Stuart Weitzman and Kate Spade acquisitions, future M&A activity could increase debt and strain cash flow.

My suggestion? If Tapestry is set on acquisitions, it should issue new shares to fund a targeted purchase, such as a niche luxury brand with strong growth potential. This approach would preserve cash and avoid debt, though it risks diluting existing shareholders. It could create more long-term value than increasing the dividend or buying back stock to where it’s trading currently—an action that offers limited upside if the stock corrects.

While I’ve enjoyed reinvesting dividends during the stock’s recent climb, weaker economic indicators, like declining retail sales, suggest uncertainty ahead. Most companies in the consumer cyclical sector face headwinds from slowing spending, and TPR is no exception.

That said, TPR isn’t wildly overvalued. With an upcoming earnings report and Investor Day looming in September, short-term upside potential remains. I’m cautiously optimistic and will monitor these events. My goal is to sell more shares at a higher price before the end of the year.

Palantir redefined data analytics, while Gangnam Style redefined K-pop. Both achieved unexpected success through unconventional approaches, capitalizing on the right timing, transformative momentum, and cultural context.

Palantir, whose stock has surged over 400% in the past year, has become a focal point in the AI movement, despite its 20-year history. Similarly, Psy was already a veteran artist in South Korea, having started his career in 1999, 13 years before the global phenomenon’ Gangnam Style’ was released in 2012. The video eventually became the first on YouTube to reach one billion views.

Both share the same superpower: unorthodoxy, which helps them stand out in a competitive field. Palantir has unexpectedly fueled the spirit of AI-driven operations, just as Gangnam Style helped usher in K-pop on a global level. Alex Karp, an unconventional CEO, and Psy, the highly unconventional K-pop artist, embody this spirit of unorthodoxy.

Grappling with Valuation:

As a Palantir shareholder, am I saying this is the “peak” for the company? I don’t know. It seemed things were getting frothy when Palantir surpassed Lockheed Martin’s market cap; now it has a larger market cap than Lockheed Martin, Boeing, and Snowflake combined.

From a price-to-earnings or even price-to-sales ratio perspective, Palantir makes zero sense. While a projected growth rate of 36% is impressive, it falls short of what Zoom Communications achieved during the pandemic or what Nvidia has accomplished over the past three years.

It’s very possible that Palantir’s growth may have already peaked or is nearing its peak. I have little doubt, though, that the company has a long and successful future. However, I am highly uncertain if Palantir can grow enough to meet its sky-high valuation. Any signs of slowing growth could lead to a steep retracement. Any broader market correction or shift in sentiment could lead to a significant decline.

Even though I’m tempted to trim and sell more (if not all) of my shares every time the stock rises, it’s difficult to fight against momentum. Palantir is a profitable free cash flow machine, and its commercial business is in an early growth phase. The story remains compelling. There is little wrong with the actual fundamentals of the company; the focus of late has been predominantly on valuation metrics.

Lessons from Psy:

What Gangnam Style can teach us about Palantir is that a valuation doesn’t have to make sense to justify itself to keep rising. Momentum and narrative transcend numbers (even though Palantir’s numbers are solid).

As T-Pain said, words cannot describe how amazing the music video for Gangnam Style is. The video itself doesn’t make much sense, yet it has dominated globally:

This is an almost Dada-esque series of vignettes that make no sense at all to most Western eyes. Psy spits in the air while a child breakdances, sings to horses, strolls through a hurricane that shoots whipped cream in his face, there’s explosions, a disco bus, he rides a merry-go-round, dances on boats, beaches, in car parks and in elevators and generally makes you wonder if you have accidentally taken someone else’s medication.

I believe the numbers cannot fully capture the actual value of Palantir as a business. My brain struggles to grasp its market cap, and a voice within me says, “This is as good as it will get.” My heart tells me this growth story has a lot more breadth. It has the potential for a longer runway compared to unprofitable companies like Snowflake, CrowdStrike, and Cloudflare.

Perhaps this narrative about Palantir being grossly overvalued could be right and wrong at the same time. In the short term, Palantir is due for an inevitable and painful correction, but proves itself not as a ‘hype meme growth AI stock’ but more akin to a ServiceNow or Microsoft, where they are early in their business lifecycle and maintain a robust growth rate for an extended period.

Palantir’s story shows that powerful momentum can outpace solid fundamentals for a long time. Like Psy’s viral hit, its valuation may defy logic, but that doesn’t mean you sell the whole position. Stay disciplined: believe in the vision, but prepare for volatility.

Reflecting on my own experience, the seismic movement in Palantir’s stock price YTD led me to sell my original cost-basis two years ago. This decision was not made lightly; it seemed reckless not to convert some gains into actual profits.

A few thoughts:

Investing isn’t an exact science. A good story stock with solid fundamentals can sometimes have wild meteoric rises. The talent scouts who discovered Taylor Swift as a teenager probably couldn’t foresee what she would become today. Scouts watching Aaron Judge hit at Fresno State probably did not forecast his ability to hit over 50 home runs and bat over .300 an entire season. Companies can far exceed even the rosiest of expectations because a. the stock market isn’t static, and b. catalysts that propel a stock upward are not visible on a balance sheet.

Palantir has solid fundmantels. Although the upward volatility is similar, it isn’t a “meme” stock in the same vein as Gamestop or AMC. Long-term investors should consider this an investment, not a trade.

The stock is riding on euphoria in the short term, and traders are piling in on the AI wave. Even institutions or “smart money” ignore valuation and are piling in to catch up on AI. There is no way to predict how long this roller coaster ride up will last, but sentiment and “vibes” are variable factors. As good as a company’s fundamentals are, Palantir is punching well above its weight class by almost every financial metric, which creates a situation in 2025 where the actual earnings results won’t justify the current stock price. Investors buying the stock at these prices could be severely disappointed 6-12 months from now with demanding Year-Over-Year comparisons.

Palantir’s market cap has surpassed Lockheed Martin’s (if you are reading this now, it could have doubled), which indicates an overextended stock. Based on revenue and net income, the stock is overvalued today.

Why won’t I liquidate my entire position and try to buy back at a better price? I have a much more long-term mindset and believe Palantir will eventually grow into its valuation. I am willing to ride the inevitable wave downwards but concede that at least some profits need to be taken to build a more significant cash position for the potential of a better buying opportunity in the future.

Company

Q3 Revenue 2024

Net income

Adjusted EPS (USD)

Palantir

726 million

143.52 million

0.10

Lockheed Martin

17.1 billion

1.62 billion

6.80

Looking at the bigger picture:

High stock prices can lead to wildly optimistic, unrealistic expectations where investors do not consider things going wrong.

Cash is the lifeblood of any portfolio. Trying to build a cash position during a downturn is often a reactionary emotional response and not ideal. It’s crucial to maintain a balanced portfolio with a healthy cash position.

Cashing in on 500-1,000% long-term gains can seem like a victory, but I urge investors to be careful. Palantir’s focus on emerging technologies like AI and data analytics positions itself well for future growth. Anyone investing in this company should have patience (which most investors do not have) and a high-risk tolerance. It is overvalued, but the commercial business and AIP are in their infancy. As an investor, Palantir is a rare diamond. It is too valuable to avoid having this cash-compounding multiplier in your portfolio. At the same time, by not selling at least some gains, if the stock were to pull back significantly, it would be as if this rally and your paper gains never happened.

This rapid move-up reminds me of Nvidia from 2016 to 2018. Even for the best-performing company in the world, investors were given windows of opportunity to buy back in at more reasonable valuations later on. I am confident we will have similar retracements with Palantir.

Revolve Group:

The biggest position in my portfolio from a total cost basis, I am optimistic about where Revole is headed in 2025. My stance on the fundamentals of Revolve has remained the same:

It’s not a homerun investment but a solid double

There is no single catalyst to propel exponential growth, and there are no glaring red flags or company-specific risks that would cause me to panic.

Guided by two co-founders with an entrepreneurial vision, no debt, a history of profitability, and a proven business model.

I remain patient because the growth strategy remains intact. Revolve’s biggest competitors are Nordstrom and Macy, legacy companies with the same problem: an inability to attract a Millenial and Gen Z audience. For a luxury department store, this is an existential looming threat.

Big Department store chains have become stale and lack the nimbleness to pivot their business models. Macy’s and Nordstrom likely need to leave the public markets to stay afloat, which is an excellent opportunity for Revolve. While most department stores need to downsize their retail footprint, Revolve’s brand is growing, and its presence in physical retail is just starting.

Some investors may feel this growth story is not appetizing enough, but I see a clear and easy opportunity. Among its e-commerce peers, it’s one of the few growing and GAAP profitable. Revolve isn’t trying to reinvent the wheel, like becoming “The Uber of the Skies” or “Revolutionizing Fitness.” Doing something never done before in investing comes with a higher reward but much more risk. The history of profitability gives me enough assurance to bet that Revolve will be a steadily growing winner.

I am cautiously optimistic. Many analysts are sleeping on Revolve, a small market cap company, becoming an emerging brand set for impressive results in the next decade. Their legacy competitors are in apparent crisis mode. At the same time, most of their e-commerce peers in the luxury industry lack the same financial and brand strength.

Devon Energy:

A position I started recently, Devon Energy, provides great diversity for investors looking to add value and non-tech growth to their portfolio. Oil and gas are highly cyclical commodities, but investors shouldn’t confuse cyclicality with speculation. The price of oil constantly fluctuates. Although oil stocks are sensitive to macroeconomics and geopolitics, Devon is among the best companies in the oil industry.

Reduction of expenses and increase in efficiencies from the Matterhorn Express & Blackcomb Pipeline.

Increase of oil production from the Grayson Mill Energy acquisition.

Dirt-cheap valuation with a strong balance sheet and consistent cash flow.

A company aggressively buys back its stock when said stock is deeply undervalued

An attractive variable dividend that allows investors to be long-term patient.

A “green light” from the Trump administration (less regulation and taxes) that Devon could benefit from significantly.

Companies in the energy sector aren’t every investor’s cup of tea, but building a robust portfolio requires some diversification and value. Although having an asset’s value strongly correlated to oil price may seem risky, investors should consider this a hedging investment rather than just a hedging tool.

I am not a big fan of derivatives or “buying insurance” in your portfolio other than cash. But if you are overweight tech, having an asset that can move up, even with rising interest rates, is quite enticing. Also, suppose you have positions for which you have a deep conviction that you would rather not sell in your portfolio. In that case, Devon Energy can be a great addition to your portfolio because it generates income and will likely rebound when oil prices fluctuate higher. From a long-term viewpoint, the price of crude Oil WTI today is neither high (140.00 in June 2008) nor low (18.84 in April 2020). It could be a good time to start a position in Devon Energy or other oil/natural gas energy companies, with their value being fair-to-good in the near short term.

Pfizer/Moderna:

Every investor has to prepare for the inevitable “truths” that will impact their portfolio: Recessions, pandemics, natural disasters, and geopolitical events are unavoidable and will happen again. Investors must stay disciplined during volatility and take preventive rather than reactionary measures before catalyst events happen. The latest information regarding H5N1 is quite alarming.

My current goal is not to put new money into something already expensive and hope it becomes even more expensive. A long-term investor needs a strategy that fits their goals instead of following a trading strategy and succumbing to behavioral biases of only buying stocks when they go up.

While the market is overweight in AI, I have been building and diversifying my portfolio over the past year by adding energy and biotech.

Pfizer is a more established biotech company that has made a big bet on oncology (cancer). Although the transition has been slow, I expect meaningful breakthroughs with cancer drugs in the next five years.

Moderna carries much higher risk and more significant potential rewards. Its focus isn’t on a specific drug approval but on utilizing AI and mRNA technology to create a “bioplatform.” If it succeeds, Moderna has the potential to unlock the holy grail for pharmaceutical drug companies. Vaccines and drugs that do not have patent expirations (assuming Moderna owns the mRNA vaccine intellectual property). A lot of this comes with unknowns and “ifs” with this bull thesis; however, we already know through data and science that mRNA technology works, and the reward is high (essentially a potential 100x payoff) with probabilities much higher than lottery odds.

Quick hits:

Hims & Her Health—I cannot fully grasp what will give Hims a long-term competitive advantage beyond branding and slick marketing. A brand’s impact on purchasing behavior in apparel works quite differently in telehealth. Your friends and social circle may care what and where you buy your clothes from; I don’t think it matters much with weight-loss drugs and erection pills. I am not bearish on Hims; just unsure how sticky brand loyalty will work in a B2C subscription telehealth platform.

Lemonade—Too early to sell. Investors should wait until Lemonade fully launches its car insurance product nationwide. Unlike most companies I write about, Lemonade has never been profitable. It will stay that way for the foreseeable future. It will remain a small position in my portfolio, but the company seems to be moving in the right direction. Like Roblox, these companies are about a potential story unfolding. The potential reward is a significant return based on a small initial investment. Look at it like a small fire; it could slowly burn or escalate into a major blaze. The stock is volatile and remains higher on the risk scale.

Nike—The turnaround story remains in play. Although sales have declined and the overall brand has stagnated, I am confident that the new CEO, Elliott Hill, can get Nike back on track. Although it seems like a somewhat oversimplified thesis, Nike should benefit from a Caitlin Clark halo effect. Clark was named Time Magazine Athlete of the Year and #100 on the Forbes 100 Most Powerful Women. I believe it is a safe bet Clark will rise up this list, as she is not even at her athletic peak. Clark’s fandom/demand is simmering, and Nike is known to historically promote and market athletes better than any other brand. It will be hard for Nike to screw this up.

Mercadolibre—I remain bullish. Most investors associate Mercadolibre with e-commerce, as it is the most valuable company in Latin America. Its strong infrastructure has created a fortified moat to protect itself from Amazon and other competitors. Next up is becoming the premier fintech bank in Latin America by leveraging its online ecosystem to extend into financial services. Mercardo Pago may never catch up to Nubank; it doesn’t have to. Mercardo Pago is penetrating a large market, and its competitive advantage comes from its ecosystem integration, much like how AWS benefited significantly from its integration with Amazon’s online business. The momentum and growth indicate that Mercado Pago will one day drive most of Mercdaolibre’s operating income, just like AWS does for Amazon. I am not bearish on Nu Holdings, but they are a pure fintech play. In contrast, Mercadolibe has several potential growth levers to pull, making it a superior investment.

While it’s difficult to say whether Big Tech is past peak growth, investors should start thinking beyond 5-10 ticker symbols, no matter how incredible they are.

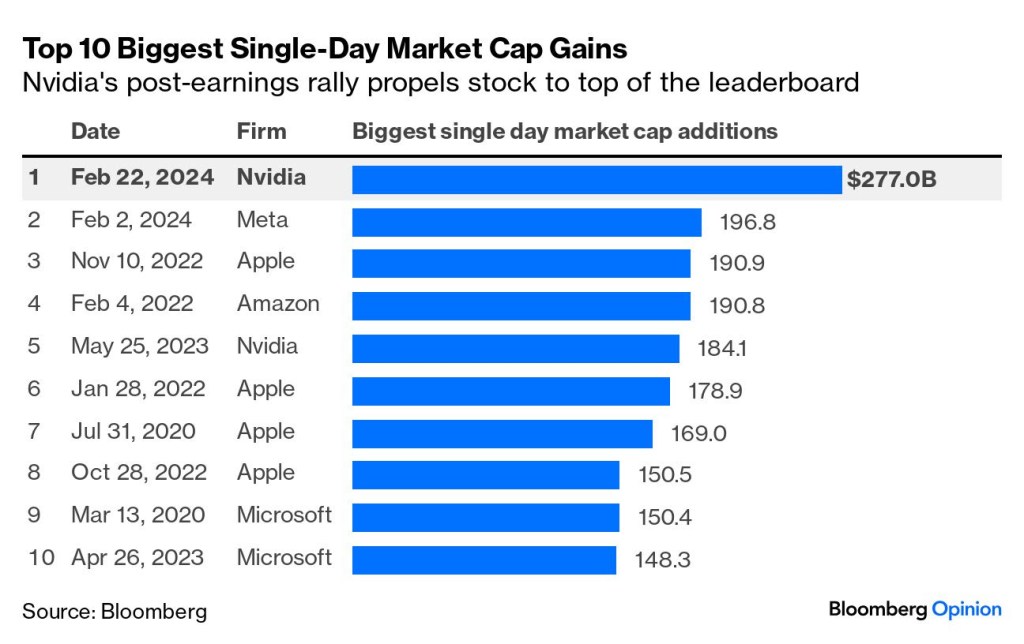

An obvious point needs to be made: If you have been investing for the past 10 years and have yet to own at least one of the big tech companies, you likely have been missing out. Any fund manager who has ignored these names has committed financial malpractice. The most significant single-day market cap gains in the past four years have come from Meta, Apple, Amazon, Nvidia, and Microsoft.

If you don’t own one of these names, you might ask yourself, “Why?”

These companies have a significant competitive advantage, allowing them to maintain their market share. They are well-positioned to benefit from several long-term trends, such as cloud computing and artificial intelligence.

It also helps that these companies can write blank checks to fight against regulatory scrutiny. They also can burn through a lot of cash on projects or initiatives that are unprofitable yet still maintain pristine balance sheets.

If you already own these names, there must be a compelling reason to sell them, and I don’t see any obvious red flags. These are companies you typically hold and don’t trade. However, strong evidence shows these names are no longer must-buys at any price.

In 2022, Facebook’s user base stagnated for the first time.

Apple’s revenue growth has been 5.5% from fiscal years ending in 2019 to 2023

Digital advertising, which accounts for over 80% of Alphabet’s revenue, slowed down in 2022. While Google Cloud revenue is still growing, the growth rate has slowed compared to previous years. The same goes for Amazon Web Services (AWS).

Although these are not necessarily signs that these companies are in peril, they signal cracks in the foundation. These companies still have high expectations for future growth. Yet, there is clear evidence of saturation and slowing growth in their core markets.

Revenue growth has already slowed, and it will get more challenging for them to get bigger. Acquisitions are a costly way to grow, but with regulatory pressures, that is not likely a realistic option anymore.

Meta also authorized its first-ever dividend, joining Apple, Microsoft, and Nvidia. A dividend usually means transitioning from a volatile, high-growth company to a stable, slower-growing one. Anytime a company offers a dividend, it gives away value to become more widely held by large institutions like pensions and mutual funds. This is the trade-off a company makes when issuing a continuously growing dividend.

What’s happening is that these companies are maturing. They are more predictable and closer to the consensus, aligning closer within parity to the general market. The Magnificent 7 is no longer a group of companies that produces alpha; it is a risk management group. The days of these names creating outsized gains in your portfolio are likely over. These companies will succumb to the law of large numbers, even Nvidia.

Is this a bad thing? Not necessarily. However, the ability of these companies to grow in size in the next ten years will likely be slower than in the past ten years. Looking at these names for supercharged growth is the wrong mindset for an investor. It’s wrong on both a fundamental and a valuation viewpoint.

Probabilities, Probabilities, Probabilities

The secret is out. These are high-quality businesses, and much of the value has been priced. The more new money you add to these names, the higher you will have to pay and the lower your future return.

There is still a place for adding stable, high-quality businesses in your portfolio, but better strategies exist to build a portfolio that outperforms.

Valuation and Quality Matters

An investor aims to find undervalued assets and dislocations in the market. Undervalued in valuation and fundamentals. Investing is not always about zigging when everyone else is zagging. An investor should also buy and hold quality, even at a premium price. Not every move is a contrarian bet, but a well-rounded investor must be able to do both. Having flexibility in thinking but a structured discipline process. Investors that can do both of these things will likely rise above the median.

As an investor, you must think like a general manager of an NFL team. Not owning a company in the Magnificent Seven is the equivalent of trying to win a Super Bowl without a star quarterback or pass rusher. Teams need quality players, but cost and value matters.

Patrick Mahomes is the best quarterback in the NFL. You can call him the Nvidia of Quarterbacks. That doesn’t mean the Kanas City Chiefs should trade him for draft picks and sign a lesser quarterback to save money. It also doesn’t mean the Miami Dolphins or Chicago Bears should mortgage their future and take on Mahome’s salary by trading for him.

The one luxury of being an investor in your portfolio is that you are the GM and Owner. You can enact your vision and strategy without the fear of being fired. If you want to “win,” you must make good decisions and not think in such a pedestrian matter.

Expensive players come at a high price that can and will diminish when they can’t keep up with overhyped expectations. Continuously overpaying, even for quality players, is a losing strategy because teams will run out of cap space. You will get less bang for your buck and likely cannot field a well-rounded team. The Chiefs’ success largely depends on getting production from their core stars and signing and drafting overlooked players in free agency and in the draft.

Buying stocks based on the market’s direction is not an investing strategy but a gambling strategy. You are not investing in companies; you are betting, period. You are falling into the trap of the allure of the market: Chasing gains and buying based on superficialities. This is emotionally a draining investment strategy when the inevitable business cycle fluctuates.

Nvidia was trading below 120 in October 2022. How many analysts had buy ratings on the company then?

Meta was trading below 100 in November 2022. What was the mood and sentiment of the market back then?

Who was pounding the table to invest in these names?

Finding quality value

As a long-term investor, think about sleepers and good bargains. Will it work every time? Of course not, but this is a proven winning investing strategy.

Build core positions in high-quality companies and add to them when undervalued. It also requires pulling the trigger when the street sits on the sidelines. There is absolutely zero edge or creativity when you follow the consensus agreement.

Every investor should, at minimum, look at the company’s balance sheet they invest in. While a balance sheet is valuable for understanding a company’s financial health, it doesn’t capture everything.

Characteristics of a good company that goes beyond the numbers:

Strong leadership: A clear and inspiring vision from ethical, transparent, and accountable leaders.

Brand reputation: A robust and positive brand image that resonates with customers and stakeholders.

Intellectual property: Valuable patents, trademarks, and other intellectual assets.

Customer & Supplier Relationships: Strong and collaborative relationships with key customers and suppliers.

These characteristics are not found in a balance sheet or screener. It requires more unconventional research and abstract thinking. I still have certain investing principles. If a company has negative gross profits (Revenue minus cost of goods), It’s almost an automatic no-touch investment. When revenue cannot cover the basic expenses incurred to create a product or service, it’s like a diner paying $6 for raw materials to sell a $5 burger. Fundamentally, the business needs to be fixed and likely won’t scale. This may seem rudimentary, but money continues to be poured into Rivian, Lucid Motors, and many other unprofitable businesses.

My playbook? I will only add to specific names in the Magnificent Seven if they become significantly undervalued, which will eventually happen, but less often than before. These names are becoming in lock-step with the herd, which means less opportunity. I will not be shy about adding to these names when the herd and the street flood out of these names. This strategy is a lot easier said than done. Heavy buying is usually best when you don’t hear a company like Nvidia is a “must-buy” stock, even though it has been up almost 2,000% in the past five years. I am OK with holding these names and increasing my ownership through a dividend reinvestment plan but not adding to them at these levels with fresh money.

Good solid investing requires creativity and outside-of-the-box within a framework. Look at traditional metrics, but be willing to go against the grain.

Two examples of looking beyond the numbers:

WWE fans are dedicated and incredibly loyal. The amount fans spend on scripted sports entertainment is quite astonishing. The revenue growth since the company went public in 1999 has been consistent. You would think fans’ interest would drift towards another form of entertainment, but it hasn’t. Fans of the product in the 90s and 00s are still engaged and driving consumption today. Pro Wrestling still hooks newer and younger fans, even though the format hasn’t changed.

WWE fans are dedicated and incredibly loyal. The amount fans spend on scripted sports entertainment is quite astonishing. The revenue growth since the company went public in 1999 has been consistent. You would think fans’ interest would drift towards another form of entertainment, but it hasn’t. Fans of the product in the 90s and 00s are still engaged and driving consumption today. Pro Wrestling still hooks newer and younger fans, even though the format hasn’t changed. An entire book could be written about pro-wrestling fanaticism, but the popularity is likely to continue for a long time.

Taylor Swift: Her current “Eras Tour” has an average ticket price of $1,088.56. Compare that to Dua Lipa for her past Future Nostalgia Tour, the average ticket price was around $97, or Olivia Rodrigo’s Current Guts Tour, which falls between $117-$637.

Explaining why a fan would spend so much on a Taylor Swift ticket is based on a combination of the artist, music, physical presence, and live experience. Explaining Swift-fandom is a complex phenomenon beyond rational or conventional thinking. Life itself is not static, and you must look at investing similarly. Swift’s meteoric rise wasn’t an accident or purely based on luck. In a different life simulation model, Swift is likely to be successful, even under worse circumstances. That’s because her success is influenced by various personal factors, not just based on one or two songs. Good investing is a process, not just being lucky in 1 or 2 ticker symbols. Investors who can develop a framework for success will likely avoid the pitfalls that the majority fall into.

I told Rick Barry I’d rather shoot 0% than shoot underhand. I’m too cool for that.

Myth #1: Quants, sophisticated algorithms, and the brightest minds in the world struggle to beat the market, and most do not. The odds are that Sam from Nebraska will not outperform the market and is better off not playing around with individual stocks. Just invest in index funds.

The problem you have, and will continue to see, is the word “invest” being interchangeably used with trading, gambling, speculating, etc…

Not everyone buying stocks is investing, certainly not long-term investing.

Many fund managers or professionals you read about do not even invest in their own fund.

Why would you invest in a fund if the fund manager isn’t doing the same?

Wall Street’s strategies differ from what you should mimic.

Investors need to understand the fundamental difference between generating income and building wealth. Typically, stocks are a wealth-building tool. Generating income from stocks requires more short-term thinking and trading strategies.

The more I see investors tinker with their portfolios or trade in and out of positions, the more confused I become. Price movement in the short term is often volatile and unpredictable. It also can be stressful and gut-wrenching. Emulating Jesse Livermore or Steve Cohen is more challenging than being the next Ronald Read or Geoffrey Holt.

As for index funds, the fundamental problem with this instrument is that it is a self-defeating investing practice. You have chosen to match the market rather than outperform it. The technical framework of most index funds is capping your gains by taking on less risk. This investment vehicle may suit some people, but I find it unacceptable.

Investing in index funds that follow a benchmark may be suitable for those who can generate a lot of income or have multiple income streams. It also may work if your portfolio is already large enough to live off without supplemental income.

You get what you deserve: The equity investor is entitled to a bigger reward because they took on more risk. Investing primarily in an index also does not change behavior or protect investors from the psychology of investing. Remember, future returns are not guaranteed. Index investing is popular because it has done well historically. Once again, a 10-15% average annual return is not guaranteed, and there is no way to assess the probability of future annual returns with pinpoint accuracy.

“A really wonderful business is very well protected against the vicissitudes of the economy over time and competition. I mean, we’re talking about businesses that are resistant to effective competition…”

“There is less risk in owning three easy-to-identify wonderful businesses than there is in owning 50 well-known, big businesses.”

– Warren Buffett

I never understood the attraction to wanting to own the entire market. It insulates yourself against a particular risk, but this diversification is unnecessary and can show a lack of focus and conviction.

Owning ten or more index funds or ETFs in your portfolios is “analysis paralysis” on steroids. There likely is a lot of overlap and bloat.

An investor must ask themselves, “What is the bigger picture?”

Diversification could help against risk, but over-diversification will likely hurt performance.

Diluted returns: Being right on a particular holding in a fund or index won’t make a material difference. The percentage of your portfolio is too insignificant to make a meaningful move.

Unnecessary risk protection: Some companies have a market cap equal to greater than the GDP of a small country. Not wanting to own these companies individually due to their potential to go to zero is not the best way to assess probability and risk.

The Brock Purdy/Tom Brady effect: The 49ers got lucky when they drafted Brock Purdy in round 7, pick #262. The Patriots got lucky when they drafted Tom Brady in round 6, pick #199. If these teams were confident that these quarterbacks would turn out the way they did, they would have drafted them in much earlier rounds. These teams took a small risk that paid off handsomely. Investing has similar scenarios. Investing $5,000 isn’t a lot of skin-in-game or conviction. A $5,000 investment in Microsoft in the 90s would be well over one million dollars today – and guess what? Microsoft is, by many analysts, rated a must-own stock today! These types of gains you will never see solely investing in an index.

Myth #2: I would have to spend countless hours researching individual companies and monitoring the market daily. Why invest in stocks with the odds out of favor in beating the S&P and its proven returns?

As I explained earlier, investors who primarily invest in an index are entitled to a lower return than a direct equity shareholder in companies who take on more risk.

The research barrier people make not to invest has always perplexed me. Looking at a company’s balance sheet is a relatively simple exercise. Earning reports are quarterly events and typically get recapped in a 1-page article.

Should an investor pay attention to current events and occasionally read business news? Everyone should be doing this, but is it necessary to spend several hours a day of research to be a successful investor?

Monitoring the market is a behavioral choice, not a requirement of being an investor. If you are a long-term investor and have already committed to holding a stock for an extended period, watching the price movement of a ticker symbol every day or every hour is an addictive habit that doesn’t help advance your investing skills. A company’s fundamentals do not change daily, even monthly, so worrying about daily price fluctuation is an unnecessary risk of losing your sanity.

No one can accurately predict the future. Every investment is a bet. You will likely succeed if you have a consistent framework for investment decisions and can understand the basic plumbing of how a company makes a profit. In most cases, the research advantage is not a true advantage. There is no significant correlation between time spent researching investments and investor performance.

Investor A: Invested $100,000 in Apple Stock in 2007 due to how innovative the iPhone looked during its launch.

Investor B: Invested $100,000 in Apple Stock in 2007 after doing hours and months of research in the company, reading balance sheets, plugging numbers through several financial modeling tools, reading articles, etc.

Investor B has more formal education than Investor A. Most people would consider Investor B “smarter” than Investor A. Investor B is an extremely hard worker, shrewd at business, and knowledgeable about the stock market.

The result is the same if both investors sell at the same time. Investor B may have been likelier to sell the stock, trying to time the market by mistaking research for market noise. For a long-term investor, selling Apple stock in the past 15 years would have been a mistake, even if the reason was valid.

Putting hours of research into investments doesn’t give you a guaranteed edge in investing. Having high cognitive intelligence doesn’t correlate to investing performance.

Investing does not require you to write a 200-page dissertation to be successful. “Time in the market” refers to the holding period, not time spent researching.

Being a highly-rated brain surgeon requires years of studying and training. The same goes for being a world-class athlete or chef.

Investing is a rare activity where sitting on your ass and doing nothing pays off more than trading in-and-out of stocks. The investor’s hidden superpower comes from having discipline, patience, and emotional intelligence. The stock market is auction-driven, where you cannot drive the outcome of the results outside of buying, holding, or selling a stock.

The skillset required is a behavioral one. That is the secret weapon needed to beat the market. In all likelihood, investors A and B have already sold their positions in Apple stock for various reasons.

“On the other hand, although I have a regular work schedule, I take time to go for long walks on the beach so that I can listen to what is going on inside my head. If my work isn’t going well, I lie down in the middle of a workday and gaze at the ceiling while I listen and visualize what goes on in my imagination.”

-Albert Einstein

The problem with the research argument:

Investors must understand that this game of critical thinking. Being an investor is a thought-job. Success comes from curiosity and continuous thought work.

Research/Investing is subjective. One person can determine Bitcoin as ‘rat poison,’ and another person can evaluate it as the future of money.

Investment returns directly correlate with how much risk you are willing to take, not how many hours of research you have done. No matter how much research an investor does, it cannot accurately predict future prices or events.

Myth #3: Pick the right company takes a lot of work. It is simply too risky, and the odds are not in your favor.

It is an easily debunked myth because the proof is an investor’s brokerage statement. Many professional and retail investors correctly invested early in companies like Nvidia, Apple, Amazon, and Tesla. These investors correctly picked the right company that generates life-changing results. These companies are well-known and have recognizable brands.

The problem is that most of these investors sold out too soon, indicating poor investment behavior. Investors frequently let fear and other emotions guide their strategic investment process.

Many investors also incorporate too much of a “market timing” tactical approach in their investment strategy, leading to how powerful psychological forces play into investing decisions. If the secret to wealth building is to buy and hold companies like Apple and Nvidia for a long time, why do so many people refuse to do so?

The answer is complex and simple at the same time. It would be like asking why don’t all poor free throw shooters in the NBA use the ‘Granny Shot’ free throw motion, where the player holds the ball at his waist with both hands and hoists the ball at the hoop in an underhand motion, with arms spread apart.

There is actual evidence that the Granny-style form works:

One argument in favour of shooting underhand, compared with traditional overhand, is that it requires less movement and is therefore easier to repeat. There are physics behind the form as well. Shooting underhand creates a slower, softer shot, because a two-hand shot, gripped from the sides of the ball, allows a player to impart more spin than a shooter launching the ball forward with one hand.

John Fontanella, a professor at the Naval Academy who wrote “The Physics of Basketball,” said most shots spin at two revolutions per second, but an underhand free throw will rotate three or four times per second. The additional backspin means more shots that bounce on the rim fall through.

Shaq attempted 13,569 free throws in the regular season and playoffs for his career. He made 7,103, just 52.3%, which is pathetic.

If Shaq worked on and adopted the granny shot the day he started the NBA, say, his career free throw percentage would improve to 70%. That’s 2,395 more points. How many more games and championships does Shaq win by doing this?

Despite the empirical and analytical evidence, no NBA star has adopted this shooting style since 1980.

Why? The answers players give are silly:

Shaq: “I’d shoot zero percent before I’d shoot underhanded.”

“They’re gonna make fun of me.”

“That’s a shot for sissies.”

The reasons why most poor free throw shooters don’t adopt a technique that is proven to work are similar to the same reasons why most investors can’t buy and hold stocks for a long time:

Fear of standing out

Outside of your comfort zone

Pride and ego

Herd mentality

Many investors invest like Shaq shoots free throws.

Shaq didn’t want to shoot underhanded because it wasn’t for him, even though it would have dramatically helped his free throw percentage.

People want to invest successfully, but they want to do it on their own terms. The rewards are life-changing, but it requires you to embrace chaos and uncertainty. Outside of your emotions, an investor has no control over the economy or geopolitics. For many investors, long-term investing means: “If I make money, I’ll stick with it, and if I don’t, I’ll sell and do something else.”

The most significant risk factor for investors is themselves.

It is not the economy, interest rates, or the threat of war. The biggest threat to your portfolio is your behavior.

My advice:

Do not get too cute with your overall portfolio strategy.

Stay focused and adopt long-termism.

If you have the discipline, adopt something similar to the coffee can strategy, an investing strategy where you mostly stay still during market volatility and sell recommendations.

Do not sell winners like Nvidia or Apple simply because someone says it is time to sell. These are companies you buy and hold, not trade. Selling a stock because someone said it’s wise to trim your position has been dud advice for high-quality companies. Keep asking yourself, “What is the bigger picture?”

People managing funds are investors at heart. They research solid companies in attractive industries that can grow from a long-term perspective. But they inevitably engage in profit-taking and market-timing based on news/rumors, drastically shortening the time horizon. We then become hyper-influenced by analysts’ recommendations and hyper-fixated on valuation metrics. Long-term investing involves holding during downturns, but letting your winners run is equally important.

Before ending the year, I wanted to discuss why investing is so difficult for many of us.

Investing is complex because several factors influence our decision-making and behavior. Some factors are within our control, and others are not. If you believe investing is only about math and financial modeling, you will likely struggle as a long-term investor. Investing is unique because it is a science and an art. It requires more than just analytics. There is a behavioral and psychological side that is much harder to measure.

Long-term investing: Much of what you’re willing to endure and risk to achieve a reward.

Investing behavior and decision-making are rarely caused by a single factor. There is an interplay of various influences that determines your risk tolerance and expectations. The better you understand these factors, the more likely you are to develop effective strategies to improve your performance.

When you think about successful investing, compare it to dieting and exercise. There are no shortcuts or one-size-fits-all answers. Generic solutions often become platitudes. Advice like weight is calorie-in-calorie-out, becomes a platitude. Someone morbidly obese could have the same diet as a marathon runner; the results may not be the same. Several key factors contribute to a healthy lifestyle. The same goes for investing. A financial expert who tells you the best way to support is to “index fund and chill” is oversimplifying a solution that doesn’t work for everyone.

Generally, people need to be motivated to lose weight. It is challenging to feel motivated if they do not see short-term results or if it takes too much time and energy to maintain a diet. Knowing vegetables and fruits are good for you doesn’t necessarily lead to a change in action. Understanding that you need to do more cardiovascular activities doesn’t mean you will start running daily. Without goals or action plans, you will get situations where people want to eat healthier but do not make meaningful changes in their diet or exercise.

Improving your outcome relates to your behavior. How do you change your behavior? Create goals to help develop your strategy. The more personal your goals become, the more likely you are to become motivated to achieve them.

Why invest:

Buy more material things.

Buy more experiences or influence.

Be able to support your spouse or family.

Fund your retirement.

Pass along your wealth to your children.

Why lose weight and exercise:

Improve external appearance.

Feel better physically and mentally.

Not be bedridden later in your life.

Be there for your loved ones.

Live a longer and more fulfilling life.

Investing is a mixture of science and human behavior. Human behavior is very imperfect, different, and subjective. Your behavior needs to change to see different results.

Financial experts say the best way to invest is through ETFs or index-weighted funds. Such advice is generic and does not change your behavioral psychology. It does not change the bad habit of consistently buying overvalued assets and selling them at a much lower valuation.

What happens when the index you invested in, based on the advice of experts, is down 10% or more?

Do you sell?

What if, after ten years, your portfolio is flat? Did you even plan on having a holding period that long?

If you are a long-term investor but continuously trade in and out of stocks.

If you enjoy highly volatile growth companies but have little tolerance for risk.

If you are health conscious, but your diet consists of fried food and sugary drinks.

If you spend a lot of money on athletic clothes but do not work out

Your actions do not align with your goals.

Align your goals and timeframe with your actions; the outcome should improve.

The problem with professional investing:

Most people can agree long-term investing works, and allowing high-quality companies to grow and compound requires a long-term holding period. So then, why is the average holding period of an individual stock just 6-10 months?

Professional fund managers: A profession where their income depends on quarterly performance. Income comes mainly from fees charged to investors who invest in them.

Funds flow out of underperforming funds and into those performing best, creating a casino environment where most fund managers chase gains and trade in and out of positions. Institutional fund managers’ informational and analytical edge over retail investors is almost useless, as they act more like traders than investors.

Institutional and Retail investors: Actions and goals not aligned with long-term performance.

Retail Investors: Freedom to invest without restrictions or deadlines. The behavioral edge often goes unrealized as retail falls victim to the same pitfalls as institutions – panic selling, over-trading, chasing gains/momentum, and emotional decision-making.

It is not your fault:

If you are struggling as an investor, it is not your fault. If you are struggling with losing weight, it is not your fault.

In 1942, the Metropolitan Life Insurance Company made standard tables to identify ‘ideal’ (and later ‘desirable’) weight, and with the naming of weight-to-height ratios as the body mass index (BMI) by Keys and colleagues in 1972, obesity was understood as a health risk that required medical intervention.

It has taken a while, but society is starting to accept that genetics, medical conditions, and other factors that contribute to our weight are outside an individual’s control. The American Medical Association (AMA) recognized obesity as a disease in 2013!

Labeling obesity as a disease is helpful as it takes pressure off the patient, not putting the blame all on themselves.

The same goes for investing. Human nature works against good investing. There is a tremendous fear of non-guarantees and a need for certainty. Human nature can work against us when it comes to investing. How does it feel to bungee jump 700 feet above the ground? You can only understand the feeling once it happens, just like how you will feel and respond to watching your portfolio fall 20% in a week. For most people, it’s likely a combination of fear, depression, and panic.

If lousy investing habits and obesity aren’t your fault entirely, how do you fix it?

The answer:

Every patient is different.

Every investor is different.

Each requires personalized attention and solutions.

I hate the phrase, “It isn’t your fault,” because even if true, what now? It does not give people the mindset that they have the power or control to change their circumstances.

Genetics, human nature, and upbringing play a role, but we are all not destined to be victims of circumstance. It is within our control over what’s preventing the desired outcome – Maintaining a healthy weight or having enough for retirement.

With the proper motivation and mindset, behavior can change gradually. There are no quick fixes.

Can GLP-1s like Wegovy or Ozempic help with weight loss? It could be part of the solution but only part of the solution. Medication does not replace a healthy lifestyle, what you eat, or daily exercise. Anyone struggling with weight should consult an endocrinologist and obesity medicine physician to develop a beneficial outcome.

Investing does not have one-size-fits-all solutions. Depending on your circumstances and financial goals, investing in funds that track broad-based indexes can help a portfolio. Should you consult a financial advisor? If that person can take the time to understand your needs based on your situation, it could help. Any effective solutions need to be customizable according to individual needs. As an investor, your primary objective should be to obtain greater knowledge and, as a result, steer you to more control over your finances.