Once the undisputed athletic apparel champion, Nike has faced increasing challenges recently. With Mark Parker’s departure and John Donahoe’s subsequent leadership, the company is struggling to keep pace with rapidly changing consumer preferences, particularly among Gen Z and Millennial demographics. The stock has seen a significant decline, underscoring the urgency of the situation.

A New Playbook

Starbucks’ revival under Brian Niccol’s CEO appointment is a powerful example of the transformative potential of strategic leadership change. Nike, too, could benefit from a bold and quick decision, emphasizing the need for risk-taking in order to reap potential rewards.

Sheryl Sandberg: The Perfect Choice

With her experience as Facebook’s COO, Sheryl Sandberg possesses a unique blend of skills and insights that are directly relevant to Nike’s current challenges. Her deep understanding of social media and her passion for women’s empowerment aligns perfectly with the company’s visions and goals, making her the perfect choice to lead Nike into a new era.

Leveraging Women’s Sports and Social Media

The growing popularity of women’s sports, exemplified by the rise of athletes like Caitlin Clark, presents a significant opportunity. Nike can tap into a powerful cultural force by investing in women’s sports and leveraging social media to connect with younger audiences. As a female executive who has broken barriers in the tech industry, Sandberg is well-positioned to champion women’s sports and empower female athletes.

Cultural Understanding

According to a recent survey, 40% of Gen Z and Millennials find women’s sports more exciting to watch than men’s, compared to about 25% of Gen X and Baby Boomers. Moreover, social media has become integral to how consumers engage with sports. Six in 10 Zoomers are very interested in content creators on Twitch or YouTube chatting about sports on live streams, and 70% discovered or deepened interest in sports through fan communities on social. This indicates a significant opportunity for brands to leverage social media to connect with younger audiences.

A Game-Changing Move

Sheryl Sandberg’s leadership could be the game-changer Nike needs to regain its cultural relevance and standing. Her proven ability to drive revenue growth, build strong teams, and foster a positive company culture would be invaluable in navigating the challenges of a rapidly evolving market, instilling hope and optimism in the company’s future.

Sandberg’s expertise and track record are based on optimizing and fine-tuning advertising revenue. She can create a more effective ad strategy, creating engaging and shareable content that builds communities and drives engagement.

The Time is Now

By bringing Sheryl Sandberg on board, Nike would signal its commitment to innovation and demonstrate its understanding of the changing landscape of sports and consumer behavior.

Caitlin Clark’s meteoric rise is changing the narrative of how we talk about women’s sports and how to market women athletes effectively. It’s a shift that’s happening now. Nike needs to adapt quickly, and bringing in a proven winning rockstar CEO can dramatically turn things around.

I endorse giving Sandberg a blank check to turn around Nike. John Donahoe is the wrong CEO to revive the brand. Sandberg’s background in technology is not directly relevant to the athletic apparel industry, but Nike has never been just an athletic apparel company—it’s a global cultural brand that celebrates great athletes. This is the right time, and Sandberg is an even better fit. I urge the Nike board of Directors to take action because quite, honestly, it makes too much sense.

Despite Nike’s current slump and the deserved hit its stock has taken, the growth potential is significant. Many of the issues are fixable, and with Nike’s robust financial and brand muscle, it can weather these storms, even a potential recession, as it did in 2008. Nike’s infrastructure and ecosystem have been stress-tested for decades, a testament to its resilience.

You won’t find it here if you’re seeking a deep security analysis of Nike Stock with a sophisticated review of Nike’s business. But that’s not a cause for concern. Nike is a simple business, and my investment thesis is relatively straightforward.

I am bullish on Nike because Caitlin Clark has the potential to propel it into a new hyper-growth phase, similar to the impact we saw with Michael Jordan in the 1980s and 1990s. This growth potential seems evident (the right time and place) for a magical story to unfold.

When Wall Street talks about Nike, it seems rather blah. Where is the creativity or outside-the-box thinking? Almost everyone analyzing this company is talking about the wrong thing. Nike can be summed up simply through a Steve Jobs quote:

“The best example of all, and one of the greatest jobs of marketing the universe has ever seen is Nike,” Jobs explained. “Remember, Nike sells a commodity. They sell shoes. And yet when you think of Nike, you feel something different than a shoe company. In their ads, they don’t ever talk about their products. They don’t ever tell you about their air soles and why they’re better than Reebok’s air soles. What does Nike do? They honor great athletes and they honor great athletics. That’s who they are, that’s what they are about.”

It’s not about the shoes; it’s about the people wearing the shoes!

It’s that simple.

A shoe is just a shoe. Proprietary shoe technology doesn’t move merchandise. Nike is an aspirational lifestyle brand. No other company in the world does a better job selling and promoting great athletes. They have an invisible superpower in their brand value, an intangible asset that drives a high level of engagement in selling apparel, shoes, and merchandise.

Nike isn’t the company it is today without Michael Jordan, who signed a five-year, $2.5 million deal in October 1984.

The contract was an absurd overpay for a basketball player at the time. Yet, now it looks like a slam dunk for Nike because Jordan transcended basketball and became a global cultural phenomenon.

The NBA and Nike didn’t elevate Jordan; it’s the opposite. The Jordan brand elevated basketball and sneakers to new heights. His sponsorship with Nike turned into a billion+ industry.

Nearly 30 years after Jordan signed with Nike, Clark signed an eight-year deal worth $28 million. This deal is bafflingly low for what could be a future brand worth $1-5 Billion.

Nike stock appreciated over 1,000% from when they signed Jordan to when he retired for the first time in 1993. It gained another 100% from when he returned in 1995 to when he retired for good in 2003.

In the story unfolding with Caitlin Clark today, we are witnessing the early stages of another cultural phenomenon that undeniably impacts culture.

How Clark can elevate Nike:

The Clark Effect:

A name that is trending up: Clark transcends sports. Very few athletes trend like this with long-term staying power. We already see this in the WNBA, a sport with an extremely niche following pre-Clark. The fanbase was small, with fans not spending “big” money on the product. That is changing.

Clark is now part of daily sports talk shows and debates. The more people talk about it, the longer it remains relevant and stays in the mainstream discussion.

Record WNBA attendance and viewership:

When the Indiana Fever played the Los Angeles Sparks, 19,103 fans attended Crypto.com Arena. That was more than the largest home game crowd for the Los Angeles Lakers, and LeBron James drew 18,997.

The cost of Indiana Fever tickets has doubled and, in some marquee matchups, nearly tripled compared to last year!

WNBA games are averaging 1.32 million viewers, almost tripling last season’s average of 462,000.

The WNBA has expanded, adding two new teams: the Golden State Valkyries in 2025 and a Toronto team in 2026. More stars will join the WNBA in the next four years – Paige Bueckers, Juju Watkins, Hannah Hidalgo, etc.- which will increase viewership and the league’s star power.

Based on ESPN personalization data, the WNBA has seen the largest YoY growth (+47%) among sports with 1M+ favorites

Caitlin Clark led all players with +373% MoM growth to become the 4th most-favorited active athlete, only behind LeBron James, Tiger Woods and Steph Curry

She is only trailing LeBron James, Stephen Curry, and Tiger Woods. Clark could quickly ascend to #1 in the next 3-5 years as the most famous athlete today, just entering her physical peak. The top three athletes in this list are nearing the tail end of their respective careers.

She’s a superstar:

We have seen hyped-up college athletes like JJ Redick and Jimmer Fredette before. We have witnessed Linsanity in the NBA and Tebow Mania in the NFL. None of these players were superstar athletes on the pro level, and their fandom eventually diminished.

No checkered past with a pristine record:

Clark seems similar to Jordan, a no-nonsense athlete intensely focused on basketball and obsessed with winning. No demons or scandals that diminished or brought down other athletes – Kobe Bryant, Johnny Manziel, and Michael Vick come to mind.

I don’t see Clark posting dances on TikTok or starting her podcast. She’s not an activist who is getting involved in politics. Eat, Sleep, Breathe, and play basketball. There are no distractions.

A new brand within a brand: Bigger than Air Jordan?

Clark already has a rabid, dedicated, and obsessive fanbase. Comparing Clark with LeBron James or Stephen Curry is the wrong comparison. Clark’s brand is more similar to that of Taylor Swift and Barack Obama.

Swift can make her fans spend over $1,000 on a non-premium seat ticket for a show and make them feel they are getting a reasonable deal.

Obama brought in millions of first-time voters to vote for him because (insert whatever reason you believe is correct) he propelled himself to a cultural phenomenon status.

A market largely untapped by Nike:

Nike’s women’s segmented business makes up just 22% of its sales.

Think of all the girls and women who want to buy Clark’s shoes. The market is largely untapped. Nike is seeing early success with Sabrina Ionescu and the Sabrina 1, a top ten WNBA player.

Clark’s brand could evolve beyond sneakers and boost Nike’s lifestyle segment into an entire product line of different types of shoes, socks, tracksuits, etc.

Identity with mass appeal:

Victor Wembanyama is a French basketball player and could be the best men’s basketball player in the next five years. He is also a Nike athlete, but I don’t see him coming close to bringing in what Clark does. “Wem-bany-am-a,” the name isn’t catchy or memorable. “Clark’s” is already a well-known popular shoe retailer in the UK. Besides the name, Clark is from the heartland and plays in the heartland.

I am not knocking Wembanyama or Ionescu as athletes, but like performers, style points matter in our culture. The top recording artists aren’t the top vocalists. Popularity and fandom are more a feeling than a rational thought. Competitive sports fall into a performance art category. What you won’t hear on CNBC or Bloomberg is the intrinsic relationship between Clark and her fans in the arena and online.

Get in while you can:

Wall Street will react once the shoe is released and the numbers are in an earnings report. I am getting in now. As we saw with Jordan, this feverish support can last for years, even decades. I see a noticeable halo effect for Nike, and this is like investing in Taylor Swift if she were a stock in 2010.

What I also love about this investment is that it isn’t binary. It could be a solid long-term investment rather than a trade.

Nike’s dividend (1.96%) is low, but given its financial health, it is well-covered by earnings and has increased over the past ten years. This trend should easily continue in the next ten years.

Nike trades at about 21x forward earnings. There is no expected earnings growth this year, so the stock is cheap (for a growth company) and reasonably priced, with low expectations.

Nike has a solid business that doesn’t need saving, but Clark could elevate the brand to a level that even Nike executives do not anticipate. A signature shoe deal was originally off the table during the initial negotiation, showing skepticism about the confidence that a shoe line by a female basketball player could drive sales. At this point, the skepticism doesn’t matter. It would be hard for Nike to mess things up and not capitalize on Clark’s meteoric rise in fame.

The biggest question is whether men will buy Clark shoes. I empathically believe yes. Hype and cultural shifts are not gender or even age-exclusive.

Take, for example, Donald Trump, who has said deplorable things against women. His actions against women have been equally disgraceful, yet he has millions of supporters who are women.

Taylor Swift’s fanbase is distributed uniformly across various ages. Almost half the people who attend her concerts are over 45, and her fanbase is almost evenly split 50-50 between males and females.

Humans are generally programmed to follow a herd. The more popular Clark becomes and achieves on the court, the more valuable her brand name becomes, making her a powerful force in selling merchandise to anyone worldwide, not just sneakerheads or young girls.

Even if Clark flops, this isn’t an all-or-nothing type of risk. The business is highly robust. Nike has missed trends and made mistakes in the past, but it always recovers because it excels at sales and marketing better than almost everyone else. If there is lightning in a bottle with Clark, Nike will know how to maximize sales. That’s what they do.

Nvidia has demonstrated an impressive growth trajectory, surging nearly 2,200% from $6 to briefly touching $140 in under five years. This meteoric rise even saw it surpass Microsoft as the most valuable stock in the market for a brief period.

Long-term investors, your perseverance and discipline have paid off. You’ve demonstrated two of the most crucial traits of successful investing: patience and discipline. While many struggle to hold a stock for even a year, you’ve shown the strength to hold on for much longer. This is an achievement worth celebrating.

The stock has made parabolic gains, but based on logic, rationality, and sound judgment, it’s time for long-time investors to cash out at least a small portion of your paper gains.

Nvidia is a fantastic company with A+ growth, leadership, and profitability. However, it is not immune to the macro economy, slowing demand, or a change in momentum/sentiment, which will inevitably happen.

As share prices rise, predictably, people with full-blown FOMO are joining the bandwagon late to the party. During this AI fever, consideration for valuation and rationality is put on the back burner as “dumb money” enters the market.

The people buying Nvidia stock now are momentum traders or dumb retail money. They admittedly have no idea what they are doing and are paying a premium for a very aggressive future outlook.

When I refer to ‘dumb money, ‘I’m not implying that these investors are unintelligent. It’s a term used to describe those who enter the market without a clear understanding of the investment they’re making, much like a dog chasing a car.

Here is a question from Linda in Illinois on a recent episode of Mad Money with Jim Cramer:

“I’m a retired postal employee who worked for 45 years. I have no financial investment knowledge. I wanted to know how to buy stocks, and I wanted to ask you if I should try to invest my Thrift Savings Plan (TSP) money in S&P Index Funds, or Magnificant 7, or Nvidia or all Nvidia.”

Think about the person in your family or at work who exhibits terrible financial acumen. The last person in the world you would want to take financial advice from.

The people considering buying Nvidia stock may have just learned about the company this year. They still may not even know what they do. If you’ve never heard of the company before last year, what happens if the stock craters? History shows people will justify their fears of a recession or market crash by selling at a deep discount and retreating into cash or gold.

This is perfectly normal animal behavior. But you are neither a dog nor a cat!

Again, Nvidia is a fantastic company—a best-in-breed company. But every company has a numerical valuation. With a straight face, can you say out loud that Nvidia will be a $10 trillion company by 2030? If you chase high growth, you typically pay a premium price for it and will likely underperform the market in the long run.

The risk-reward profile of buying Nvidia today significantly differs from a year ago. This may sound hard to believe, but shares are less valuable today because the valuation is far more uncertain than last year.

How many companies have gone from $3 trillion to $8-10 Trillion? Answer: None. Saying this happens with a level of certainty or confidence seems misplaced. It also ignores the risk of things going wrong. We are in uncharted waters with no precedent.

I’m actually coaching 8/9 year olds. Hoping to move up to middle school in the next 3-5 years.

Recently, the Lakers hired former player and current podcaster/ESPN analyst JJ Redick as their new head coach. Redick is the same age as LeBron James. He also has no coaching experience beyond youth basketball. Yes, you have read that correctly—a professional basketball team has hired a coach who has not even coached middle schoolers!

There is nothing wrong with being optimistic about Redick as a coach, but how can anyone be confident that he will succeed when he has never done it before? Of course, Redick could be the next Pat Riley or Phil Jackson; it could happen, just like Nvidia can continue skyrocketing. Valuation is an imprecise art because the future is unpredictable. But can you say with confidence this is probable or more possible?

Let me summarize my gameplan:

Am I saying to go all-in cash or to sell out of everything tomorrow?

No.

There is no need to think so dramatically or immaturely.

Betting against Nvidia is extremely risky.

Putting fresh money into Nvidia is risky because investing is more than just about data points and figures. Investing has far more intangibles, making it both an art and a science.

The safe time to buy Nvidia was the second half of 2022 when the US government banned them from selling chips to China and Russia.

I will ride Nvidia long-term, but the growth path is not guaranteed or linear. Past performance is no guarantee of future results.

Jennifer Lopez’s It’s My Party tour grossed $54.5 million with 31 shows in 2019. She recently canceled her tour. The same is true for the Black Keys, while other stars like Pink and Justin Timberlake (pre-DWI) have canceled some tour dates.

Meanwhile, Olivia Rodrigo’s “Guts” tour tickets go for above $570 on the resale market. In 2019, Rodrigo was a relatively unknown 15-year-old.

There is nuance and context to life and investing.

As a long-term investor in Nvidia, I am strategically preparing my portfolio by gradually increasing my cash holdings during periods of strength. This approach allows me to prepare for potential market downturns while benefiting from the company’s growth.

Nvidia is undoubtedly a great company, but why pay premium prices for future assumptions? I am building my cash position not out of fear but of a rational understanding that market fluctuations are normal. This way, I am prepared to take advantage of more appealing risk-reward profiles in the future.

It’s a win-win situation. Hold most of your holdings and reap the reward if the companies perform well. Trim your position in small incremental amounts to build cash. If bad things happen in the market, you at least have more cash to take advantage of a more appealing risk-reward profile in either a cheaper Nvidia stock or another company with a better runway for growth.

The law of big numbers says Nvidia will not hit $10 trillion by 2030. We have never seen a $3 Trillion company triple in 5 years. I am a contrarian, but even that sounds like a stretch. There are compelling companies that can go from $1-10 billion to $10-$100 billion, which is more plausible and we have witnessed several times.

There is nothing wrong with using nuance and rationality in investing. Take some money off the table, even just a tiny amount.

That’s how you, as an investor, need to think. Buy stocks when the valuation becomes desirable. To buy stocks when they are desirable, you need cash on hand, which is best built during days like today. What better time to raise money when your initial investment has increased 10x or more?

Preparing for the future by slowly building a cash position is sound investing advice because the market will eventually experience an inevitable downturn, and prices will fall. When risk falls, that would be a more appropriate time to pounce (use that animal instinct) and buy more aggressively.

Great investing requires a solid strategy and not just emulating pure emotional instinct. Don’t be the dog chasing a car.

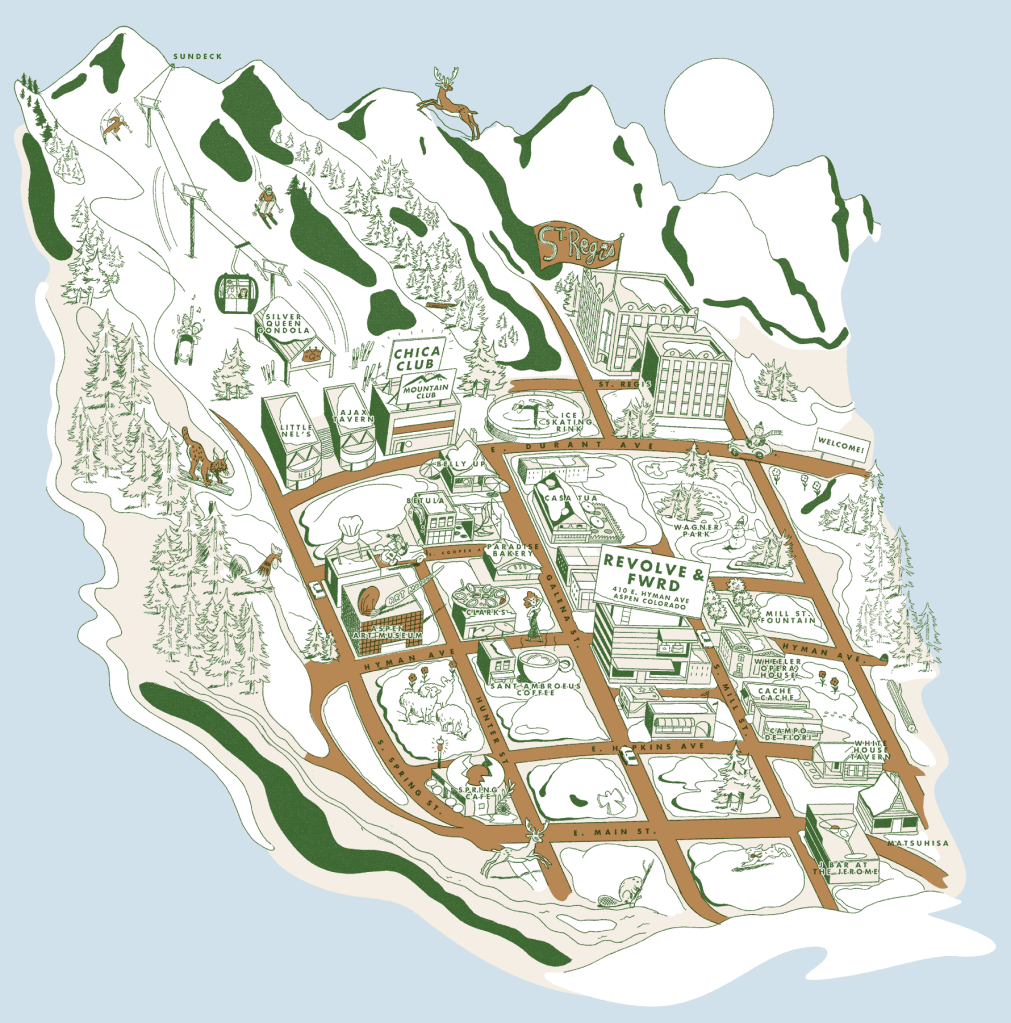

Revolve’s venture into brick-and-mortar retail with its first Aspen, Colorado store was not just a success, but a triumph. The initial pop-up store in December was a mere glimpse of the potential, and the decision to sign a multi-year lease was a resounding testament to Revolve’s ability to exceed its own expectations.

Why does this matter? Revolve, a digital-first business that has been diligently building its brand and e-commerce model, has made a strategic shift. Despite previous comments from earnings calls suggesting no serious plans for retail, Revolve has now embraced the potential of the physical retail space.

But the results were too good to ignore. It wasn’t so much that they sought retail, but demand called, and Revolve answered the call.

Aspen is just the beginning. With a robust digital marketing apparatus already in place, and the success of its first brick-and-mortar store, Revolve is poised for further expansion. This is a pivotal moment for Revolve, as it can now potentially translate its digital brand into a network of physical stores, paving the way for future growth.

This has the potential to increase an already impressive high average order value from the benefits of in-person shopping: impulse buyers from being able to feel and touch the merchandise. The Aspen store has also been a source of bringing in new customers, which is Revolve’s advantage and opportunity.

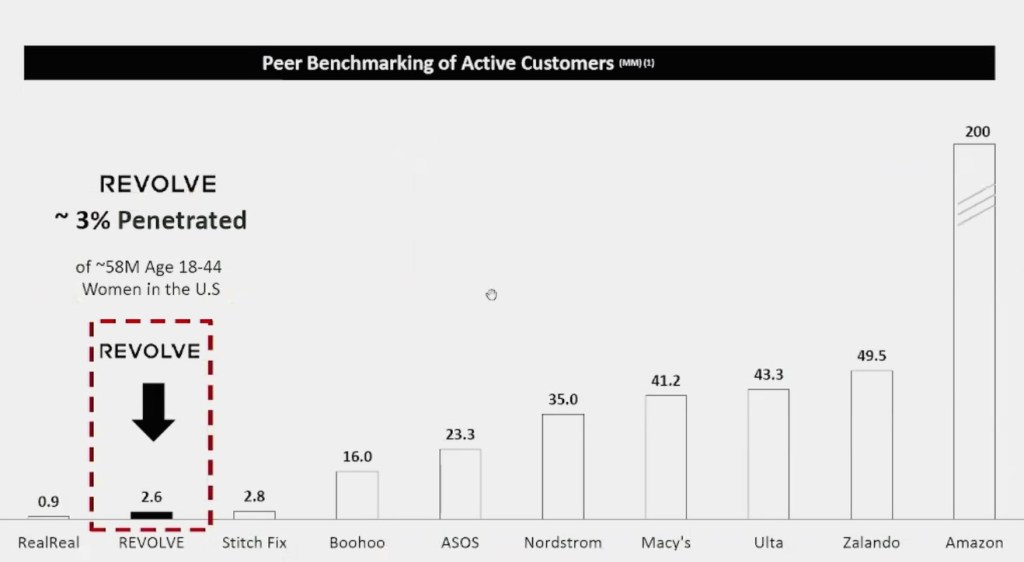

Advantage: Revolve’s customer base is mostly Millennial and Gen Z females. Roughly 60-70% of Macy’s and Nordstrom’s customers are Gen X and Boomers. I am not optimistic about legacy department stores. They have a problematic long-term business outlook. Macy’s is investing heavily in Bloomingdale’s and Bluemercury, but their brand name has declined significantly in the past decade. Nordstrom is doing a better job attracting young customers due to its off-price retail chain, Nordstrom Rack, but focusing on deals and discounts is a race to the bottom, and they will likely lose to Amazon, Walmart, and Target. I never understood Nordstrom’s business model because the off-price division does not complement the flagship stores. A “luxury” brand shouldn’t target consumers on a budget and vice versa.

Opportunity: Macy and Nordstrom need help mightily attracting Gen Z customers. It’s dire. Both companies will likely not show any year-over-year sales growth. Macy and Norstrom will eventually go private and leave the public market soon. It’s not a matter of if but when. These businesses may be able to restructure by going private, but it will likely take a very long time. Going private would also make raising capital difficult and cause a potential departure from key employees. Once the move happens, the capital and employees will likely shift towards a company like Revolve.

Is the Aspen store a signal for immediate retail expansion? I hope not. The focus should remain on building the digital platform and live events—Coachella, The Super Bowl, Cannes, etc. Physical retail should only complement the existing business unless the data overwhelmingly suggests otherwise. Much work is needed to build the brand through product/category expansion and international growth, which is more cost-effective through social media and pop-up events.

It would be premature for Revolve to make an aggressive retail push like Aritizia (3-5 new stores annually by FY27). They also don’t need it. Revolve has a much bigger online presence than other digitally native brands like Figs, Warby Parker, or Allbirds.

As a shareholder, I advise Revolve management to focus on curation rather than expansion. Identify 3-5 unique locations to create a highly personal and immersive experience. The stores should be bright and feature natural wood fixtures, making them engaging places to shop. Aspen works because it is an affluent city that blends luxury, charm, and scenic beauty. However, a store like Aspen is not scalable to a nationwide rollout. The ambiance is more subtle than in bigger cities like Las Vegas or Miami. It offers lesser-known brands in the high-end category to stand out more to a wealthy clientele.

I have identified some markets for Revolve to explore that can create a potential Aspen effect:

Park City, Utah Nantucket, Massachusetts Jackson Hole, Wyoming Charleston, South Carolina Carmel-by-the-Sea, California Key West, Florida Santa Fe, New Mexico

Entering smaller but highly profitable markets is a strategic move that makes perfect sense. Revolve, armed with ample marketing data, is poised to make prudent decisions and identify a few Aspen-like markets. The goal is to create a small footprint of high-ROI stores that offer a curated collection of luxury fashion brands—a blend of art, immersion, and boutique feel. The key is a luxurious bespoke experience, catering to the target audience’s preference for experiences over value or deal-hunting.

There is still plenty of room to grow. Despite a challenging macroeconomic picture for luxury retail, I haven’t sold any shares. I am confident in the business’s fundamentals and see a long-term pathway for growth and overperformance.

Why Tesla Shareholders should emphatically vote to approve Musk’s $56 Billion pay package

Musk’s compensation isn’t just about dollars; it’s about shaping Tesla’s destiny and soul. As shareholders, we are not just passive observers but active participants in this journey. Our votes on his pay package are a direct reflection of our belief in his vision and our commitment to Tesla’s future.

Under Musk’s guidance, Tesla’s stock price has skyrocketed, defying recent market turbulence. This dramatic rise starkly contrasts the stock’s value in 2018, which was a mere $21. Long-term shareholders have reaped substantial financial gains from this growth, a clear testament to Musk’s undeniable influence. This is not a personal viewpoint but an impartial, nonpartisan, indisputable reality.

Musk’s strategic decision-making has been a driving force behind Tesla’s success. Against all odds, he has led the charge in electric vehicle and clean energy innovation, reshaping entire industries. His ongoing leadership is not just important; it’s crucial for maintaining Tesla’s competitive edge and ensuring a prosperous future for the company. The potential loss of his leadership should inspire every shareholder to vote in favor of his compensation package.

Tesla’s long-term vision hinges on visionary guidance. Voting on compensation reflects shareholders’ trust in Musk’s ability to steer the company toward its goals. Elon’s compensation package is entirely contingent on achieving ambitious targets. If Tesla fails to meet specific triggers, Musk receives no compensation. This ensures that his pay is directly linked to the company’s success, aligning his interests with the shareholders. This alignment of interests should foster trust and confidence in every shareholder.

Tesla shareholders should ask themselves why they invested in the company in the first place. How many cars they sell this quarter or next quarter is less important than how they are positioning themselves for a Robotaxi world. This is an AI and Robotics company. Shareholders who dislike Musk or want to invest in a typical car company that achieves predictable quarterly numbers can choose from a bevy of other publicly traded companies.

Actual long-term Tesla shareholders don’t see Tesla as a car company; they see it as a venture with a start-up mindset into sustainable energy, AI, and software development. At heart, the vision is greater than just manufacturing vehicles. There is a clear line in the sand. Do you want Tesla to attempt to achieve moonshot or be a mediocre car company run by a Wall Street figurehead chasing predictable quarterly numbers?

If you vote no, you clearly communicate that you do not want Elon running Tesla. It’s a big middle finger to spite someone when the sentiment and stock price are low. Accelerate the transition to sustainable energy, revolutionize transportation, and produce humanoid robots at scale vs. grabbing low-hanging fruit and achieving goals with lower-moderate upside?

The rhetoric being spewed by pundits is biased, carrying a political agenda. Elon Musk’s loudest and most vocal critics are likely not Tesla shareholders, meaning they have no skin in the game. Think about it. Why would you “invest” in a company with a CEO you find deplorable? Does that make sense?

A story about business and technology has been hijacked by partisan fundamentalists. This rabid audience is tribal and less open to listening to opposing views. Elon Musk has been tagged as a villain that commentators will continue to deride. They have used the recent downturn in the stock as ammunition to defend their ideology.

Attacking Elon Musk has become a proxy for attacking President Trump. It’s that simple. These pundits are not your friends and are far from advocates of unbiased investment advice. Tesla stock could 100x and produce more than 200 million all-electric cars in a year; Elon Musk is still a con man to them, and the company is still a bad investment. Facts, data, and performance don’t change a fundamentalist’s opinion. It also won’t get them to admit they are wrong. The goal is to see Elon and Tesla fail spectacularly. Ask yourself if their interests align with yours as a shareholder.

I have voted yes because Elon’s pay compensation is necessary and mission-critical to Tesla’s future growth. Not voting for this package could potentially have catastrophic consequences. Losing his leadership would be a setback for Tesla and the future of our society as a whole. Musk is a man on a mission, and we as a society are in debt for his projects, which are critical to improving humanity through Tesla, SpaceX, Neuralink, The Boring Company, X, and xAI.

Elon Musk has revolutionized the electric car industry and taken on unimaginable financial and reputational risks. His sacrifices and suffering paved the way for Tesla’s success, allowing shareholders to thrive. This pay package is a testament to his past performance and a powerful incentive for future success. I voted yes because it keeps the trailblazer in place and re-positions Tesla into propelled growth for the next decade.

A Zoom court hearing in Michigan involved a defendant who was allegedly caught driving with a suspended driver’s license.

I invest in both companies.

I see solid fundamentals and strength in both businesses.

It is important to remember that the growth is still early in markets that are still evolving. Evaluating these companies based on traditional valuation metrics is problematic because these industries are far less static than other sectors. Both have bright futures, but Zoom would have a slight edge if I had to choose the better long-term investment based on a risk and reward estimation. This suggests a potential for high returns, inspiring optimism in potential investors.

Zooming in: Misunderstood as a one-product company:

Company

Revenue (Billions)

Gross Profit (Billions)

Earnings (Millions)

Palantir

2.23

1.8

209.8

Zoom

4.53

3.5

637.5

1. Core Functionality & Additional Services:

Zoom offers foundational features like video conferencing (Meetings), chat, and phone calls.

But on top of that, they provide additional services built around this core functionality like:

Rooms – dedicated video conferencing hardware for meeting spaces.

Events – hosting large-scale virtual events.

Contact Center – cloud-based call center solutions.

2. Openness and Integrations:

A key feature of platforms is openness. Zoom offers a Developer Platform (https://developers.zoom.us/docs/), allowing third-party developers to create custom applications that integrate with Zoom’s core services.

This extends Zoom’s functionality and caters to specific user needs. Imagine a Zoom app for scheduling meetings directly from your calendar.

3. Diverse User Base and Use Cases:

Zoom caters to a wide range of users, from individuals to large enterprises.

The platform’s flexibility allows it to be used for various purposes, such as business meetings, virtual classrooms, telehealth appointments, and even social gatherings.

In essence, Zoom provides a foundational communication platform and allows users and developers to build upon it to create customized experiences. This is a core difference from a product company that offers a fixed set of features.

Zoom has a larger TAM and a much easier pathway toward highly profitable growth.

According to the most recent reports, Zoom boasts 191,000 enterprise customers. While the exact number might fluctuate, Palantir has several hundred enterprise customers (1,300-1,500), significantly less than Zoom’s reported customer count.

Palantir primarily targets large enterprises, providing software platforms for data integration and analysis, often with over 10,000 employees and significant revenue. Zoom has a much broader customer base with businesses of all sizes.

One company targets a niche market of government agencies and large corporations with specific complex enterprise software solutions. The other offers a communication and collaboration solutions platform to businesses of all sizes, with its bread and butter being video conferencing.

Zoom is available in the Education, Financial Services, Government, Healthcare, Manufacturing, and retail industries. Palantir targets many of the same sectors; however, its platform is bulkier and has no actual application use for smaller enterprise businesses. Palantir’s software is generally considered expensive, with some estimates suggesting hundreds of thousands or even millions of dollars per year. Zoom offers a freemium model with tiered pricing plans, different features, and user capacities for businesses and government agencies.

A significant market opportunity ahead with an exceptional product:

Zoom saw 325.81% revenue growth in 2021 due to the pandemic. It is safe to say they will never see this type of year-to-year growth again, but it doesn’t need to.

Zoom is riding a consistent growth trend that began long before the pandemic. Work-from-home or Remote Work, whatever you want to call it, is the inevitable increased globalization of work. Fast Company coined the term “Gen Global” For Gen Z, who prefer “work from anywhere” and prioritize travel over education. Young workers grew up on social media and are more comfortable communicating via video conferencing.

Working full-time in the office is a dying trend. The new long-term trend is a form of hybrid work, from which Zoom will likely reap the rewards. As technology improves, the migration from On-Prem to the Cloud continues, and older CEOs phase out, companies will become more receptive to Zoom’s platform. Hybrid work is inevitably the future and growing; companies that resist the trend will lose out on talent, leading to a loss in profits. Zoom’s strategy to capitalize on this trend is to continue improving its platform and expanding its customer base, particularly in the government and healthcare sectors.

Zooms provides cloud-based products that the next generation of workers will use. Meetings offer a better mousetrap for workers and are becoming an essential product for employers to provide as an efficient way to communicate with each other.

It is popular among most workers who see it as a “perk.”

Reduced costs for real estate

Expanded pool of recruitable talent

Increased worker retention.

Adopted over time as hardline proponent CEOs of returning to work retire.

Fundamentals vs. Valuation:

Zoom and Palantir have been public for less than five years, so evaluating past performance based on limited data is difficult. With companies like these, it is more helpful to first zone in on the fundamentals to make an educated guess about the future.

The Artificial Intelligence Platform (AIP) is promising. I am a believer; however, the pathway is far from certain. Palantir’s commercial business is nascent, with even its most ardent supporters having to take a leap of faith that it will grow. Selling a product that companies don’t even know they need is almost impossible to map out five years out.

Palantir has a long sales cycle. Learning its solutions takes much longer because the learning curve is high. It will likely take a year before their platform shows any meaningful ROI.

AIP is intriguing and ambitious. The presentation deck is broad and alluring. It captures an investor’s attention when you help uncover human trafficking rings or battle the Russian army. I have determined the risk is worth the rewards as an investor, but valuing this as an investment is problematic because it assumes high optimism in a new space without a clear track record.

Can Palantir expand its commercial business and attract a broader and more diverse customer list? It is too early to know if the path is certain. A longer track record of low churn and increasing profits is needed to make a better determination.

Zoom’s software has already penetrated multiple enterprises, organizations, and businesses. However, its platform still has a lot of room to grow. Many analysts dismiss Zoom’s government business, which is largely untapped, more so than Palantir.

Another lockdown may not happen again, but the residual effects of the lockdown are seeing permanent work behavioral changes despite the pandemic being over:

Columbia University went fully remote due to Palestinian protests.

School districts in many U.S. cities went remote during the winter due to the flu/Covid outbreak.

Flu/Covid outbreaks will continue in the future.

Someone even had a Zoom court hearing while driving with a suspended license.

MLB’s league offices use Zoom Meetings, Zoom Rooms, Zoom Phone, and Zoom Webinar, while Zoom’s all-in-one collaboration platform is integrated across several MLB clubs, platforms, and broadcast outlets.

For a platform critics say is dying, people still use it daily. Zoom’s client list ranges from news broadcasts to hospitals, school districts, colleges, and courts. Its partnership with MLB is one of the best case studies of how Zoom’s suite of products can provide a large, multifaceted enterprise with various solutions.

The two biggest fundamental questions that I will be closely watching for the near future:

(1) Leadership execution, mainly if they can make intelligent acquisitions of smaller technology companies to complement and grow their existing businesses. Zoom has a large cash pile and will likely search for an acquisition target to grow its business.

(2) Increased sales and marketing. The CEO & Founder, Eric Yuan, acknowledged this on a previous earnings call: “One thing I think we did not do well, as I mentioned even before, is we did not do well on the marketing front. A lot of customers and users do not know Zoom has a greater presence in Team Chat functionality at no additional cost. And it works extremely well.”

Yuan has proven he can make great products, but Zoom must enter wartime sales mode. Zoom must ramp up S&M spending and sacrifice profits for growth. Zoom has a significant edge over Palantir because it has far more brand recognition. Conceptually, learning how Zoom’s products can help a business is easy. Practically, there is a low learning curve, with Meetings & Chat being extremely user-friendly. Foundry is a much more challenging platform to use and understand. Palantir would need to make Foundry less heavy to address many lukewarm and bad reviews. It’s an early and fixable problem but a potential red flag for future growth.

Both companies have potential opportunities, but Zoom has a bigger total addressable market. Despite the pandemic being over and Zoom becoming a target for other companies to criticize, Zoom’s platform is already becoming a mainstay in the enterprise ecosystem. The story is still early for its commercial and government businesses.

Low vs High Expectations and Sentiment

From a Price-to-Earnings Ratio and other traditional financial metrics, Palantir is an expensive stock. Is it overvalued? That depends on whether it can meet or exceed high expectations. Zoom is the opposite, an inexpensive stock with low expectations.

In the short term, Zoom has a low bar to jump. Analysts would view 5-10% YoY growth in 2025 as wildly optimistic and likely cause the stock price to double from today’s price. For Palantir, anything under 25%-plus overall growth would be disappointing and likely not well-received from Wall Street.

A company with high expectations can exceed them, but Zoom likely has better odds of meeting its target projections.

So why mention expectations? I discuss this to reflect the nuisance of investing and how to become a better, well-rounded investor. Suppose you are an investor and only consider the company’s qualitative aspects. That strategy probably works out in the long term, but you must ask yourself: Is there a compelling reason to buy the stock where it trades today? The better-discounted price you get, the more likely you have a higher return.

Analyst ratings for both companies are pretty tepid. Remember, Palantir traded above 35 in early 2021, and Zoom traded above 555 in 2020. Many bitter retail and institutional investors are underwater on their investments if they are still holding, but this is where the behavioral aspect of investing plays a factor. The mood of the market and macro environment was completely different during the pandemic than today.

The past is the past. An investor cannot change the price at which you bought the stock last year or five years ago. The company’s valuation is different, but if you are down 30-80% on your Zoom or Palantir shares, it doesn’t mean the company is 30-80% worse. Palantir has seen significant growth in its commercial business. Zoom is a high-quality company trading at a rare reasonable valuation with solid fundamentals. Zoom has yet to see its revenue decline, which likely would have happened if its platform was a pandemic fade. The low sentiment has manifested skepticism about the viability and feasibility of the Zoom platform. This creates a potential opportunity for patient longs who do not care about the lack of momentum. Shares for both companies are not overbought according to the relative strength indicator (RSI), a momentum-oriented technical analysis tool.

Final Thoughts:

Both of these companies have compelling evaluations. They meet the criteria for quality companies. I give the edge to Zoom because it trades more at a discount. Both companies have an opportunity because their balance sheets look healthy, and their cash flow is growing steadily.

I may seem down on Palantir, but as I said earlier, I invest in both companies. Although it looks fairly valued today, Palantir is not an overhyped AI company. I could be underestimating its fundamentals, meaning it is grossly undervalued today.

I love the fundamentals, but valuation matters. Can you ignore the possibility of an economic slowdown, a hiccup, or a U-turn in sentiment or the story’s narrative? Can you invest successfully, ignoring risk and assuming a large meteoric rise based on already-priced assumptions? I don’t have enough conviction to go all in on one name, but I do have enough of a risk appetite to stay on the ride and let it play out. Zoom’s sentiment today is low, and all the momentum it had during 2020 and 2021 seems to have evaporated. Although not dirt-cheap, Zoom appears like an inexpensive stock with better odds of overperforming.

While it’s difficult to say whether Big Tech is past peak growth, investors should start thinking beyond 5-10 ticker symbols, no matter how incredible they are.

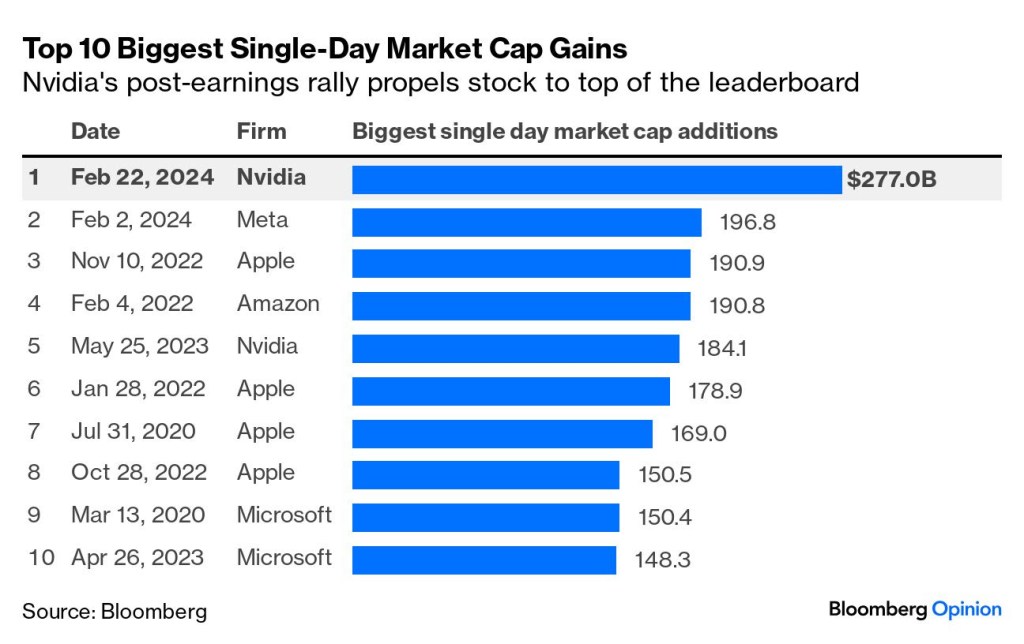

An obvious point needs to be made: If you have been investing for the past 10 years and have yet to own at least one of the big tech companies, you likely have been missing out. Any fund manager who has ignored these names has committed financial malpractice. The most significant single-day market cap gains in the past four years have come from Meta, Apple, Amazon, Nvidia, and Microsoft.

If you don’t own one of these names, you might ask yourself, “Why?”

These companies have a significant competitive advantage, allowing them to maintain their market share. They are well-positioned to benefit from several long-term trends, such as cloud computing and artificial intelligence.

It also helps that these companies can write blank checks to fight against regulatory scrutiny. They also can burn through a lot of cash on projects or initiatives that are unprofitable yet still maintain pristine balance sheets.

If you already own these names, there must be a compelling reason to sell them, and I don’t see any obvious red flags. These are companies you typically hold and don’t trade. However, strong evidence shows these names are no longer must-buys at any price.

In 2022, Facebook’s user base stagnated for the first time.

Apple’s revenue growth has been 5.5% from fiscal years ending in 2019 to 2023

Digital advertising, which accounts for over 80% of Alphabet’s revenue, slowed down in 2022. While Google Cloud revenue is still growing, the growth rate has slowed compared to previous years. The same goes for Amazon Web Services (AWS).

Although these are not necessarily signs that these companies are in peril, they signal cracks in the foundation. These companies still have high expectations for future growth. Yet, there is clear evidence of saturation and slowing growth in their core markets.

Revenue growth has already slowed, and it will get more challenging for them to get bigger. Acquisitions are a costly way to grow, but with regulatory pressures, that is not likely a realistic option anymore.

Meta also authorized its first-ever dividend, joining Apple, Microsoft, and Nvidia. A dividend usually means transitioning from a volatile, high-growth company to a stable, slower-growing one. Anytime a company offers a dividend, it gives away value to become more widely held by large institutions like pensions and mutual funds. This is the trade-off a company makes when issuing a continuously growing dividend.

What’s happening is that these companies are maturing. They are more predictable and closer to the consensus, aligning closer within parity to the general market. The Magnificent 7 is no longer a group of companies that produces alpha; it is a risk management group. The days of these names creating outsized gains in your portfolio are likely over. These companies will succumb to the law of large numbers, even Nvidia.

Is this a bad thing? Not necessarily. However, the ability of these companies to grow in size in the next ten years will likely be slower than in the past ten years. Looking at these names for supercharged growth is the wrong mindset for an investor. It’s wrong on both a fundamental and a valuation viewpoint.

Probabilities, Probabilities, Probabilities

The secret is out. These are high-quality businesses, and much of the value has been priced. The more new money you add to these names, the higher you will have to pay and the lower your future return.

There is still a place for adding stable, high-quality businesses in your portfolio, but better strategies exist to build a portfolio that outperforms.

Valuation and Quality Matters

An investor aims to find undervalued assets and dislocations in the market. Undervalued in valuation and fundamentals. Investing is not always about zigging when everyone else is zagging. An investor should also buy and hold quality, even at a premium price. Not every move is a contrarian bet, but a well-rounded investor must be able to do both. Having flexibility in thinking but a structured discipline process. Investors that can do both of these things will likely rise above the median.

As an investor, you must think like a general manager of an NFL team. Not owning a company in the Magnificent Seven is the equivalent of trying to win a Super Bowl without a star quarterback or pass rusher. Teams need quality players, but cost and value matters.

Patrick Mahomes is the best quarterback in the NFL. You can call him the Nvidia of Quarterbacks. That doesn’t mean the Kanas City Chiefs should trade him for draft picks and sign a lesser quarterback to save money. It also doesn’t mean the Miami Dolphins or Chicago Bears should mortgage their future and take on Mahome’s salary by trading for him.

The one luxury of being an investor in your portfolio is that you are the GM and Owner. You can enact your vision and strategy without the fear of being fired. If you want to “win,” you must make good decisions and not think in such a pedestrian matter.

Expensive players come at a high price that can and will diminish when they can’t keep up with overhyped expectations. Continuously overpaying, even for quality players, is a losing strategy because teams will run out of cap space. You will get less bang for your buck and likely cannot field a well-rounded team. The Chiefs’ success largely depends on getting production from their core stars and signing and drafting overlooked players in free agency and in the draft.

Buying stocks based on the market’s direction is not an investing strategy but a gambling strategy. You are not investing in companies; you are betting, period. You are falling into the trap of the allure of the market: Chasing gains and buying based on superficialities. This is emotionally a draining investment strategy when the inevitable business cycle fluctuates.

Nvidia was trading below 120 in October 2022. How many analysts had buy ratings on the company then?

Meta was trading below 100 in November 2022. What was the mood and sentiment of the market back then?

Who was pounding the table to invest in these names?

Finding quality value

As a long-term investor, think about sleepers and good bargains. Will it work every time? Of course not, but this is a proven winning investing strategy.

Build core positions in high-quality companies and add to them when undervalued. It also requires pulling the trigger when the street sits on the sidelines. There is absolutely zero edge or creativity when you follow the consensus agreement.

Every investor should, at minimum, look at the company’s balance sheet they invest in. While a balance sheet is valuable for understanding a company’s financial health, it doesn’t capture everything.

Characteristics of a good company that goes beyond the numbers:

Strong leadership: A clear and inspiring vision from ethical, transparent, and accountable leaders.

Brand reputation: A robust and positive brand image that resonates with customers and stakeholders.

Intellectual property: Valuable patents, trademarks, and other intellectual assets.

Customer & Supplier Relationships: Strong and collaborative relationships with key customers and suppliers.

These characteristics are not found in a balance sheet or screener. It requires more unconventional research and abstract thinking. I still have certain investing principles. If a company has negative gross profits (Revenue minus cost of goods), It’s almost an automatic no-touch investment. When revenue cannot cover the basic expenses incurred to create a product or service, it’s like a diner paying $6 for raw materials to sell a $5 burger. Fundamentally, the business needs to be fixed and likely won’t scale. This may seem rudimentary, but money continues to be poured into Rivian, Lucid Motors, and many other unprofitable businesses.

My playbook? I will only add to specific names in the Magnificent Seven if they become significantly undervalued, which will eventually happen, but less often than before. These names are becoming in lock-step with the herd, which means less opportunity. I will not be shy about adding to these names when the herd and the street flood out of these names. This strategy is a lot easier said than done. Heavy buying is usually best when you don’t hear a company like Nvidia is a “must-buy” stock, even though it has been up almost 2,000% in the past five years. I am OK with holding these names and increasing my ownership through a dividend reinvestment plan but not adding to them at these levels with fresh money.

Good solid investing requires creativity and outside-of-the-box within a framework. Look at traditional metrics, but be willing to go against the grain.

Two examples of looking beyond the numbers:

WWE fans are dedicated and incredibly loyal. The amount fans spend on scripted sports entertainment is quite astonishing. The revenue growth since the company went public in 1999 has been consistent. You would think fans’ interest would drift towards another form of entertainment, but it hasn’t. Fans of the product in the 90s and 00s are still engaged and driving consumption today. Pro Wrestling still hooks newer and younger fans, even though the format hasn’t changed.

WWE fans are dedicated and incredibly loyal. The amount fans spend on scripted sports entertainment is quite astonishing. The revenue growth since the company went public in 1999 has been consistent. You would think fans’ interest would drift towards another form of entertainment, but it hasn’t. Fans of the product in the 90s and 00s are still engaged and driving consumption today. Pro Wrestling still hooks newer and younger fans, even though the format hasn’t changed. An entire book could be written about pro-wrestling fanaticism, but the popularity is likely to continue for a long time.

Taylor Swift: Her current “Eras Tour” has an average ticket price of $1,088.56. Compare that to Dua Lipa for her past Future Nostalgia Tour, the average ticket price was around $97, or Olivia Rodrigo’s Current Guts Tour, which falls between $117-$637.

Explaining why a fan would spend so much on a Taylor Swift ticket is based on a combination of the artist, music, physical presence, and live experience. Explaining Swift-fandom is a complex phenomenon beyond rational or conventional thinking. Life itself is not static, and you must look at investing similarly. Swift’s meteoric rise wasn’t an accident or purely based on luck. In a different life simulation model, Swift is likely to be successful, even under worse circumstances. That’s because her success is influenced by various personal factors, not just based on one or two songs. Good investing is a process, not just being lucky in 1 or 2 ticker symbols. Investors who can develop a framework for success will likely avoid the pitfalls that the majority fall into.

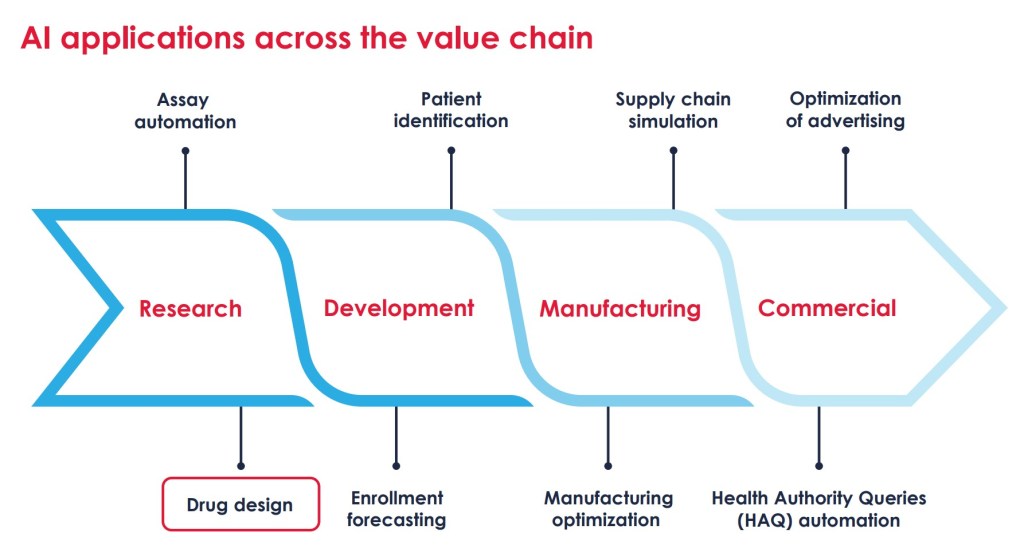

Moderna created the Spikevax vaccine, a miracle vaccine that saved millions of lives during the pandemic. Something not mentioned enough is how AI algorithms aided the vaccine in analyzing vast datasets to optimize the mRNA sequence in Spikevax.

While Spikevax isn’t an AI drug, it showed the potential of AI in accelerating and improving drug discovery. Moderna has always been an AI company since its founding in 2014. The impact of AI is seen almost everywhere in Moderna’s value chain, which makes it a leader in the space rather than a company responding to a hot secular trend.

mRNA vaccines have a bright future in medicine, and the story has just begun. mRNA is a molecule that teaches your cells how to produce antibodies that help fight certain diseases. The breakthrough discovery was utilizing Lipid Nanoparticles as a bubble to safely deliver the RNA (a fragile molecule) to its target cell. Once this happened, the technology was no longer theoretical but a signal that medicine had evolved.

The biggest challenge to Moderna and RNA technology is achieving efficient and targeted delivery to the suitable cells within the body. Optimizing RNA delivery efficiency to the desired cells remains a work in progress, but AI is streamlining this process with data analysis, experiment design, and manufacturing processes. These advancements have dramatically improved drug development efficiency, where we are no longer growing our drugs; we are printing them.

With Moderna experiencing tremendous advances in its platform, what does that mean for its future financial outlook?

Moderna estimates its combined annual revenue from its respiratory virus vaccines (COVID-19, RSV, and flu) to reach $8 billion to $15 billion by 2027.

Getting an approved RSV and flu vaccine would help Moderna return its revenue close to its peak during COVID-19, bringing in a whopping $19.3 billion in 2022.

Three approved respiratory virus vaccines may not propel its stock to all-time highs, but it would likely be significantly higher than where the stock trades today: In the 70-130 range.

What would be a paradigm shift for Moderna?

Moderna expects to add $10 billion to $15 billion in annual sales five years after launching new Oncology, Rare, and Latent diseases products by 2028. This is in addition to the previously announced $8 billion to $15 billion of expected sales from the Respiratory Franchise in 2027.

Moderna stock is undervalued and has a good chance of bouncing back. Whether it surpasses where it was in 2021 depends on how many approved vaccines it develops, the pricing, and the market adaption of each new product it launches.

My prediction. Moderna has 1-3 potential home runs in their pipeline outside of Covid. With a plan to launch 15 products in the next five years, one or two will likely be a blockbuster drug.

mRNA-4157 is a potential home run as a future cancer vaccine. Vaccines or therapeutic cancer treatments are always potential game changers because there is no effective cure for cancer. The timeline for a cancer vaccine is a long, unwinding road, but the results have shown promise against Melanoma, the key word being promise. Cancer therapeutics have always shown potential but are primarily unsuccessful. Although progress is very likely in the next five years, whether that will lead to a robust ROI is a complete mystery.

Moderna has many potential vaccines dealing with herpesviruses. There are over a hundred herpesviruses, but eight infect humans. Most people in the world have at least one of the eight herpesviruses:

Herpes simplex virus: double-stranded DNA virus

HSV-1 (oral Herpes): The most common type causes cold sores around the mouth. It can also cause genital Herpes, although this is less common.

HSV-2 (genital Herpes): This type of HSV causes genital Herpes, which can be painful and itchy. It can also be transmitted to a newborn during childbirth.

Human herpesvirus 3 (HHV-3): Varicella-zoster virus (VZV):

VZV is a viral infection that causes chickenpox in children and shingles in adults.

Human herpesvirus 4 (HHV-4): Epstein-Barr virus (EBV):

EBV is a widespread virus that infects most people at some point in their lives. It usually causes no symptoms, but it can sometimes cause Mono, a fever, and swollen glands.

Human herpesvirus 5 (HHV-5): Cytomegalovirus (CMV):

CMV is a common virus that can cause mild symptoms in healthy adults but can be severe for newborns and people with weakened immune systems.

Human herpesvirus 6 (HHV-6): Herpes 6

HHV-6 is a common virus that causes roseola, fever, and rash in young children.

Human herpesvirus 7 (HHV-7): Herpes 7

HHV-7 is a common virus that is often found in people with roseola, but it is not clear if it causes the disease

Human herpesvirus-8 (HHV-8): Kaposi’s sarcoma-associated herpesvirus (KSHV):

KSHV is a virus that can cause Kaposi’s sarcoma, a type of cancer, and multicentric Castleman disease, a rare inflammatory disorder.

There is a common theme with all Herpesviruses:

No cure.

Most people with herpes are asymptomatic: People can be infected with Herpes and not experience any symptoms. These cases often go undetected, contributing to the undercounting of total infections.

Very contagious and easy to spread in various ways.

The CDC does not recommend herpes testing for people without symptoms.

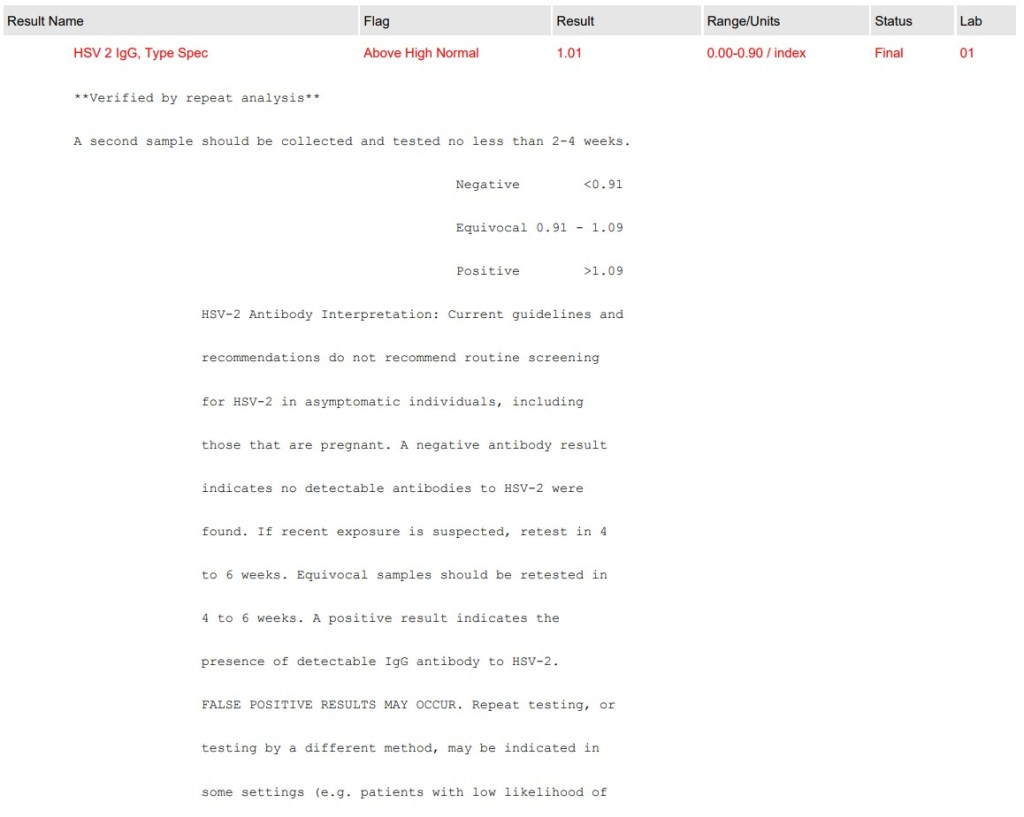

My test results indicate I have tested equivocal/positive for Herpes Type 2. Herpes Simplex Virus II is also commonly known as Genital Herpes.

Moderna has programs in development for Herpes simplex 1&2, VZV, EBV, and CMV.

Based on most conservative estimation models, 50% of the global population has oral Herpes, but more than 2 out of 3 people likely have it. Far more people, by a significant amount, have oral Herpes than are obese.

About 1 out of 8 people are more likely to have genital Herpes, but those estimates are likely conservative as well. The exact number is unknown, but it is expected more than 2 out of 10 people worldwide have genital Herpes. The complexity of the virus is that it is easy to spread even without symptoms, and it likely will not require any medical attention. Most people with Herpes do not know it, and the number of those who have recurrent painful outbreaks is in the minority.

Going through the process of getting tested for Herpes gave me insight into how profitable a vaccine would be.

My Western Blot results for Herpes Type 2, The Gold Standard for Herpes blood tests.

I recently took an STD Panel test and tested equivocal/positive for Herpes Type 2. I was pretty shocked as I never showed any symptoms. Mentally, it was starting to take a toll on my physique as I became worried every itch or pain was the beginning of an outbreak.

I learned that most standard blood tests for Herpes, when there are no sores or symptoms, are inaccurate. These tests are likely misinterpreting HSV-1 and HSV-2 antibodies with other antibodies your immune system produces.

I live in the only state in the United States that conducts the most accurate or “gold standard” for Herpes blood tests: The Western Blot at The University of Washington Virology Research Clinic. Through a referral from my provider, I was able to get my blood tested in person (anyone out-of-state has to mail their blood sample) and, after a week, received an official negative diagnosis for HSV-2.

Due to the complexity of the virus and the high number of asymptomatic cases or those that experience mild symptoms, a vaccine would create a massive opportunity with high demand and a large market.

Anyone who suffers from frequent outbreaks of Herpes is likely interested in a potential vaccine. More people would probably get tested if a safe vaccine were available, revealing a more prevalent virus than current studies suggest.

Even though Herpes doesn’t seem like a big deal, the stigma and psychology of the virus are real, particularly genital Herpes. How much money would you pay for a vaccine that would likely make having sex more accessible and safer?

Cancer and Herpes are only two potential growth catalysts for Moderna. The company has a long runway for growth, with over 45 developing drugs and 38 ongoing clinical trials. There’s a buffet selection of diseases, even though most of these trials will fail. Getting 10-15 drugs approved in the next five years could give Moderna a higher market cap than any other biotech company.

mRNA technology is still in its infancy. There are hurdles and uncertainty ahead, but the future looks exponentially promising. With many potential applications, this has the feel of the Internet or mobile phone in the early 1990s. Ten years from now, we will not look at mRNA as a fad but as a widely used technology much more significant than we could conceive today.

What’s wildly exciting is that we likely don’t know many things. Investing in what you don’t know is typically seen as a negative, as you can have blind spots toward risk factors. It’s important not to downplay the potential for a blue-sky scenario. The more we understand RNA and how to improve its delivery, the more likely we can see its capabilities and applications increase. Our current expectations may not be high enough. Moderna is developing drugs that can change the world and revolutionize medicine. It is important to remember the miraculous progress made in the past five years.

I told Rick Barry I’d rather shoot 0% than shoot underhand. I’m too cool for that.

Myth #1: Quants, sophisticated algorithms, and the brightest minds in the world struggle to beat the market, and most do not. The odds are that Sam from Nebraska will not outperform the market and is better off not playing around with individual stocks. Just invest in index funds.

The problem you have, and will continue to see, is the word “invest” being interchangeably used with trading, gambling, speculating, etc…

Not everyone buying stocks is investing, certainly not long-term investing.

Many fund managers or professionals you read about do not even invest in their own fund.

Why would you invest in a fund if the fund manager isn’t doing the same?

Wall Street’s strategies differ from what you should mimic.

Investors need to understand the fundamental difference between generating income and building wealth. Typically, stocks are a wealth-building tool. Generating income from stocks requires more short-term thinking and trading strategies.

The more I see investors tinker with their portfolios or trade in and out of positions, the more confused I become. Price movement in the short term is often volatile and unpredictable. It also can be stressful and gut-wrenching. Emulating Jesse Livermore or Steve Cohen is more challenging than being the next Ronald Read or Geoffrey Holt.

As for index funds, the fundamental problem with this instrument is that it is a self-defeating investing practice. You have chosen to match the market rather than outperform it. The technical framework of most index funds is capping your gains by taking on less risk. This investment vehicle may suit some people, but I find it unacceptable.

Investing in index funds that follow a benchmark may be suitable for those who can generate a lot of income or have multiple income streams. It also may work if your portfolio is already large enough to live off without supplemental income.

You get what you deserve: The equity investor is entitled to a bigger reward because they took on more risk. Investing primarily in an index also does not change behavior or protect investors from the psychology of investing. Remember, future returns are not guaranteed. Index investing is popular because it has done well historically. Once again, a 10-15% average annual return is not guaranteed, and there is no way to assess the probability of future annual returns with pinpoint accuracy.

“A really wonderful business is very well protected against the vicissitudes of the economy over time and competition. I mean, we’re talking about businesses that are resistant to effective competition…”

“There is less risk in owning three easy-to-identify wonderful businesses than there is in owning 50 well-known, big businesses.”

– Warren Buffett

I never understood the attraction to wanting to own the entire market. It insulates yourself against a particular risk, but this diversification is unnecessary and can show a lack of focus and conviction.

Owning ten or more index funds or ETFs in your portfolios is “analysis paralysis” on steroids. There likely is a lot of overlap and bloat.

An investor must ask themselves, “What is the bigger picture?”

Diversification could help against risk, but over-diversification will likely hurt performance.

Diluted returns: Being right on a particular holding in a fund or index won’t make a material difference. The percentage of your portfolio is too insignificant to make a meaningful move.

Unnecessary risk protection: Some companies have a market cap equal to greater than the GDP of a small country. Not wanting to own these companies individually due to their potential to go to zero is not the best way to assess probability and risk.

The Brock Purdy/Tom Brady effect: The 49ers got lucky when they drafted Brock Purdy in round 7, pick #262. The Patriots got lucky when they drafted Tom Brady in round 6, pick #199. If these teams were confident that these quarterbacks would turn out the way they did, they would have drafted them in much earlier rounds. These teams took a small risk that paid off handsomely. Investing has similar scenarios. Investing $5,000 isn’t a lot of skin-in-game or conviction. A $5,000 investment in Microsoft in the 90s would be well over one million dollars today – and guess what? Microsoft is, by many analysts, rated a must-own stock today! These types of gains you will never see solely investing in an index.

Myth #2: I would have to spend countless hours researching individual companies and monitoring the market daily. Why invest in stocks with the odds out of favor in beating the S&P and its proven returns?

As I explained earlier, investors who primarily invest in an index are entitled to a lower return than a direct equity shareholder in companies who take on more risk.

The research barrier people make not to invest has always perplexed me. Looking at a company’s balance sheet is a relatively simple exercise. Earning reports are quarterly events and typically get recapped in a 1-page article.

Should an investor pay attention to current events and occasionally read business news? Everyone should be doing this, but is it necessary to spend several hours a day of research to be a successful investor?

Monitoring the market is a behavioral choice, not a requirement of being an investor. If you are a long-term investor and have already committed to holding a stock for an extended period, watching the price movement of a ticker symbol every day or every hour is an addictive habit that doesn’t help advance your investing skills. A company’s fundamentals do not change daily, even monthly, so worrying about daily price fluctuation is an unnecessary risk of losing your sanity.

No one can accurately predict the future. Every investment is a bet. You will likely succeed if you have a consistent framework for investment decisions and can understand the basic plumbing of how a company makes a profit. In most cases, the research advantage is not a true advantage. There is no significant correlation between time spent researching investments and investor performance.

Investor A: Invested $100,000 in Apple Stock in 2007 due to how innovative the iPhone looked during its launch.

Investor B: Invested $100,000 in Apple Stock in 2007 after doing hours and months of research in the company, reading balance sheets, plugging numbers through several financial modeling tools, reading articles, etc.

Investor B has more formal education than Investor A. Most people would consider Investor B “smarter” than Investor A. Investor B is an extremely hard worker, shrewd at business, and knowledgeable about the stock market.

The result is the same if both investors sell at the same time. Investor B may have been likelier to sell the stock, trying to time the market by mistaking research for market noise. For a long-term investor, selling Apple stock in the past 15 years would have been a mistake, even if the reason was valid.

Putting hours of research into investments doesn’t give you a guaranteed edge in investing. Having high cognitive intelligence doesn’t correlate to investing performance.

Investing does not require you to write a 200-page dissertation to be successful. “Time in the market” refers to the holding period, not time spent researching.

Being a highly-rated brain surgeon requires years of studying and training. The same goes for being a world-class athlete or chef.

Investing is a rare activity where sitting on your ass and doing nothing pays off more than trading in-and-out of stocks. The investor’s hidden superpower comes from having discipline, patience, and emotional intelligence. The stock market is auction-driven, where you cannot drive the outcome of the results outside of buying, holding, or selling a stock.

The skillset required is a behavioral one. That is the secret weapon needed to beat the market. In all likelihood, investors A and B have already sold their positions in Apple stock for various reasons.

“On the other hand, although I have a regular work schedule, I take time to go for long walks on the beach so that I can listen to what is going on inside my head. If my work isn’t going well, I lie down in the middle of a workday and gaze at the ceiling while I listen and visualize what goes on in my imagination.”

-Albert Einstein

The problem with the research argument:

Investors must understand that this game of critical thinking. Being an investor is a thought-job. Success comes from curiosity and continuous thought work.

Research/Investing is subjective. One person can determine Bitcoin as ‘rat poison,’ and another person can evaluate it as the future of money.

Investment returns directly correlate with how much risk you are willing to take, not how many hours of research you have done. No matter how much research an investor does, it cannot accurately predict future prices or events.

Myth #3: Pick the right company takes a lot of work. It is simply too risky, and the odds are not in your favor.

It is an easily debunked myth because the proof is an investor’s brokerage statement. Many professional and retail investors correctly invested early in companies like Nvidia, Apple, Amazon, and Tesla. These investors correctly picked the right company that generates life-changing results. These companies are well-known and have recognizable brands.

The problem is that most of these investors sold out too soon, indicating poor investment behavior. Investors frequently let fear and other emotions guide their strategic investment process.

Many investors also incorporate too much of a “market timing” tactical approach in their investment strategy, leading to how powerful psychological forces play into investing decisions. If the secret to wealth building is to buy and hold companies like Apple and Nvidia for a long time, why do so many people refuse to do so?

The answer is complex and simple at the same time. It would be like asking why don’t all poor free throw shooters in the NBA use the ‘Granny Shot’ free throw motion, where the player holds the ball at his waist with both hands and hoists the ball at the hoop in an underhand motion, with arms spread apart.

There is actual evidence that the Granny-style form works:

One argument in favour of shooting underhand, compared with traditional overhand, is that it requires less movement and is therefore easier to repeat. There are physics behind the form as well. Shooting underhand creates a slower, softer shot, because a two-hand shot, gripped from the sides of the ball, allows a player to impart more spin than a shooter launching the ball forward with one hand.

John Fontanella, a professor at the Naval Academy who wrote “The Physics of Basketball,” said most shots spin at two revolutions per second, but an underhand free throw will rotate three or four times per second. The additional backspin means more shots that bounce on the rim fall through.

Shaq attempted 13,569 free throws in the regular season and playoffs for his career. He made 7,103, just 52.3%, which is pathetic.

If Shaq worked on and adopted the granny shot the day he started the NBA, say, his career free throw percentage would improve to 70%. That’s 2,395 more points. How many more games and championships does Shaq win by doing this?

Despite the empirical and analytical evidence, no NBA star has adopted this shooting style since 1980.

Why? The answers players give are silly:

Shaq: “I’d shoot zero percent before I’d shoot underhanded.”

“They’re gonna make fun of me.”

“That’s a shot for sissies.”

The reasons why most poor free throw shooters don’t adopt a technique that is proven to work are similar to the same reasons why most investors can’t buy and hold stocks for a long time:

Fear of standing out

Outside of your comfort zone

Pride and ego

Herd mentality

Many investors invest like Shaq shoots free throws.

Shaq didn’t want to shoot underhanded because it wasn’t for him, even though it would have dramatically helped his free throw percentage.

People want to invest successfully, but they want to do it on their own terms. The rewards are life-changing, but it requires you to embrace chaos and uncertainty. Outside of your emotions, an investor has no control over the economy or geopolitics. For many investors, long-term investing means: “If I make money, I’ll stick with it, and if I don’t, I’ll sell and do something else.”

The most significant risk factor for investors is themselves.

It is not the economy, interest rates, or the threat of war. The biggest threat to your portfolio is your behavior.

My advice:

Do not get too cute with your overall portfolio strategy.

Stay focused and adopt long-termism.

If you have the discipline, adopt something similar to the coffee can strategy, an investing strategy where you mostly stay still during market volatility and sell recommendations.